Natural gas prices in the U.S. are caught in a seasonal crosscurrent. As May shows, the market faces a delicate balance: rising temperatures in the South are ramping up power demand, LNG exports are hitting record highs, and European buyers are back in the market. Yet, soaring storage injections and robust domestic productions are constraining prices — for now. Top it off with economic uncertainties and changing trade policies, and it’s clear that the U.S. gas prices are being pulled in multiple directions. This analysis unveils the key forces shaping the market and what they signal for months ahead.

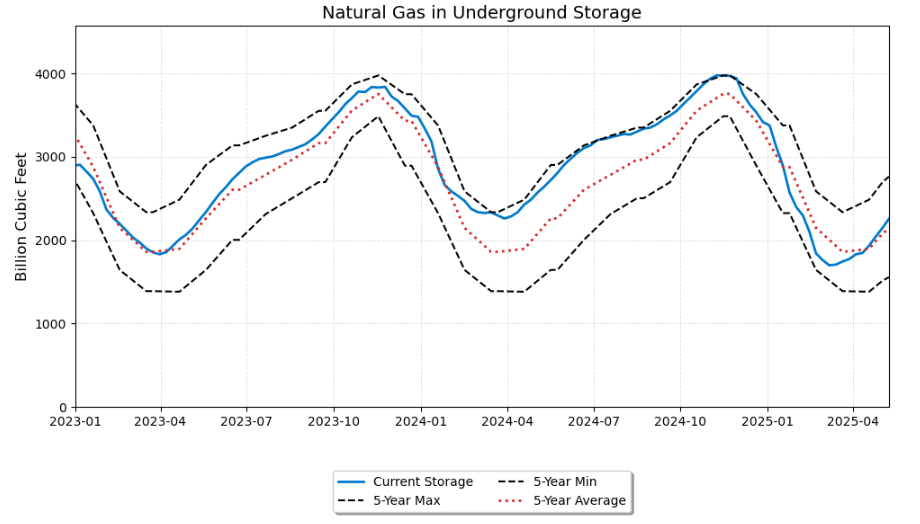

Storage Levels USA

As of Friday, May 9, 2025, working gas in underground storage in the Lower 48 states was 2,255 billion cubic feet (Bcf), according to EIA estimates. This represents a net increase of 110 Bcf from the previous week. Current stocks are 375 Bcf lower than at the same time last year and 57 Bcf higher than the five-year average of 2,198 Bcf.

Regional breakdowns indicate the South Central region holds the largest volume at 957 Bcf, followed by the Midwest at 480 Bcf. Notably, the Salt subregion within the South Central area saw a net increase of 15 Bcf, while the Nonsalt subregion rose by 24 Bcf. Despite being below last year’s levels, total working gas remains within the five-year historical range, suggesting a stable but slightly tighter supply situation compared to the previous year.

Weather Patterns

United States: Heat is emerging in parts of the U.S., which is a key short-term driver for natural gas demand. In Texas, record-breaking heat with temperatures in the 32-35 ℃ is boosting early air-conditioning use, driving strong power-sector gas demand in ERCOT (the Texas grid). Meanwhile, much of the rest of the U.S. remains seasonally mild (highs in the 15-27 ℃), keeping overall national cooling/heating demand moderate.

Source: https://www.cpc.ncep.noaa.gov/

Forecasts indicate that in the 8–14-day range, Texas may cool slightly from extremes, but the broader U.S. South is expected to stay warmer than normal (widespread 25-31 ℃). This suggests that as May progresses into June, air-conditioning demand will ramp up across the southern U.S., providing upward pressure on natural gas consumption for power generation. On the other hand, if milder conditions persist in northern states, residential heating demand will remain low (late-spring heating is mostly over), somewhat offsetting the bullish impact of Southern heat. Overall, weather forecasts point to a near-term demand uptick primarily in cooling demand, which could lend support to gas prices if high temperatures materialize as expected.

Source: https://www.cpc.ncep.noaa.gov/

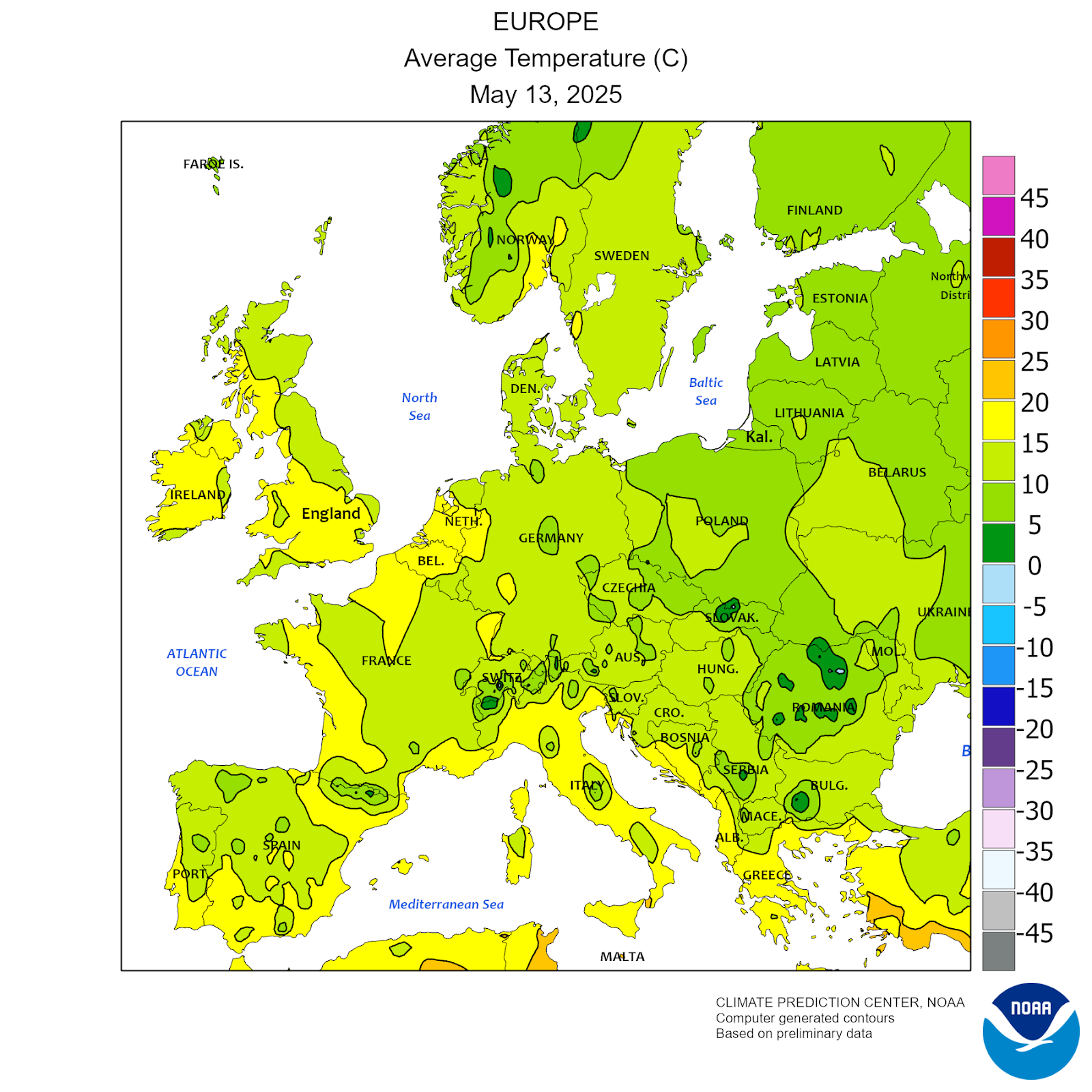

Europe: In Europe, the spring shoulder season typically brings lower gas demand; however, recent weather-related factors are creating undercurrents that could affect gas consumption. Thus far, Europe has not experienced a major early heatwave (cooling demand remains relatively low), and the winter heating season has ended. Mild spring temperatures mean little heating demand, but a different weather influence is at play: unusually low wind speeds and a lingering drought in parts of northwest Europe have reduced renewable power output. Weak wind and low hydropower generation (due to below-average hydro reservoir levels) have forced European utilities to burn more gas for electricity than they otherwise would.

Source: https://www.cpc.ncep.noaa.gov/products/JAWF_Monitoring/Europe/temperature.shtml

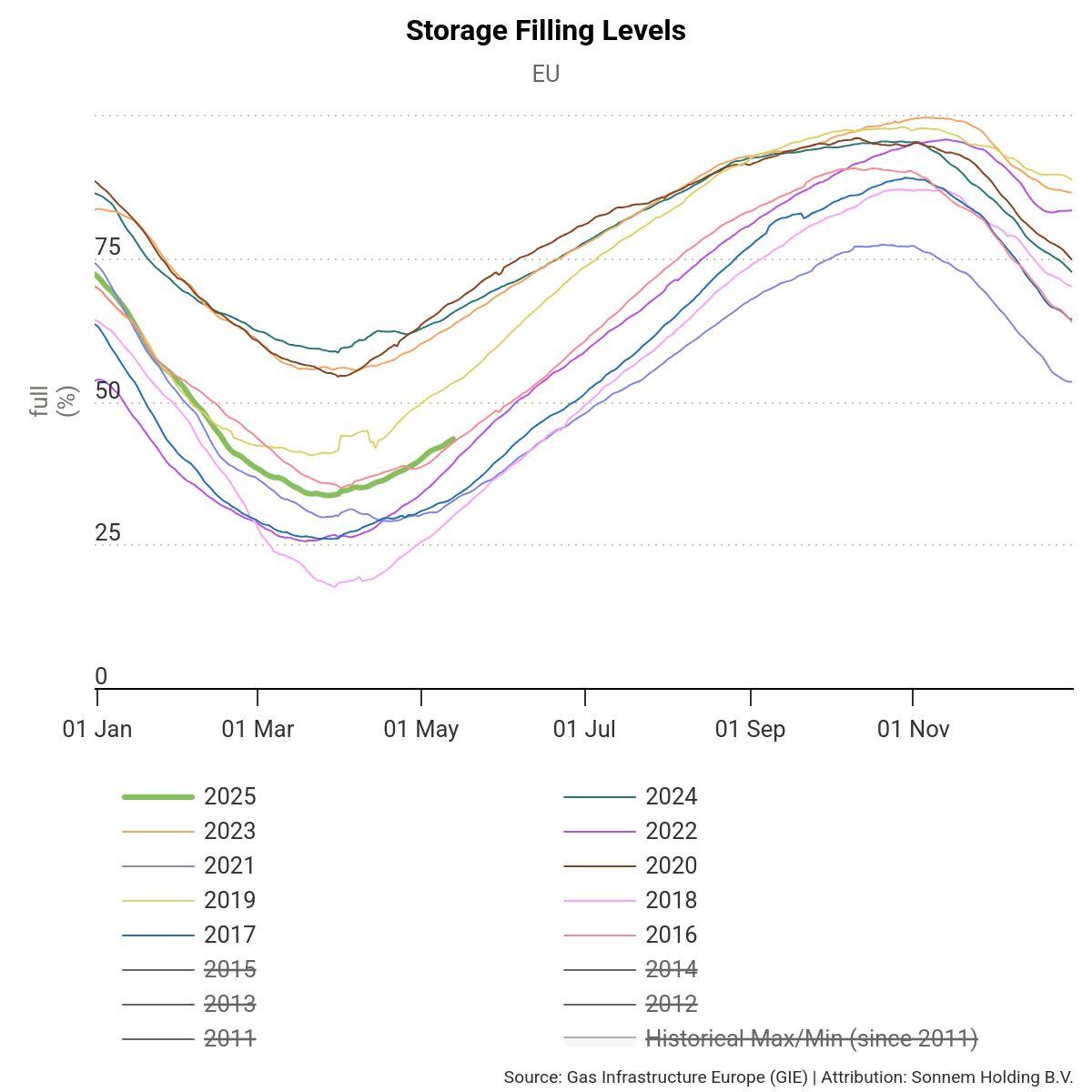

European gas storage levels

Europe exited the winter season with gas storage at its lowest level since 2022, after a colder winter and reduced wind/hydro power output led to a faster drawdown. As of late April, EU storage was about 39% full, roughly 33% below the level at the same time last year. Now EU storage is about 43%, in line with typical levels for this time of year. However, the upcoming air conditioning season poses the usual upside risks for gas demand. If early summer turns hotter or renewable generation remains below average, gas consumption for power generation could rise, tightening the European and global gas markets. While storage is currently adequate, weather patterns and renewable output remain key variables for short-term gas demand and pricing.

Source: https://agsi.gie.eu/data-visualisation/filling-levels/EU

It’s important to highlight that European storage, while low versus last year, is roughly in line with the five-year average (2017–2021) for spring, so the situation is not as dire as it was during the crisis of 2022.

U.S. Tariffs and Macro-Economic Factors

Trade policy is another factor subtly influencing natural gas markets via its impact on the broader economy. According to a May 12, 2025 Yale Budget Lab report, U.S. tariff levels remain historically high, despite some recent reductions. The average effective tariff rate on U.S. consumers is about 17.8% – the highest since 1934 – even after accounting for a new China tariff deal and other adjustments (it would be ~16.4% after consumers shift purchases, still the highest since 1937). These tariffs, including elevated duties on Chinese imports and certain metals, have raised the overall price level by roughly 1.7% in the short run, acting like an inflationary tax on households. In turn, higher consumer prices and retaliatory trade measures weigh on economic growth; the report estimates 2025 tariffs will shave about 0.7 percentage points off U.S. real GDP growth.

For natural gas, the implications of tariffs are indirect but notable. A drag on GDP growth can temper industrial production and power demand at the margin, since industries may scale back energy use amid higher input costs. Tariffs on steel and aluminum, now partially lifted for allies, had raised costs for energy infrastructure (pipelines, LNG terminals) but recent policy tweaks (e.g. removing tariffs on UK steel/aluminum and lowering some China tariffs) should marginally ease those pressures. Overall, the short-term effect of U.S. tariffs is a slight headwind to natural gas demand growth – by dampening economic activity – but this is relatively minor compared to weather and supply factors. If anything, the recent partial rollback of certain tariffs reduces this headwind a bit. Policymakers and market analysts will be watching trade developments because significant shifts (e.g. further tariff reductions or new disputes) could change industrial energy usage and market sentiment. In summary, while weather and supply fundamentals dominate near-term gas price movements, the tariff environment’s impact on inflation and growth is an underlying factor that cannot be ignored, as it influences the broader demand backdrop for natural gas.

Production Trends

U.S. natural gas production continues to operate at near-record highs, which is a crucial factor moderating prices despite rising demand. As of early May 2025, dry gas output is around 104–105 Bcf/day, approximately 4–5% higher than a year ago. This growth has been enabled by past drilling and efficiency gains; however, there are signs of a tempered outlook as producers exercise capital discipline. The gas-directed rig count has fallen slightly (down ~4% from last year), which suggests slower production growth ahead. In the immediate 1–3-week horizon, though, production is ample and steady, ensuring robust supply into the summer. Notably, associated gas from oil drilling (particularly in the Permian Basin) also contributes significantly to supply and may continue to grow as long as oil activity remains strong. High production means the market can better meet spikes in cooling demand or LNG exports without shortages. This supply is a bearish or stabilizing force for prices in the short run – unless there is an unexpected disruption (e.g. pipeline maintenance, hurricane impacts on gas output in the Gulf, etc., which are more of a mid-summer concern).

LNG Exports

The United States has become a critical supplier to the global natural gas market, and record-high LNG exports are a significant factor tightening the domestic balance. Several new LNG export trains ramped up in late 2024, and as a result U.S. LNG export capacity and utilization are surging. U.S. pipeline feed gas deliveries to LNG terminals are currently around 15 Bcf/d, up from roughly 12.5 Bcf/d this time last year. This ~20% year-on-year jump in export volumes reflects both new capacity and strong overseas demand. The Energy Information Administration notes that LNG exports are the main driver of growth in U.S. natural gas demand this year, forecasting a 22% increase in LNG export volumes in 2025 (adding about 3.4 Bcf/d of demand). Indeed, two new export facilities (Plaquemines LNG Phase 1 and Corpus Christi Stage 3) began operations around December, and more (Golden Pass, etc.) are on the way. In the short term (next few weeks), U.S. LNG export terminals are expected to run near full tilt to serve European and Asian markets, especially as Europe refills its storage. This means ~13–14 Bcf/d of U.S. gas production is effectively being pulled out of the domestic market and sent overseas daily.

Europe will rely heavily on imports – both pipeline gas (from Norway and North Africa) and liquefied natural gas (LNG) – to maintain supply for conditioning. High summer refill needs provide bullish underpinning for European gas prices (TTF), which in turn can lend support to U.S. prices via the LNG export linkage. Nonetheless, any supply hiccups or a hot summer could quickly tighten the European market. On the supply side, European domestic gas production (for example in the UK or Netherlands) is in long-term decline and provides limited relief. Thus, Europe’s supply security in the short term is largely about its ability to attract LNG cargoes. Recent news indicates Europe may need to offer competitive prices to secure ~30 bcm of additional LNG this year to fill storage– a signal that global competition for gas will be a factor.

Power Sector Trends

The power generation sector is a major consumer of natural gas, especially in summer, and recent analyses point to growing demand – and some challenges – in this arena. A report by Wood Mackenzie highlights that over the next decade and beyond, the gas-fired power market faces tight supply conditions due to manufacturing constraints for turbines, rising costs, and competition from renewables. They project that about 890 GW of new gas-fired generation capacity could be added globally by 2040 (led by the U.S. and China). While that is a long-term outlook, it underscores a present theme: demand for gas in power generation is strong and climbing. In the near term, the U.S. Energy Information Administration (EIA) expects U.S. electricity demand to hit a record – reaching 4,205 billion kWh in 2025 (vs. 4,097 billion kWh in 2024). Much of this growth is driven by economic activity and increasing electrification, but crucially also by weather (e.g. more extreme summer heat boosting air conditioner usage). For 2025, this implies natural gas burn for power could be very robust, since gas plants often fill the gap when electricity consumption breaks new highs.

However, the power grid’s evolving mix raises reliability concerns that could influence short-term gas usage patterns. The North American Electric Reliability Corporation (NERC) warned in its Summer Reliability Assessment that a “middle swath” of North America (from the U.S. Midwest down to Texas) is at elevated risk of power shortfalls in summer 2025 if temperatures are higher than normal. Essentially, if a widespread heatwave strikes, electricity demand could exceed available supply in some regions. There are a few reasons for this risk:

Rapid Demand Growth: U.S. and Canadian electricity demand has grown by 10 GW in peak load since last summer, more than twice the growth seen the year before. New strains like data centers, crypto mining, and general economic growth, plus ongoing transportation electrification, are pushing summer peaks higher.

Retirement of Fossil Plants: Over 7 GW of fossil-fueled generation (coal and gas) has retired since summer 2024. Notably, the Midwest (MISO) is down ~1.6 GW of gas and coal capacity from last year. These retirements remove some of the around-the-clock baseload supply that could be called upon in a heatwave.

Surge in Solar (and Battery) with Timing Issues: About 30 GW of solar PV and 13 GW of batteries have been added in the past year across North America. While this increases overall capacity, solar is an intermittent resource – it generates in daytime and fades in the evening, which is exactly when hot-day demand often peaks (late afternoon/early evening). NERC specifically flags that ERCOT (Texas) will be tested in the early evening hours when demand remains high but solar output drops off. This is a classic “net peak” issue: as the sun sets, grid operators must fire up fast-ramping sources (often gas peaker plants) to meet the surge in cooling demand.

Wind Variability: In regions like SPP (covering parts of the Plains) and MISO, low wind conditions during a heatwave could further reduce available generation. Wind farms contribute a lot of capacity, but if a high-pressure heat dome settles (often calming winds), their output could disappoint when needed most.

These factors mean that natural gas-fired generators will play a pivotal role in maintaining reliability. Gas peaker plants and combined-cycle units are the flexible resources utilities turn to when demand spikes or when renewables lag. If the feared above-normal temperatures materialize over the next few weeks, we can expect spiking power-sector gas burn as grid operators scramble to meet load. Short-term gas prices could react sharply in regional markets: for example, Texas hub prices might jump on extremely hot days if generators are maxing out. Moreover, if any grid emergencies occur (e.g. conservation alerts or even rolling outages), that can indirectly jolt market sentiment and gas futures, as it underscores tight supply-demand margins.

Conclusion

In the very short term, U.S. natural gas prices are balancing between bearish supply forces and bullish demand catalysts. On one side, record production and increasing storage injections are keeping the market well-supplied. On the other, the combination of looming summer heat, medium European inventories, and relentless LNG exports is providing upward pressure. Barring an extreme weather event, prices are likely to remain in a moderate range, but with a weather-driven skew: a significant heat spike could cause a rapid price uptick.

As of May 15, 2025, natural gas futures at the Henry Hub (US) are trading around $3.46 MMBtu, reflecting a moderate decrease amid forecasts of mild weather and robust storage injections. In Europe, natural gas futures at the TTF hub (Netherlands) are priced at approximately €35.04 MWh, equivalent to about $11.50 MMBtu. This indicates a persistent price premium in Europe compared to the US.