kitiwan mesinsom/E+ via Getty Images

Investment Thesis

First Solar (NASDAQ:FSLR) is a key player in the energy transition. The stock isn’t that cheap, but with the tax credits, it can be a rewarding investment.

To put my bull case succinctly, this is a call on whether governments around the world will continue to invest in solar energy as a key energy source away from carbon-intensive energy sources.

If there continues to be an appetite for solar-derived energy sources, and governments continue to be content to keep their wallets open, then First Solar will remain a rewarding investment.

Why First Solar? Why Now?

In my previous bullish analysis, I said,

[…] the bearish thesis facing the stock, [is] that without IRA credits, this company’s profitability rapidly unwinds.

[…] to decarbonize our energy sources, we must replace this energy with something. It’s not good enough to argue that we don’t want carbon-intensive energies.

And that something, I believe, is all energy sources. From nuclear power to solar panels.

I’ll save the discussion of the tax credits and their impact on First Solar’s profitability for later in this analysis. For now, I’m going to highlight the continual demand for renewable energy and how that is translating into increased bookings for First Solar.

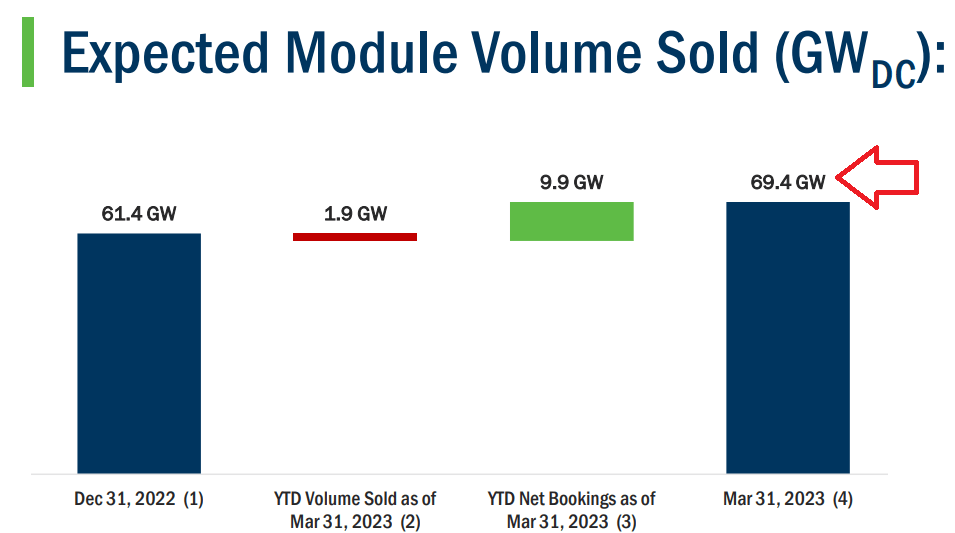

What you see below are First Solar’s bookings at the end of Q1 2023:

FSLR Q1 2023

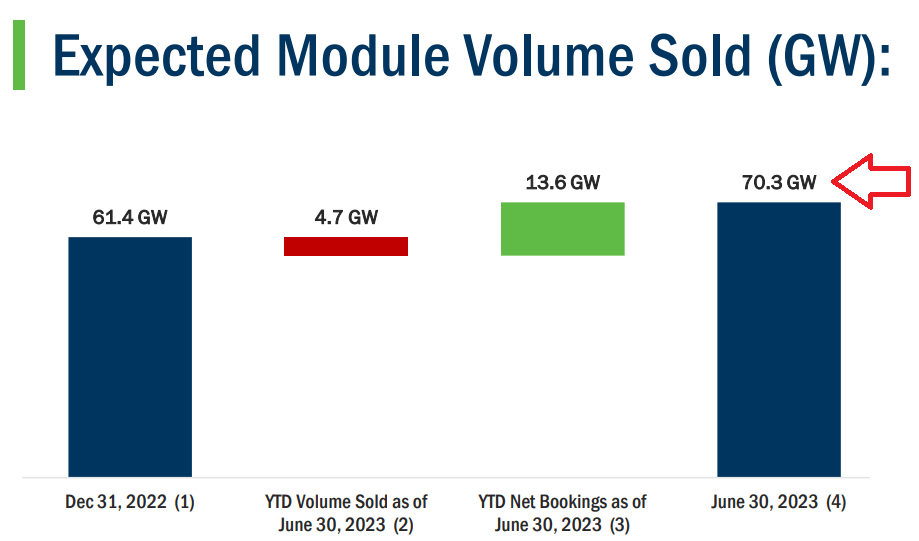

You see 69.4 GW of bookings at the end of Q1 2023. And next, you see First Solar’s bookings at the end of Q2 2023:

FSLR Q2 2023

Between the quarters, the increase in First Solar’s bookings was rather muted, at about 1 GW.

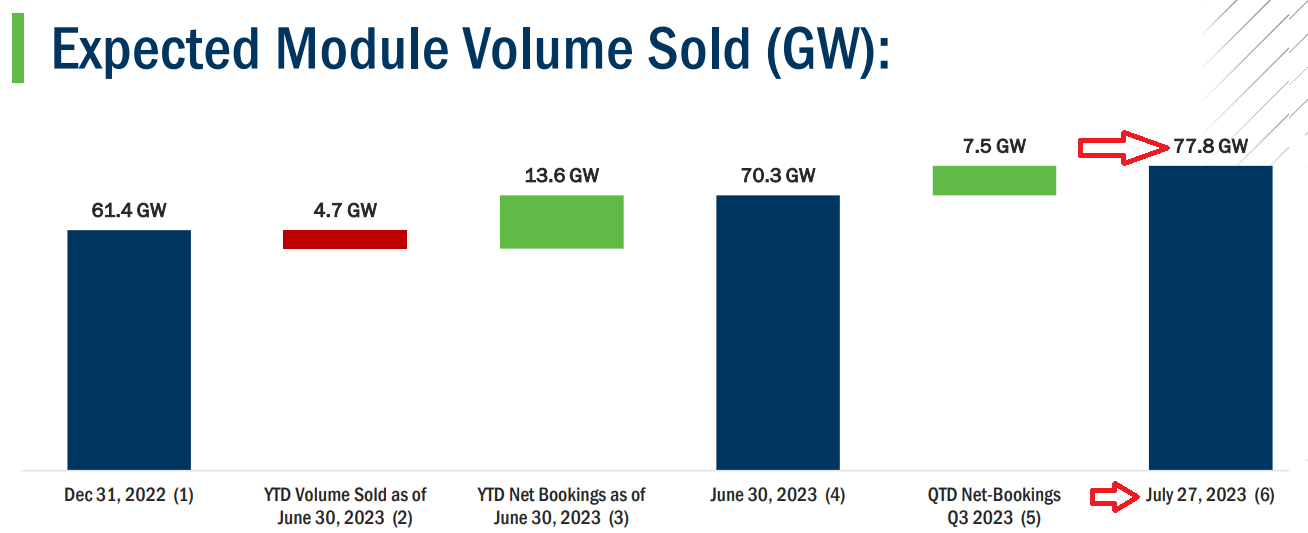

Of course, by the time it reported its Q2 earnings results, First Solar had succeeded in getting a new batch of orders, that helped First Solar put out a more bullish earnings call than would have otherwise been the case.

FSLR Q2 2023

The point I’m making here is that bookings can be more lumpy than we may otherwise perceive from the outside and it’s something to keep in mind.

Yes, there’s plenty of demand for thin film photovoltaic (“PV”) modules, but the growth in demand is bumpy and unpredictable.

Furthermore, anecdotally, I wonder whether with natural gas prices so low right now, this is tempering some enthusiasm for PV modules? After all, First Solar is not only having to compete with other energy sources.

Beyond the alternative energy sources, First Solar also has substantial competitors in the US that are able to offer largely competing technologies.

Consequently, putting aside investors’ strong affinity for First Solar, First Solar wasn’t able to upwards revise its full-year outlook.

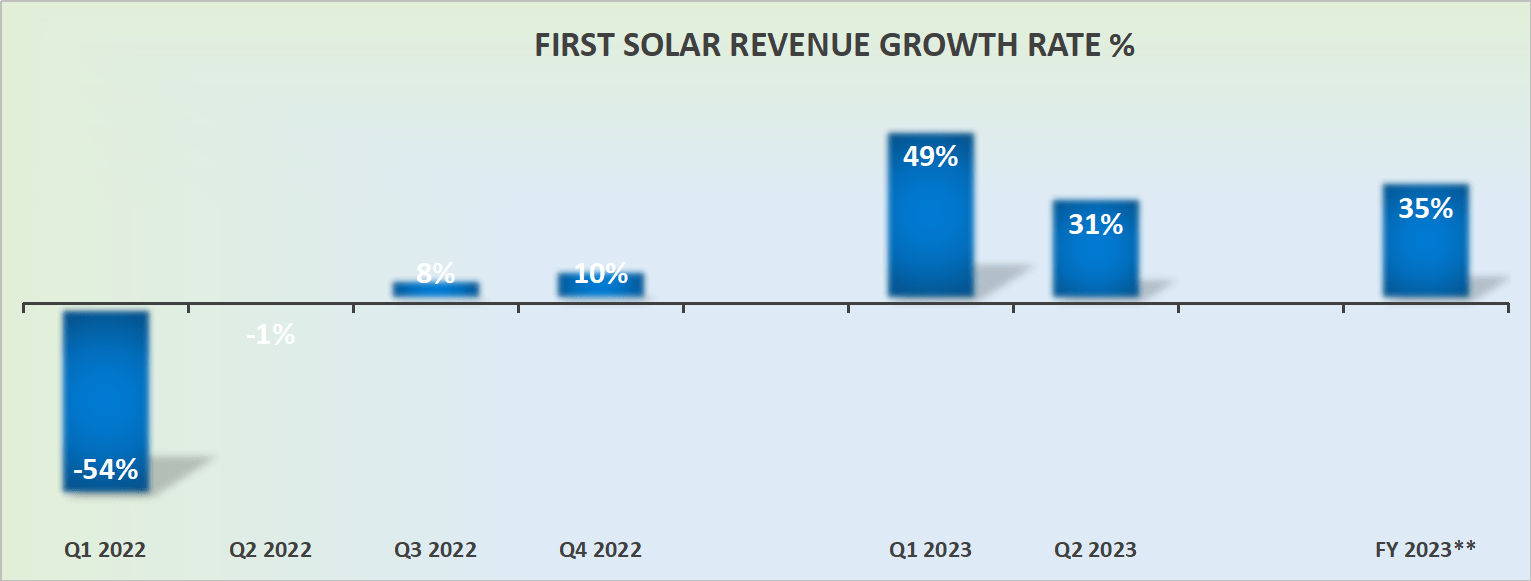

Revenue Growth Rates Continue to be Alluring

FRST revenue growth rates

As touched on already, First Solar didn’t upwards revise its full-year outlook. For a company that has in the past been extremely aggressive with its forward guidance, First Solar’s revenue outlook for the remainder of 2023 hasn’t changed since the start of the year.

After all, it’s not just me being supercilious, you can see below that investors’ expectations for First Solar are meaningfully higher than those of its peers:

All that being said, there’s no doubt that First Solar’s guidance for +30% CAGR is nothing to be dismissive over either. This is a company that appears to be very well-positioned to embrace the growing demand for PV technology and is very well-placed to benefit from various support programs being offered.

Profitability Profile Benefitting From Support Programs

Here’s a quote from the earnings call,

Gross margin was 38% in the second quarter compared to 20% in the first quarter. This increase is primarily driven by the increase in module ASPs [pricing], lower sales rate costs and higher volumes of modules produced and sold in the U.S., resulting in additional credits from Inflation Reduction Act.

There was a massive jump in gross profit in the quarter, from 20% in Q1 to 38% in this current quarter. And a substantial contributor to this jump in profitability comes from tax credits, with $155 million of such credits recognized in the quarter.

And that’s the battleground between bulls and bears. Put another way, a figure that reached 18% of First Solar’s revenues is in the form of government support schemes. If those government support schemes for whatever reason don’t extend beyond the next US election, that could meaningfully change this company’s prospects.

Moving on, First Solar appears cheaply valued at 26x this year’s EPS, but keep in mind that First Solar has substantial capex needs. Yes, the business is growing at a rapid rate on the top line, but its capex needs are coming in at approximately twice its government-supported underlying profitability.

Again, this doesn’t break the bull case, but instead, it’s something to consider when it comes to investing in First Solar.

The Bottom Line

I see First Solar as a key player in the energy transition. While the stock may not be cheap, it has the potential to be a rewarding investment due to tax credits.

The bullish case for First Solar is based on whether governments worldwide will continue to invest in solar energy as a clean alternative to carbon-intensive sources. If the demand for solar energy persists and governments remain committed to supporting the industry, First Solar will likely remain a profitable investment.

The company’s bookings have shown steady growth, and its revenue growth rates are alluring. However, the profitability heavily relies on government support programs, and any changes to these schemes could significantly impact the company’s prospects.

Despite some challenges, First Solar seems well-positioned to capitalize on the increasing demand for PV technology.

{kind=link}