kitiwan mesinsom

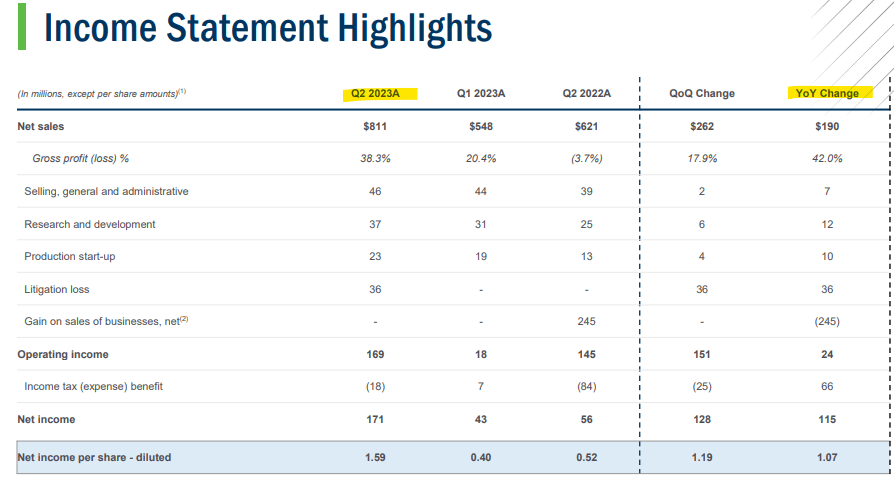

First Solar, Inc. (NASDAQ:FSLR) reported impressive Q2 earnings, with EPS of $1.59 beating out the consensus estimate by $0.65. Revenue of $811 million, up 31% year-over-year, came in $92 million above expectations. The story here has been a ramp-up in solar module production while the company is benefiting from its unique position as a U.S.-based manufacturer.

Indeed, FSLR is set to capture a windfall in clean-energy incentives from the Inflation Reduction Act (IRA) which added a boost to its long-term growth outlook. That was our thesis when we covered the stock in 2022 citing the legislative development as a “game changer“. Our update today reaffirms a bullish call on the stock.

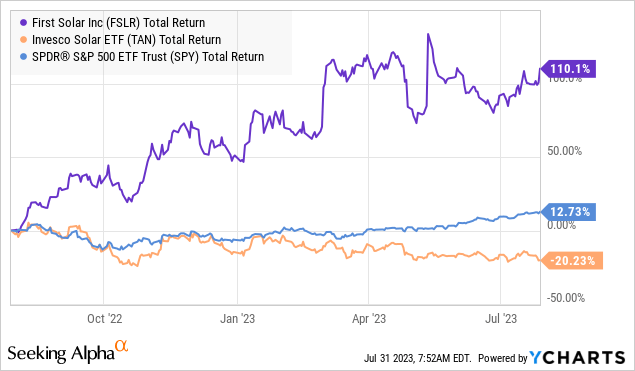

While shares have already been a big winner, more than doubling in value over the past year and something of an outlier amid a more volatile performance in the broader solar industry, we see room for more upside.

FSLR Q2 Earnings Recap

A big theme for First Solar has been the launch of its “Series 7” thin-film cadmium telluride technology modules, recognized for high-performance efficiency. Amid a strong market response supporting sales volumes, management notes that higher pricing is also adding to the top-line momentum.

Even as the older Series 6 technology continues to represent the bulk of the business, the newer modules are driving profitability and represent the future of the company. The impact is evident as the Q2 gross margin at 38.3% climbed from 20.4% in Q1 and helped operating income reach $169 million.

Q2 bookings of 12.2 GW accelerated from 8.9 GW in Q1, taking the year-to-date total to 21.1 GW, leading to a total backlog of 77.8 GW extending through the next decade. An important point here is that while North America represents nearly three-quarters of the total business, First Solar is also advancing internationally.

source: company IR

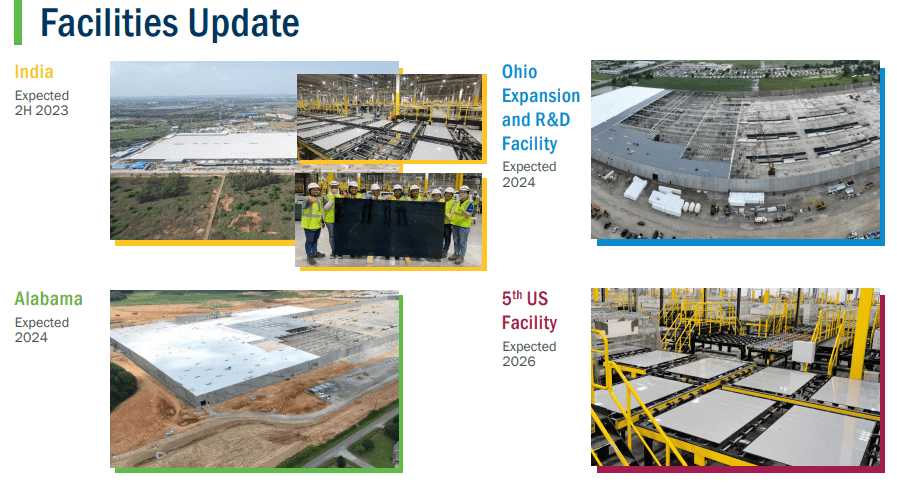

A key update alongside the Q2 earnings release was the company announcement of moving forward with a fifth U.S. manufacturing site, expected to be completed by 2026. According to the press release, First Solar intends to invest upward of $1.1 billion adding 3.5 GW of capacity in 2026.

The idea here is to take advantage of tax incentives within the Inflation Reduction Act (IRA) through 100% U.S.-made components While the location is yet to be determined, the company notes this new facility will be tooled to focus on the “Series 7” thin-film cadmium telluride technology modules recognized for high-performance efficiency.

The expectation here is that from an estimated 16.0 GW annual nameplate global manufacturing capacity by the end of 2023, this fifth facility helps take that total to 25 GW by 2026. This figure also includes the addition of a new site in India expected to be completed still in the second half of this year in addition to an ongoing expansion of its existing Ohio facility and a separate development in Alabama.

The interpretation here is that First Solar management has some confidence that underlying demand conditions are strong and warrant further investments to address what it sees as a significant market opportunity.

source: company IR

What’s Next For FSLR?

The understanding is that First Solar’s operational and strategy initiatives are helping it to consolidate market share at a time when smaller players are being challenged by falling solar panel prices. In other words, efforts the company has made in recent years in terms of R&D and infrastructure are paying off at a time when its operation has reached a mass scale.

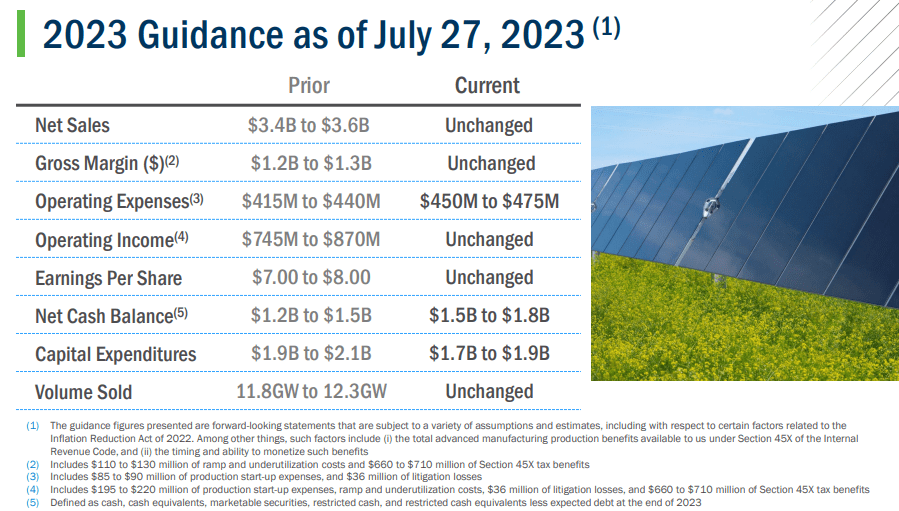

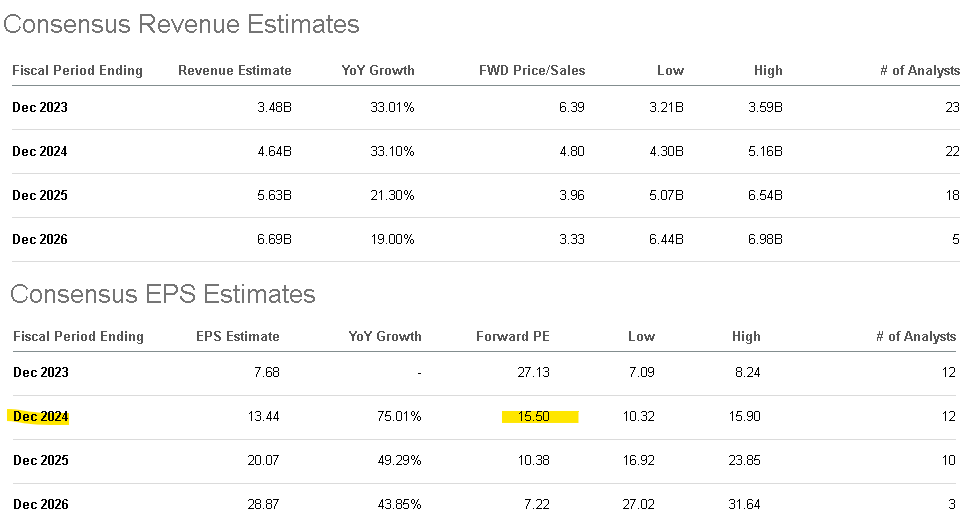

In terms of guidance, management is keeping the 2023 net sales and EPS target unchanged from the Q1 update. The expectation here is for top-line growth of around 33% higher from 2022, while the EPS range between $7.00 and $8.00 reverses a loss of -$2.79 last year.

Again, the major drivers are both the expanded capacity while margins benefit from the improved scale and easing supply-chain disruption that defined 2022. That being said, we believe the Q2 results were good enough to project higher confidence in results out through 2024 and beyond.

source: company IR

According to current market estimates, First Solar is expected to maintain revenue growth above 30% in 2024 with a path for EPS to climb by more than 75%.

Looking out to 2024, we make the case that FSLR is attractively priced and even undervalued trading at just 15.5x 1-year forward expected earnings, in the context of this level of sales growth and accelerating earnings.

source: company IR

FSLR Stock Price Forecast

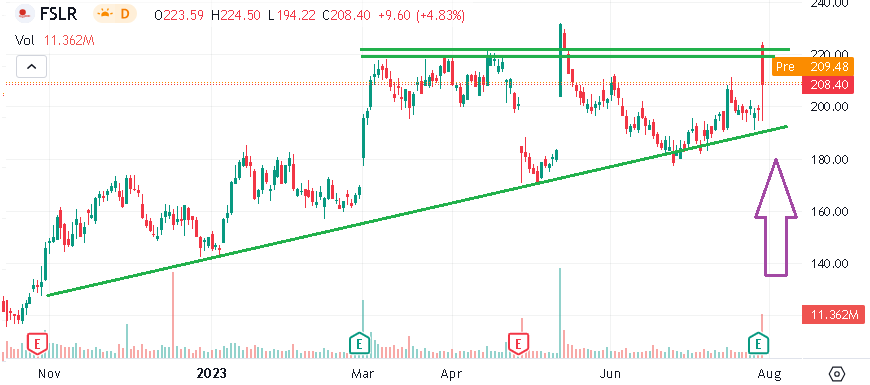

FSLR at around $210 per share has essentially been stuck in a relatively tight range going back to the Q1 earnings report back in March, up against what appears to be an important area of technical resistance.

The way we see it, the latest results were good enough to both reinforce the long-term bullish cash while we can make the argument that the financial outlook is now stronger than ever. By this measure, we see room for the stock to gain momentum and break out higher through the second half of the year.

Here we reaffirm our buy rating with a year-end target for the stock at $300 implying a 22x multiple on the current 2024 consensus EPS.

The way we see it playing out is that the market should continue to reward FSLR as a best-in-class solar name benefiting from solid financial execution and several secular tailwinds including an ongoing transition towards clean-energy technologies. The company’s U.S. manufacturing base can capture a wide range of tax incentives, highlighting its unique positioning within the sector,

source: company IR

Final Thoughts

There’s a lot to like about FSLR which offers investors exposure to high-level sector trends in solar in the U.S. market and the broader clean energy sector. The company benefits from solid fundamentals supporting a positive long-term outlook.

The main risk to consider comes down to company execution. With some lofty targets over the next few years, any setback in terms of the schedule for completing new factory construction or weaker-than-expected sales trends would undermine the outlook. Similarly, the possibility of a deteriorating macro environment could drive renewed volatility in the stock.

{kind=link}