EGT

Ecopetrol S.A. (NYSE:EC) is a buy based on a discounted cash flow analysis with assumptions such as sustaining its current financial results, a discount rate of 8 %, and a terminal multiple of 10. It is also uniquely positioned to benefit from increases in not only the oil price but also the Colombian Peso versus the U.S. Dollar.

Introduction to Company

Ecopetrol S.A. is the modern successor to the national oil company Empresa Colombiana de Petróleos funded in 1951. Today, it functions as an integrated oil company, meaning it has activities in all areas of the oil and gas sector from exploration to refining. Today, the Republic of Colombia is the majority shareholder with 88.49 % of shares outstanding. Although most of its operations are situated in Colombia, it also has biofuel businesses in Brazil, Mexico, and the United States.

The Oil Market

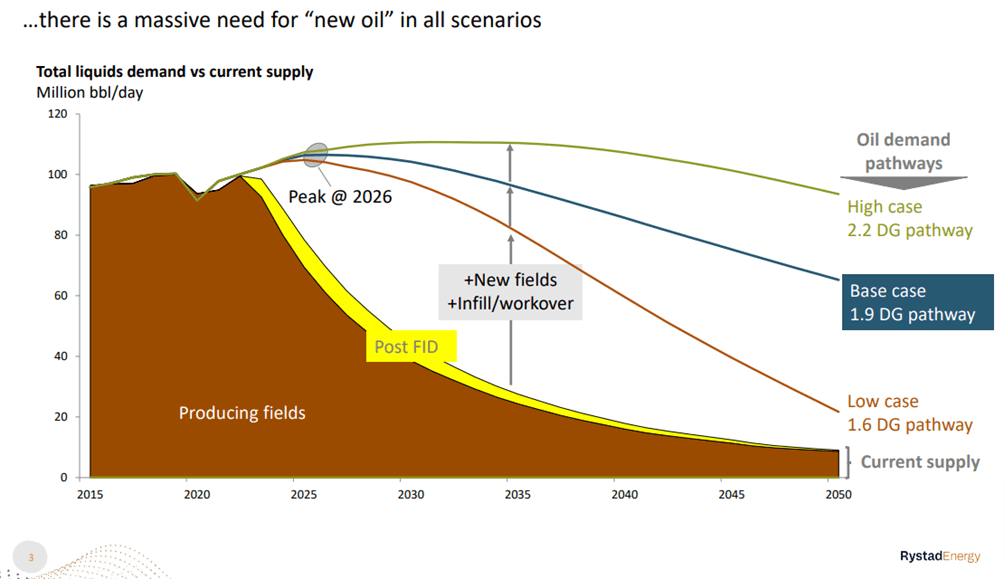

Rystadenergy.com

As can be inferred by the above chart from Energy Research firm Rystad Energy, there is a growing long-term supply-demand mismatch in the oil markets, thus making room for high future oil prices. At least, of course, unless serious innovation in the oil and gas sector makes it possible to increase production or new, low-cost reserves are found. As both of these will take large amounts of money and time, there is good reason to think large integrated oil companies like Ecopetrol will have shareholder returns- viable oil prices for at least some time in the coming years.

As American Investors in foreign companies, it is also worth knowing about the latest foreign exchange developments in the relevant currency, here the Colombian Peso.

Tradingeconomics USD COP

As can be seen in the above chart, the Colombian Peso has been strengthening since the end by about 20 % since the start of the year. As Ecopetrol earns the largest part of its revenues domestically in Colombian Peso, this means an investor will experience the best returns with a strengthening Colombian Peso relative to the U.S. Dollar during the investment period.

Latest Financials

Income Statement

Q1 2023 has provided Ecopetrol with favourable dynamics in both the brent oil price (from about 77 USD to current 85 USD) and the USD COP exchange rate. With the current USD COP exchange rate of about 3,920, Q1 2023 revenue is 9.86 B USD or 38,854 B COP. With Q1 2022’s USD COP exchange rate of about 3,800, Q1 2022 revenue was 8.54 B USD or 32,473 B COP. In USD terms, this is a quite large percentage increase of 15.4 % while in COP terms, this corresponds to a 19.6 % increase. These figures result in operating incomes in Q1 2023 and Q2 2022, respectively, of 13,721 B COP or 3.5 B USD and 12,530 B COP or 3.3 B USD, reflecting a percentage increase in the USD figures of 6 % and, in the COP figures, 9 %. While lower growth numbers than the revenue ones, this kind of growth can be considered great for a billion-dollar market capitalization company. All of this resulted In Q1 2023 and Q1 2022, respectively, of Net Income attributable to shareholders of 5,660 B COP or 1.44 B USD and 6,573 B COP or1.73 B USD, meaning a percentage decline of almost 17 % in Net Income in USD terms and a percentage decline of 14 % in COP terms. This is mostly a result of an increase of 4,841 B COP or 1.23 B USD in its Cost of sales.

Balance Sheet

Regarding its balance, the company has a general asset-liability ratio of 146 %, indicating somewhat normal financial health. Regardless, it also has a quick ratio of 0.23 which indicates short-term problems with paying its obligations within a year by its current business activities. The asset-liability ratio suggests that it might be able to add debt instead of diluting shareholders.

Risks

As an investor in Ecopetrol, there are many risks which can have a great impact. Of these include the chances of declining oil prices, a weakening of the Colombian Peso against the U.S. Dollar. Also, technological innovation in not only the oil and gas space but also in other energy sources might make render Ecopetrol’s oil obsolete. Recessions and economic slowdowns are also known to have an adverse impact on not only oil prices but also emerging markets which Colombia is a case of. Because of the reasons outlined in the subsection ‘The Oil Market’, a high oil price for some time is probable.

Valuation

As assumptions for a discounted cash flow valuation model, the 10-year average of the earnings per share, 1.4 USD, will be used as well as a discount rate of 8 % and a terminal multiple of 10. With a growth rate of 10 % in the first 5 years and 6 % in the subsequent 5, this results in a per share valuation of 26.5 USD:

Made in Excel with Data from Quickfs.net

Which, with current share prices of around 11 USD, predicts that Ecopetrol’s shares should rise by 141 %.

Changing the growth assumptions to 2 % annual growth in its eps for the first 5 years and 1 % in the subsequent 5 years results in a share price of about 17 USD:

Made in Excel with data from Quickfs.net

While the last scenario is lot more conservative in its assumptions than the first one, it still projects an increase of 54.5 % in its share price and is much more probable.

Conclusion

In conclusion, allocating a portion of one’s investments to Ecopetrol shares does look like a value opportunity at the moment, although clear risks are associated with this investment, like an unprofitable brent-peso environment which could come with a recession. Nonetheless, oil supply-demand dynamics suggest that economically high oil prices are probable for some time.

{kind=link}