marketlan

Tourmaline Oil Update

Here’s an update on Tourmaline Oil Corp. (OTCPK:TRMLF), the largest natural gas producer in Canada and its fourth-largest gas processing midstream operator. Around 80% of the company’s production is natural gas, and it boasts the lowest capital costs in the Alberta Deep Basin.

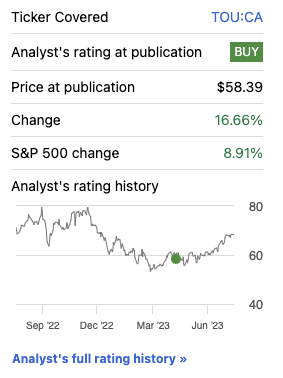

I previously recommended Tourmaline Oil as a buy at US$43 due to reported substantial insider purchases of C$6 million (US$4.45 million) worth of shares within the past year. Tourmaline’s undervaluation and healthy balance sheet also caught my attention – with a P/E ratio of 4.65, an EV/EBITDA of 4.23, and just $494 million in debt for a $17 billion oil and gas company.

Seeking Alpha

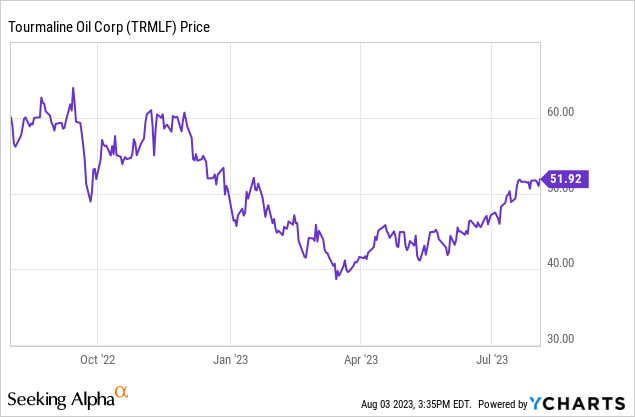

Since then, the stock has risen 16.66%, outperforming the S&P 500 (SP500), which rose by 9.11%. But the company’s Q2 2023 financial results suggest more share price gains are on the horizon.

Tourmaline: Analyzing Q2 Results

Tourmaline

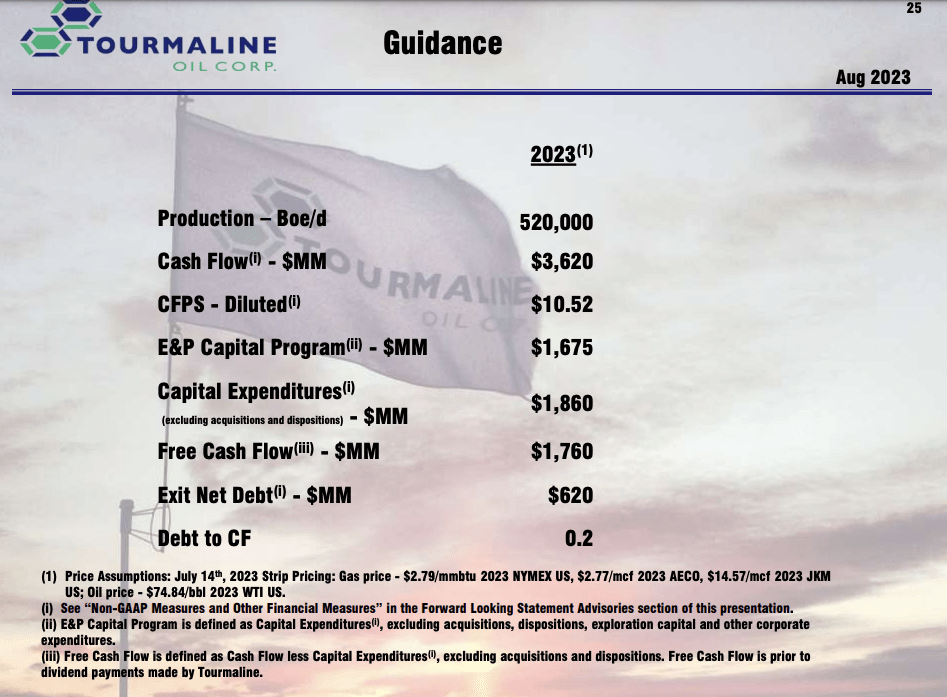

I’ve included a slide of Tourmaline’s 2023 estimated guidance for some background on what to expect in 2023 and how this quarter’s results compares to its full-year plan.

In Q2, Tourmaline excelled despite challenges, such as Canadian wildfires, which negatively affected many natural gas producers. Those wildfires resulted in a 3% reduction in the company’s production, causing delays in post-spring drilling and completion activities. However, Q2 production still averaged an impressive 495,918 boepd.

The company reported an average realized natural gas price of C$4.31/mcf in Q2 2023, higher than benchmark prices of C$2.46. Strong production and low cash costs led to a robust Q2 cash flow of $784.0 million ($2.28 per diluted share), and free cash flow of $545.5 million ($1.59 per share). Net earnings were $510.7 million, or $1.49 per diluted share.

Tourmaline also continues to reward its shareholders.

First, it plans to declare a special dividend of $1.00 per common share on August 22, 2023, and since September, has distributed total dividends of $7.74 per share. The stock yields over 10% when factoring in those total dividends.

The forward yield is likely much lower, but still substantial at an estimated 4%, based on the $.26 quarterly dividend and $1 special dividend. But that yield could go much higher if more special dividends get announced.

The company will also initiate a share buyback program on August 8, 2023, allowing it to purchase up to close to 17 million common shares over the next year, which, is likely a good idea given Tourmaline’s low valuation.

In summary, Tourmaline’s strong Q2 results and commitment to shareholder returns, combined with its healthy balance sheet (Net debt of $791.1 million or 0.2X its 2023 full-year forecast cash flow of $3.62 billion), position it as a solid investment option.

Tourmaline Is Still Deeply Undervalued

Despite Tourmaline’s impressive performance since our previous coverage, the stock remains compellingly undervalued. Currently, it carries a P/E ratio of 5.84 and an EV/EBITDA ratio of 3.92. Both figures sit comfortably below the sector medians, suggesting an attractive valuation.

Given the strong fundamentals and strategic advantages that Tourmaline has displayed, including robust production rates, strategic cost management, and a commitment to shareholder returns, the stock deserves a higher premium.

Tourmaline: Big Growth On The Horizon

Tourmaline

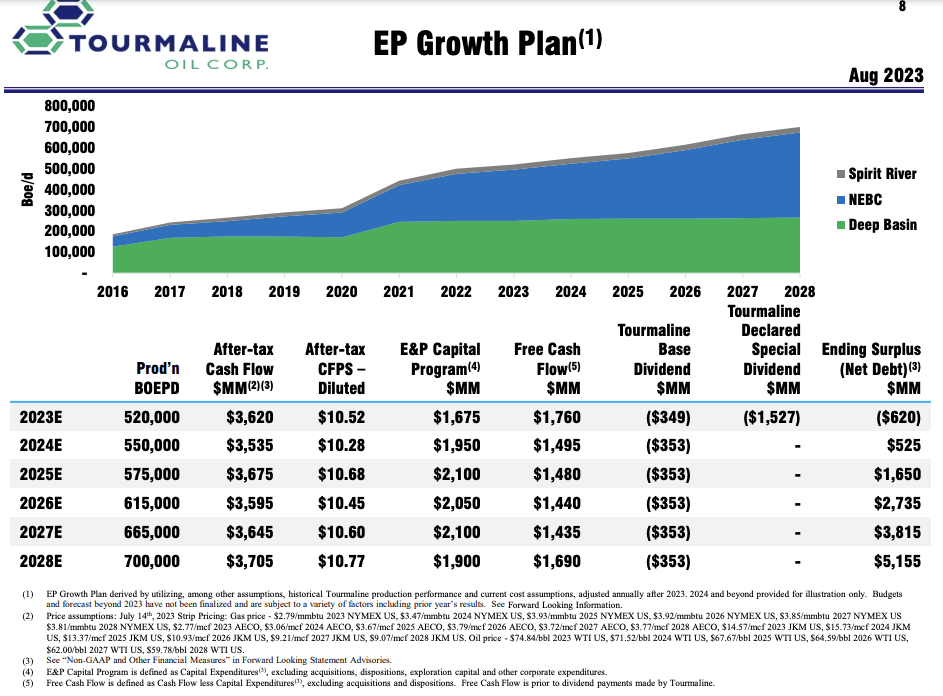

While Tourmaline’s near-term prospects are promising, it’s crucial for investors to consider the company’s long-term growth strategy. The company’s plan forecasts over 20% increase in production by 2026, with further growth expected through 2028.

Furthermore, the company anticipates generating considerable free cash flow, between $1.44 – $1.76 billion annually until 2028. This accumulation of resources could potentially lead to a cash surplus of over $5 billion by 2028. Note, this estimation includes Tourmaline’s base dividends but doesn’t account for any potential special dividends from 2024-28.

The company’s natural gas price assumptions appear conservative, with NYMEX US figures projected at: $2.79/mmbtu for 2023, $3.47/mmbtu for 2024, $3.93/mmbtu for 2025, $3.92/mmbtu for 2026, $3.85/mmbtu for 2027, and $3.81/mmbtu for 2028. Keep in mind, not too long ago, natural gas prices were trading above $9/mmbtu; however, a realistic long-term average likely falls between $4-$5.

Tourmaline: The Bottom Line

Tourmaline Oil, Canada’s largest natural gas producer, continues to demonstrate strong performance and commitment to shareholder returns. Despite being faced with challenges like wildfires, the company’s Q2 2023 results exceeded expectations. Robust production levels, strategic cost management, and generous shareholder returns make this company stand out.

Looking towards the future, Tourmaline’s growth strategy outlines a production increase of over 20% by 2026, with expectations of generating substantial free cash flow. These projections, coupled with what I feel are conservative natural gas price assumptions, hint at big gains in the future.

Despite all these factors, Tourmaline remains undervalued, which presents an opportunity for investors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

{kind=link}