AlizadaStudios/iStock via Getty Images

Phillips 66 (NYSE:PSX) is a multinational energy company with an almost $50 billion market capitalization and a dividend yield of more than 4%. The company has worked to build up an impressive portfolio of assets since its spin-off from ConocoPhillips (COP), and as we’ll see throughout this article, despite a stagnating share price can drive strong returns.

Phillips 66 Overview

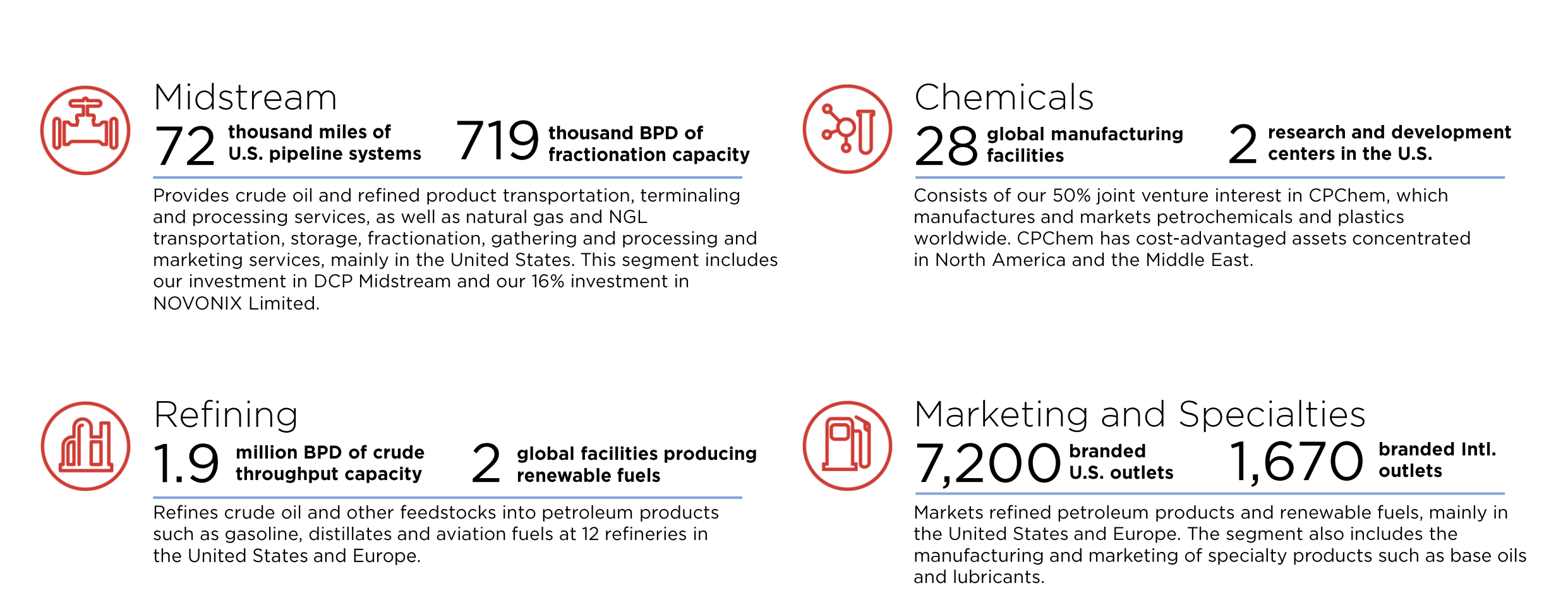

Phillips 66 has an impressive and diverse portfolio of assets.

Phillips 66 Investor Presentation

The company has 72 thousand miles of U.S. pipeline systems, a large portfolio, supported heavily by the company’s effective acquisition to have a >80% strength in DCP midstream. The company also has 719 thousand barrels / day of fractionation capacity, a popular industry that comes to grow aggressively.

For the company’s refining assets, its midstream assets manage to integrate well into its overall portfolio. The company’s refining assets consist of a massive 1.9 million barrels / day of assets and throughput including 2 facilities producing renewable fuel. The company’s strength here continues to almost 10 thousand branded outlets for selling the fuel it refines.

The company also has strong refining operations with 28 global facilities. That enables the company to refine other high value products in line with its global manufacturing portfolio.

Phillips 66 Priorities

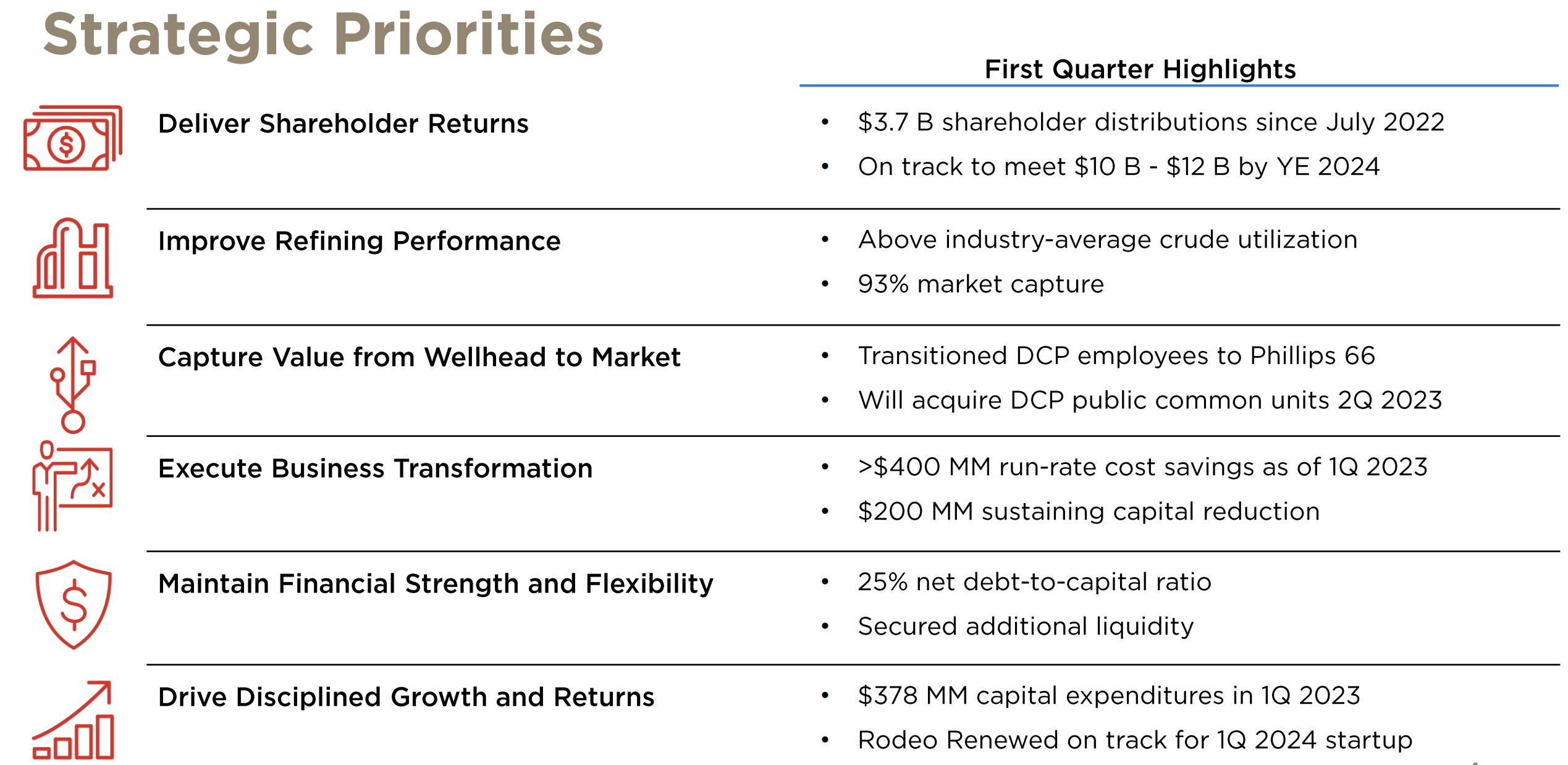

The company’s priorities are to continue generating strong shareholder returns, given its strong established assets.

Phillips 66 Investor Presentation

The company is targeting $11 billion of shareholder returns by YE 2024 as it continues to invest heavily. For refining its goal is to improve its operations and keep margins high. The company’s DCP acquisition will help it to improve margins and operations here. The company expects overall synergies to remain strong supported by heavy capital reductions.

The company recently approved $5 billion in share repurchases and repurchased $800 million in the most recent quarter.

Phillips 66 Financial Targets

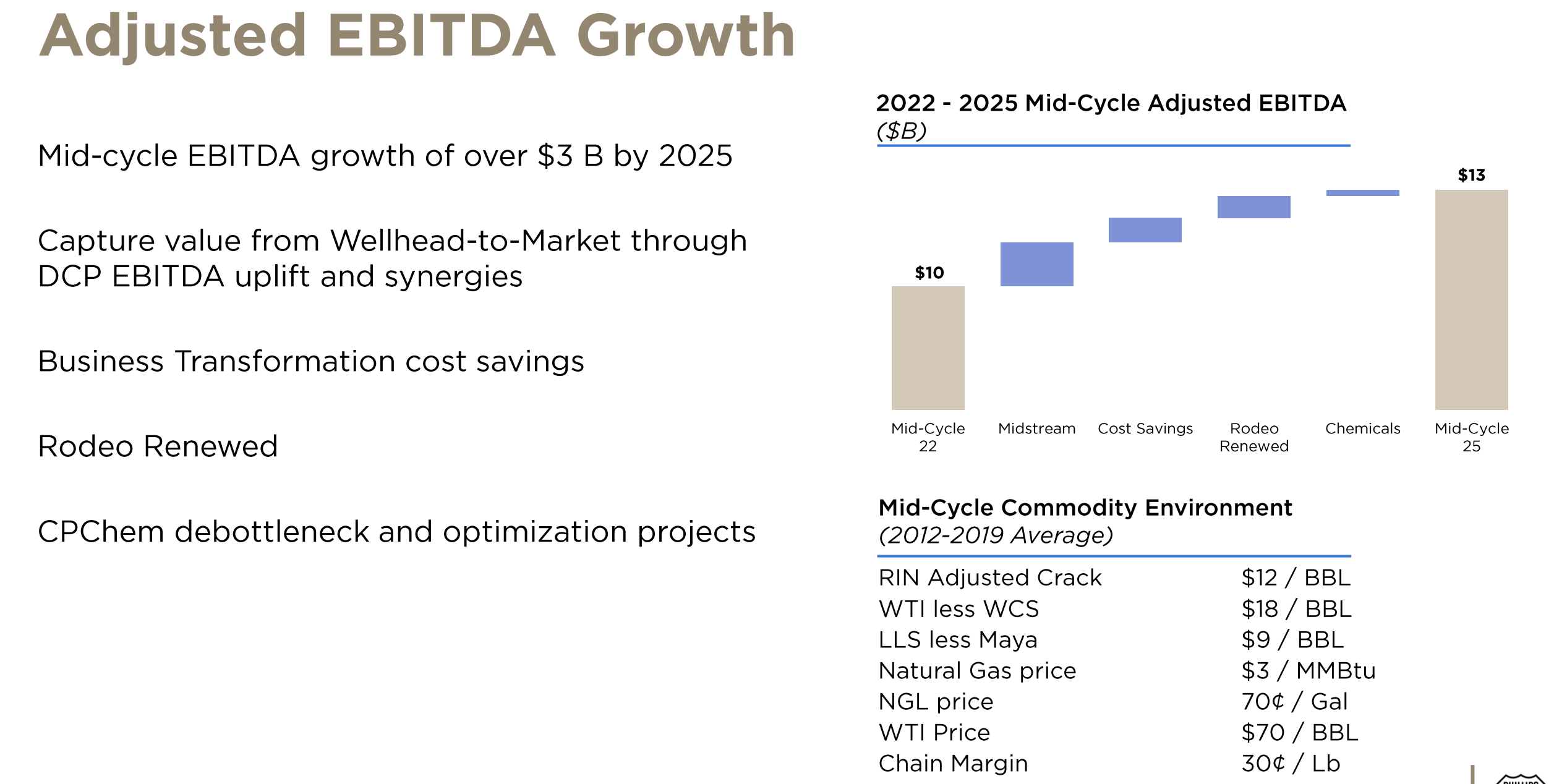

The company expects its mid cycle EBITDA to continue growing and it continues to increase margins and operations.

Phillips 66 Investor Presentation

The company expected mid-cycle EBITDA to grow from $10 billion in the current year to $13 billion in 2025. That’s supported by a variety of factors, including increased midstream synergy capture (supported by its DCP acquisition), increased cost savings, and a growing portfolio of renewable fuels that are in high demand by companies.

The important takeaway for the above is the 30% growth in mid-cycle EBITDA the company is targeting in a 3-year period with minimal investment. Those are high margin earnings for the company.

Phillips 66 Refining

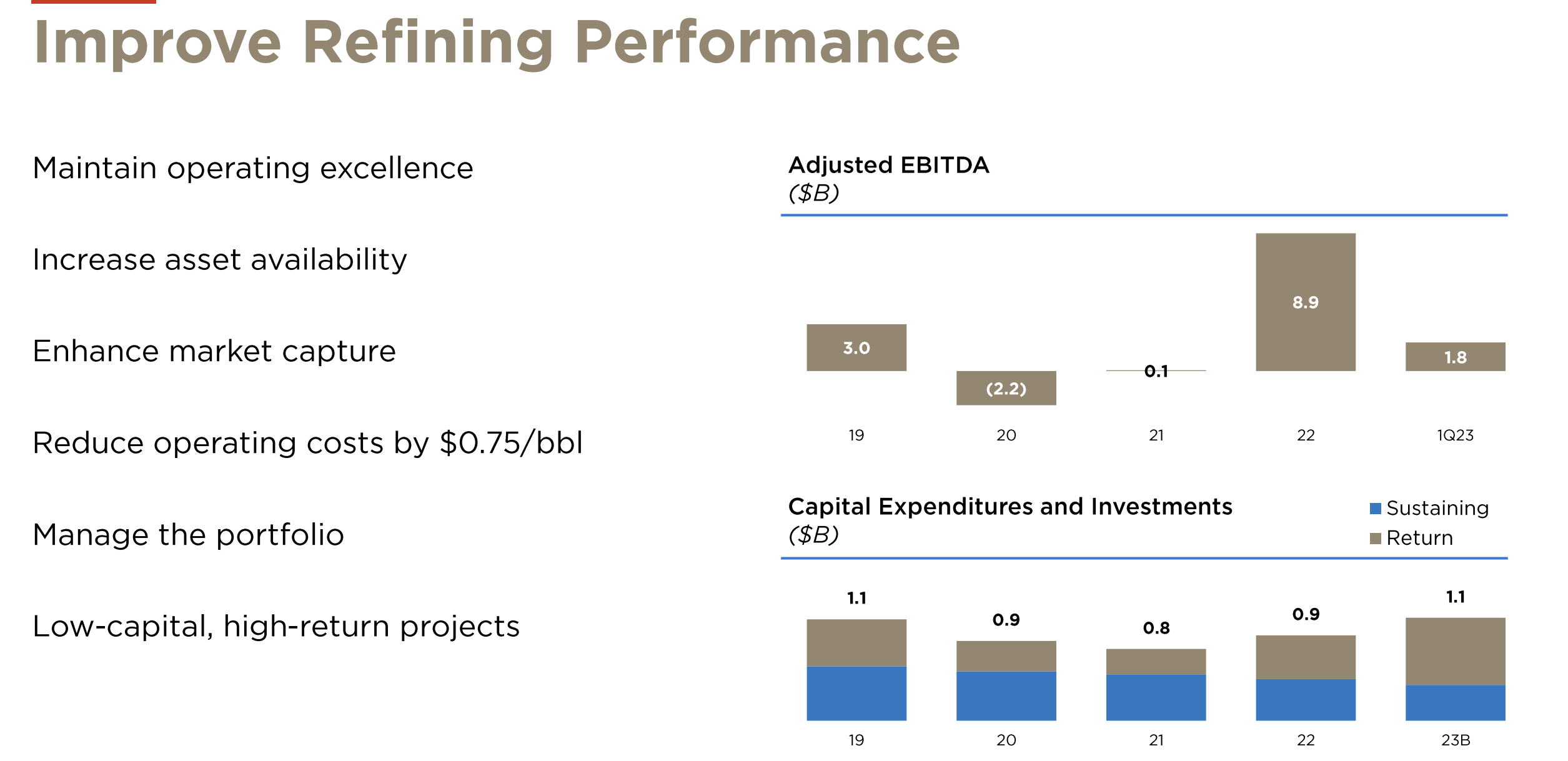

The company’s refining segment continue to generate strong earnings as margins remain strong.

Phillips 66 Investor Presentation

However, it’s worth noting that earnings here remain volatile and capital expenditures don’t disappear. The company’s capital sustaining expenditures are roughly $600 million / year and don’t disappear. The company is focused on reducing operating costs and has done well so far, and margins in the industry remain strong for now.

But it’s always worth keeping in mind that these margins can drop massively during a downturn hurting the company. The hefty fixed and sustaining costs of refining means that negative earnings are definitely a continued possibility during bad years.

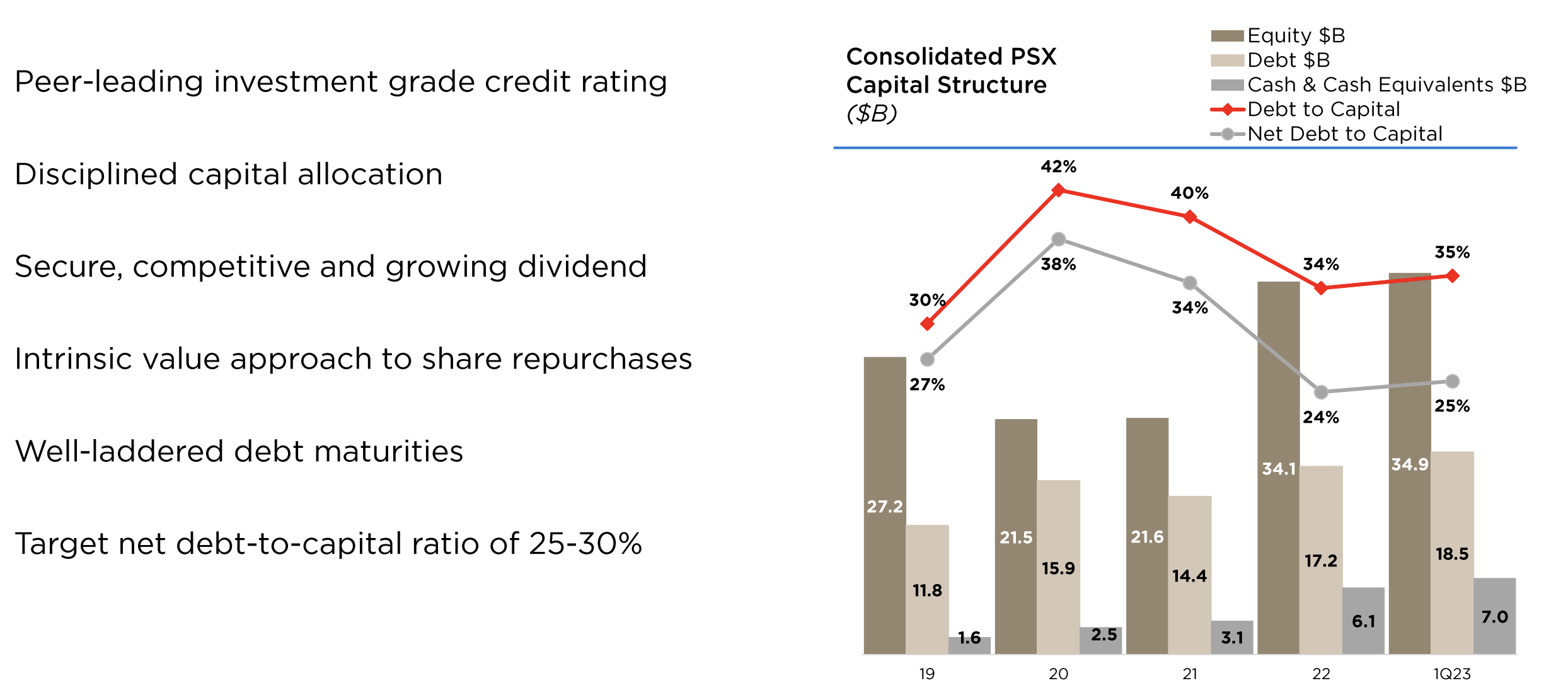

Phillips 66 Financials

Phillips 66 continues to maintain a strong portfolio of assets that the company can drive towards shareholder returns.

Phillips 66 Investor Presentation

The company has $18.5 billion in debt and $7 billion in cash and cash equivalents. That means the company’s net debt to capital is 25%, a level that’s come down over the last several years. This is clearly a level of debt that the company is comfortable with and one that it can maintain. That helps to highlight the company’s financial strength.

The company has a dividend yield of more than 4%. The company has long driven shareholder returns through a consistent repurchase of units, which push its returns to the double digits. More importantly, as long as refining spreads remain high, regardless of how temporary, the company can repurchase units to drive returns.

Thesis Risk

The largest risk to our thesis is refining margins and how quickly they can collapse coupled with the company’s high consistent spending obligations. It can lead to a concerning collapse in profits during tough times, something the company can handle, but also something that heavily impacts shareholder returns. As a cyclical company, a protracted downturn impacts the company more.

Conclusion

Phillips 66 has an impressive portfolio of assets. They’re a large scale technical refiner, and as a result, they get to enjoy strong margins in the industry. Demand for their assets and operations remain strong. Their new focus and growth in renewable fuels is a high-margin product that’s in high demand as company’s look to reduce their carbon footprint.

The company has the ability to continue driving strong shareholder returns. It has a long history of repurchasing shares to generate returns and we expect that to continue for the company. Additionally, it has a reasonable baseline dividend. In the meantime, as long as margins remain high in the short-term repurchases can help long-term margins.

Overall the strong current environment, and the company’s long-term operation potential, make it a valuable investment.

{kind=link}