FangXiaNuo/iStock via Getty Images

Over the last several years, the energy transition, as it is called, was seemingly, at a point, mainly the addition of renewables-plus in the time period during the Obama years. But it started earlier than that, with President George Bush incentivizing renewables in 2005, mainly wind at the time but also hybrid and fuel-cell cars. Shale began its ascent and reversed the course of U.S. oil and gas imports from OPEC, Qatar, Caribbean countries, and others.

It’s a very different transition now. The pandemic created new thinking in energy, which was influenced years earlier with the rise of ESG and the goal of net zero. The war in Ukraine shifted the thinking once more toward energy security, which can mean different things depending on the specific country context, its level of development and state of infrastructure. The Inflation Reduction Act legislation, passed in August of 2022 under the Biden Administration, shifted the thinking once again. Energy firms are responding. Exxon Mobil (XOM) just acquired Denbury (DEN), with its carbon capture and enhanced oil recovery capabilities.

But fundamentals are fundamentals and they underly activity to a large degree — basic, boring supply and demand, economics 101. Currently, global oil supply is rising to about 102 m/b/d, by most counts and groups. U.S. production has largely recovered to levels seen before the pandemic.

Hopkins at Seeking Alpha interview Jennifer Warren (Concept Elemental)

Global Energy Dynamics: Macro Context, Recovery, and Global Shifts (Video link)

Analysts suggest an oil price range of $70-90 for the global benchmark Brent for the rest of the year, and that’s not unlike the Hatfield analysis (AMZA) earlier. However producers in a Dallas Fed survey believe in a WTI range of $72-80. Others suggest the true price is higher than $80, and that discovery will be revealed over the next six months to a year.

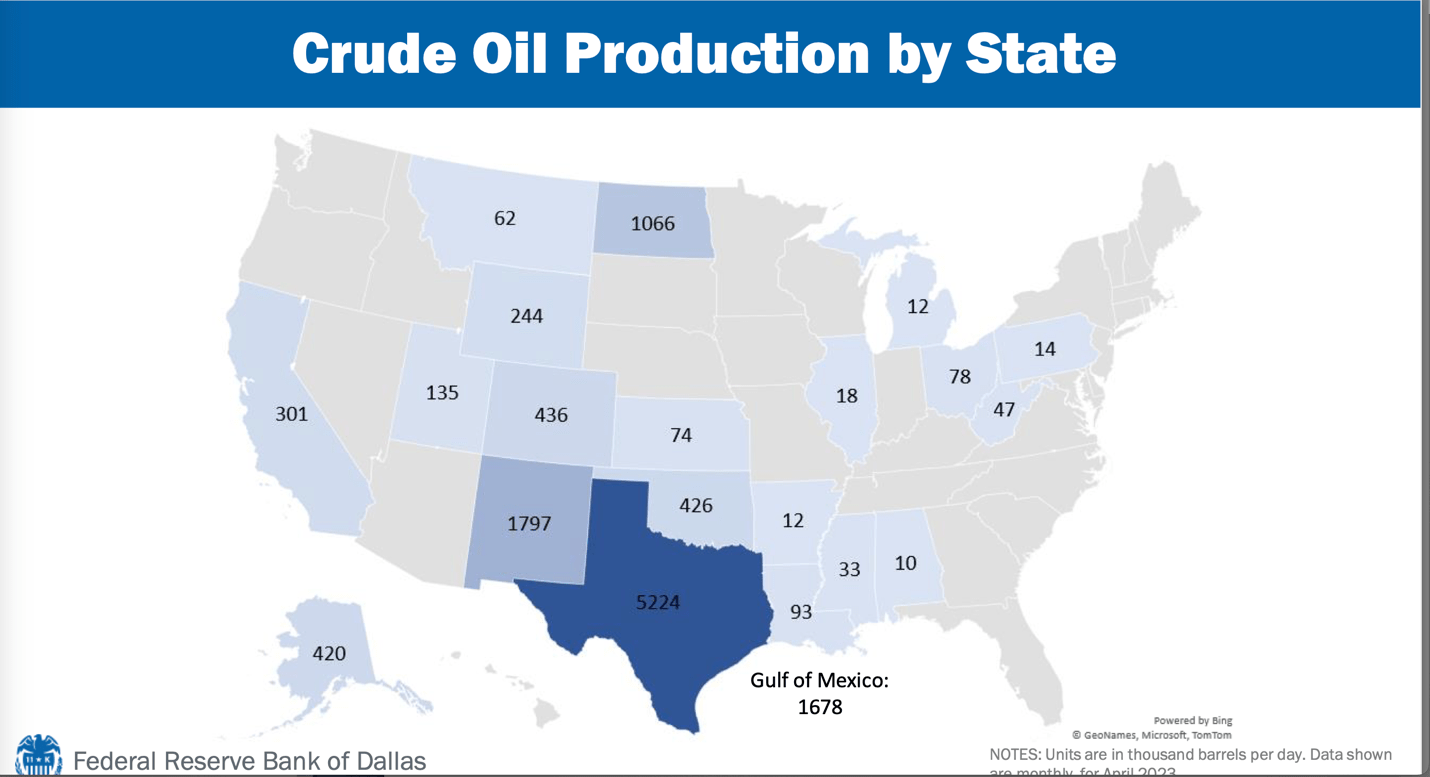

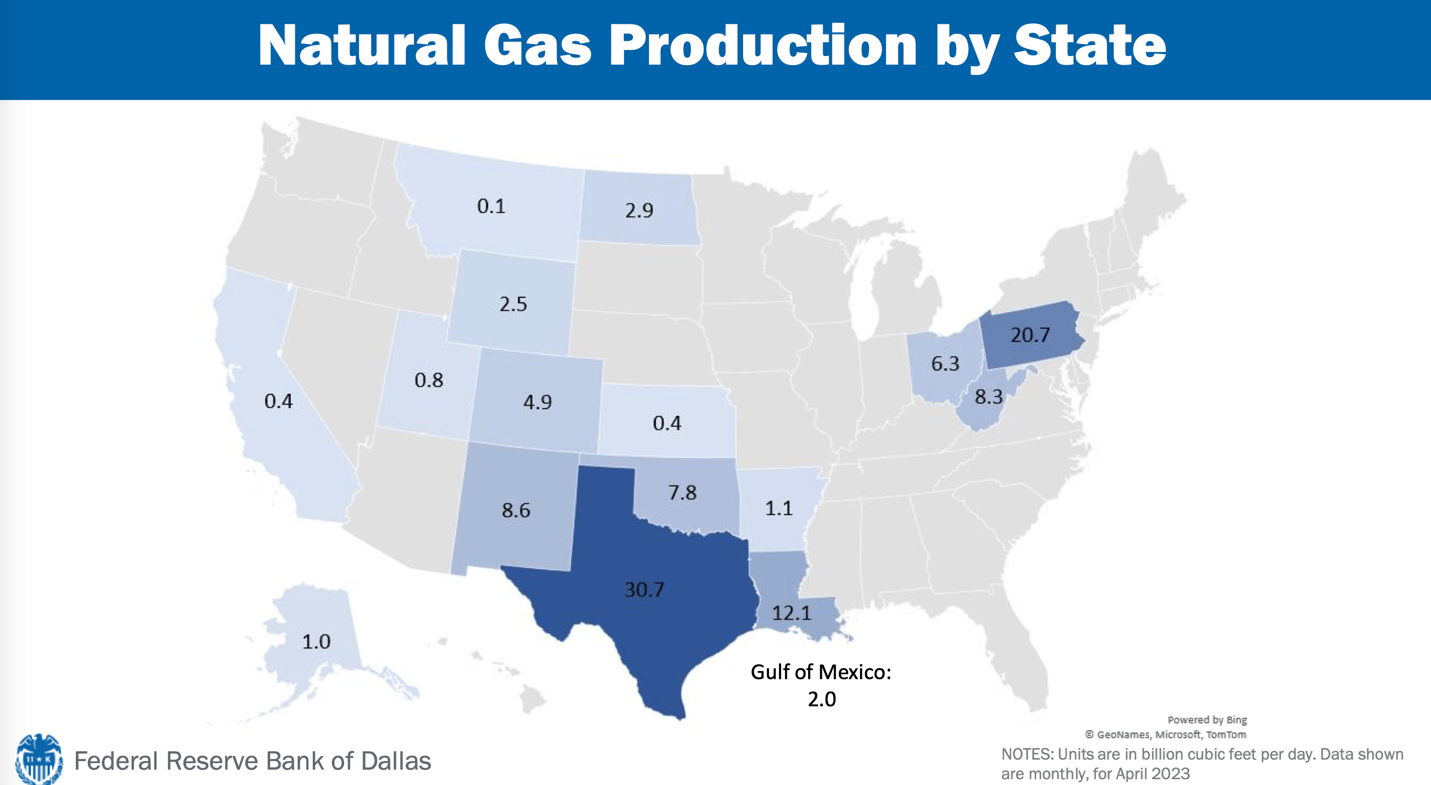

The outlook for U.S. oil and gas production is solid, barring some black swan event. Oil and gas dominates from an energy mix point of view. With regard to U.S. production growth, the Permian is the main driver of that growth. But, other basins play their part. Texas is the largest gas producer in the country too.

US oil production by state (EIA 2023)

US gas production by state (EIA, 2023)

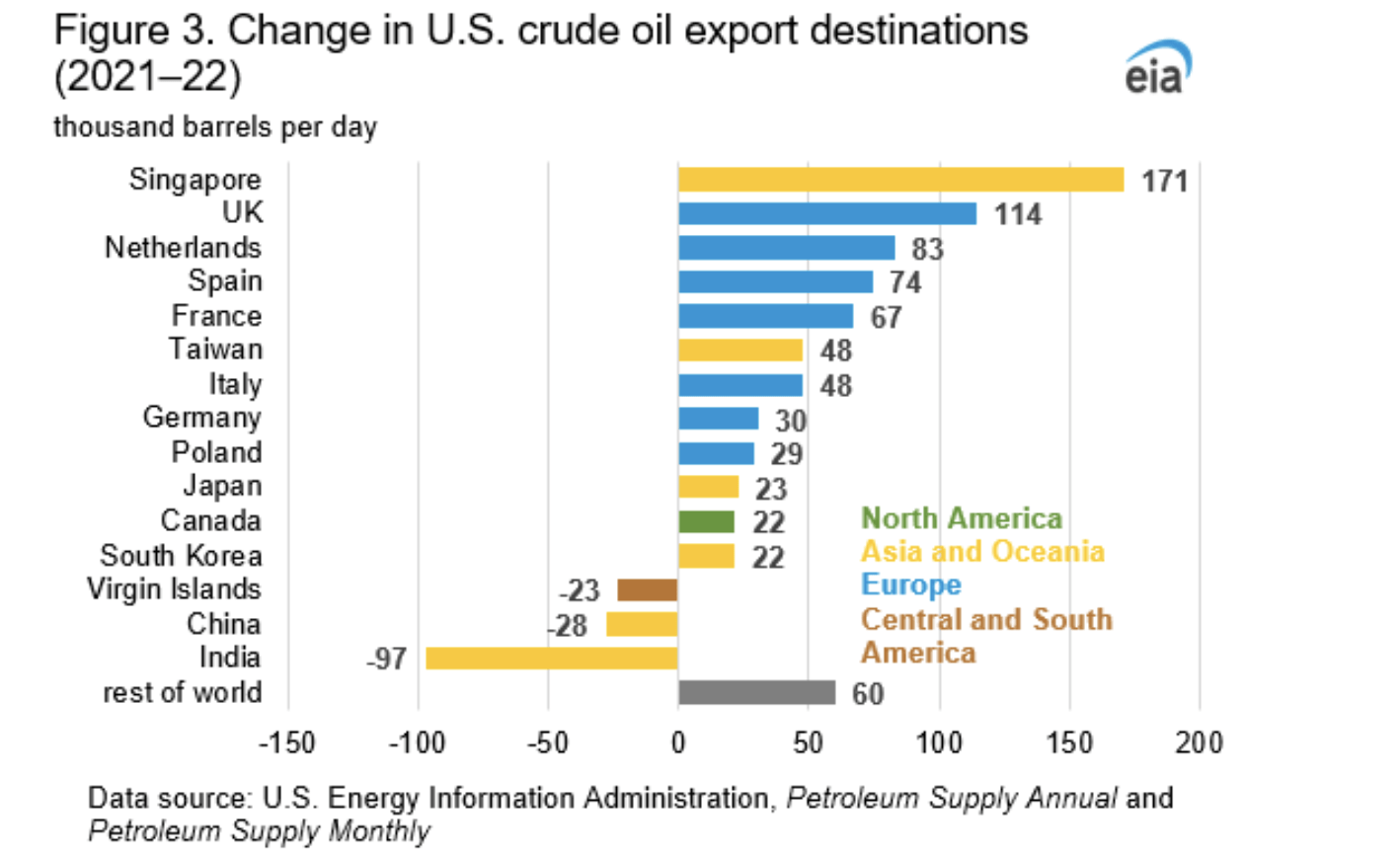

Exports

Since 2015, when the crude oil export ban was lifted, U.S. exports have become important to trading partners. We’re also a top global producer of natural gas, and our LNG exports matter too.

Oil exports by destination (EIA, 2023)

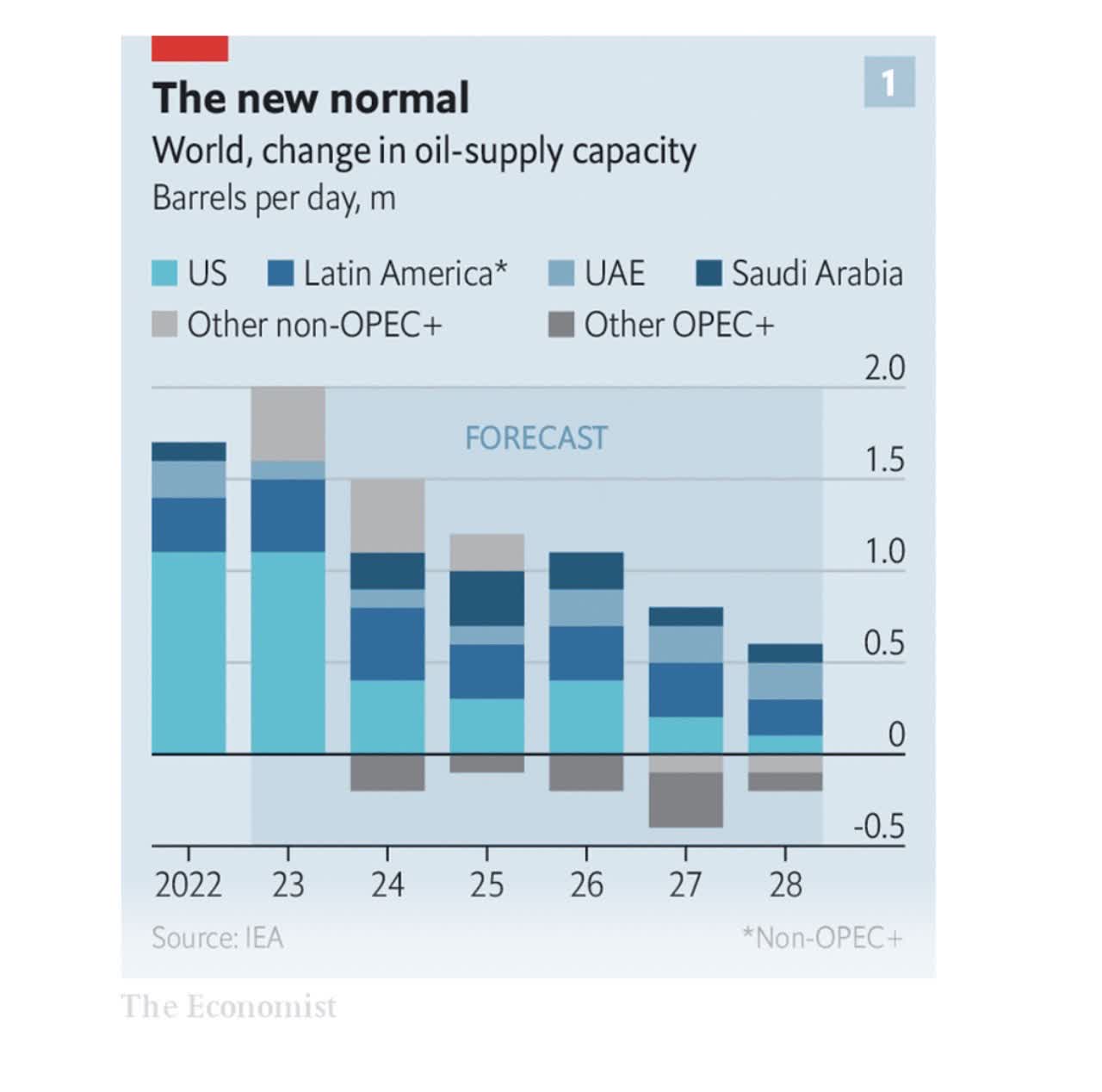

The growth of oil production is slowly starting to plateau. But one cannot make simple assumptions from this. There’s a lot of nuance by country and producer. Interestingly, the Economist chart shows an expected increase in production coming from Latin America. Exxon is a key player in Guyana, which accounts for some of this additional production.

Oil supply capacity and growth (Economist, 2023)

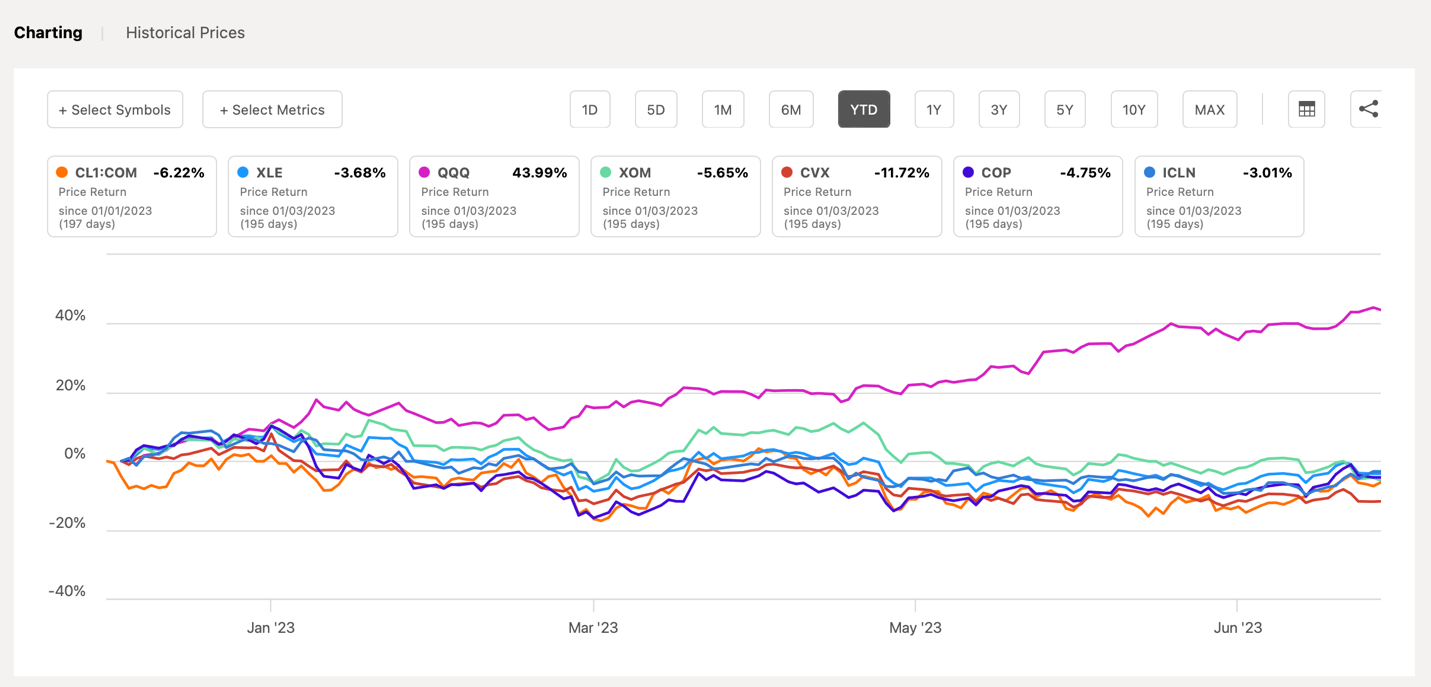

Energy firm performance has been lower, owing to questions of demand, driving the price of oil to a lower price range than a number of analysts and executives believe to be the true price. It’s higher than $65-75. There are a number of reasons. Jay Hatfield suggests that negative sentiment driven by the excitement over the tech mega caps has influenced investors’ stock allocations. And I don’t disagree. Some past articles capture this sentiment, as in the market celebrating the AI (Nvidia’s ascent) day.

The Invesco QQQ Trust ETF (QQQ) reflects this too.

Stocks year to date (Seeking Alpha)

The dust is settling some from the initial euphoria. Many firms continue to leverage AI opportunities and offerings, and marketing opportunities. (Many a GenZ coder are “over” the constant hitching to the AI wagon, “expressing exhaustion with the generative AI conversation being inserted in every part of the tech industry.”) Today was legitimate with Microsoft’s (MSFT) announcement about Copilot, mentioned in the AI Day video and article. It’s a real use case, with a real revenue stream and price tag, carefully selected to leverage opportunity.

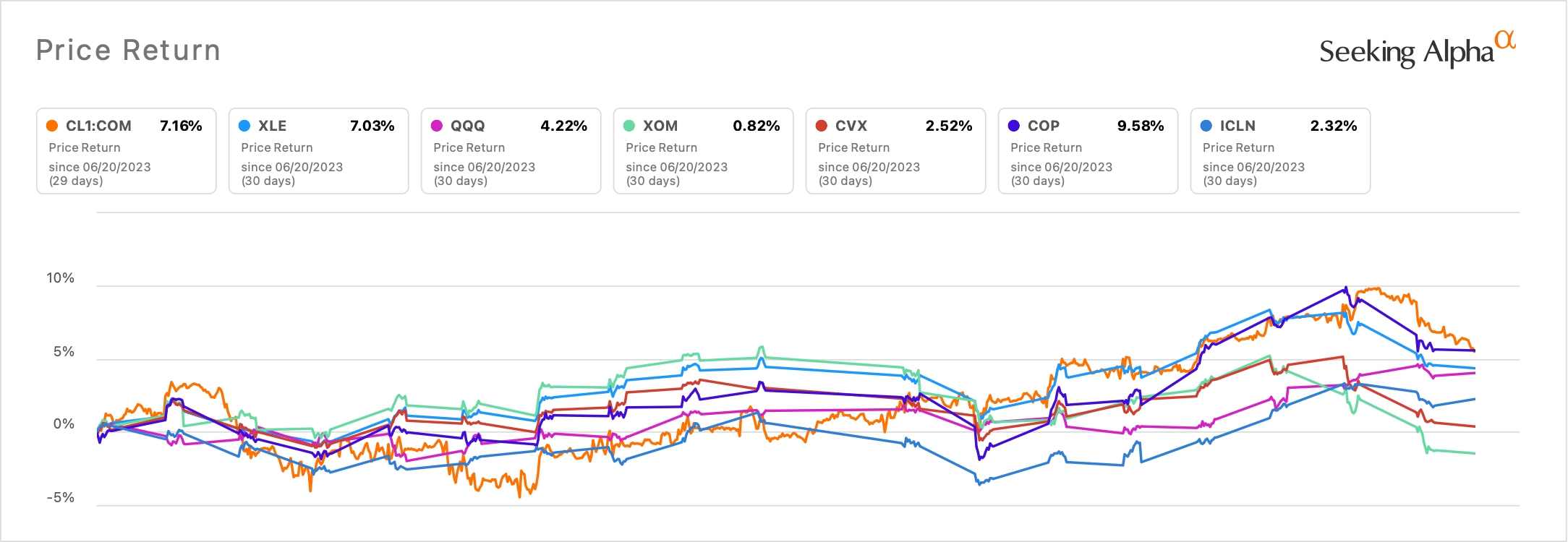

The dynamic still dominates the market’s attention.

Select stocks of July 20,2023 (Seeking Alpha)

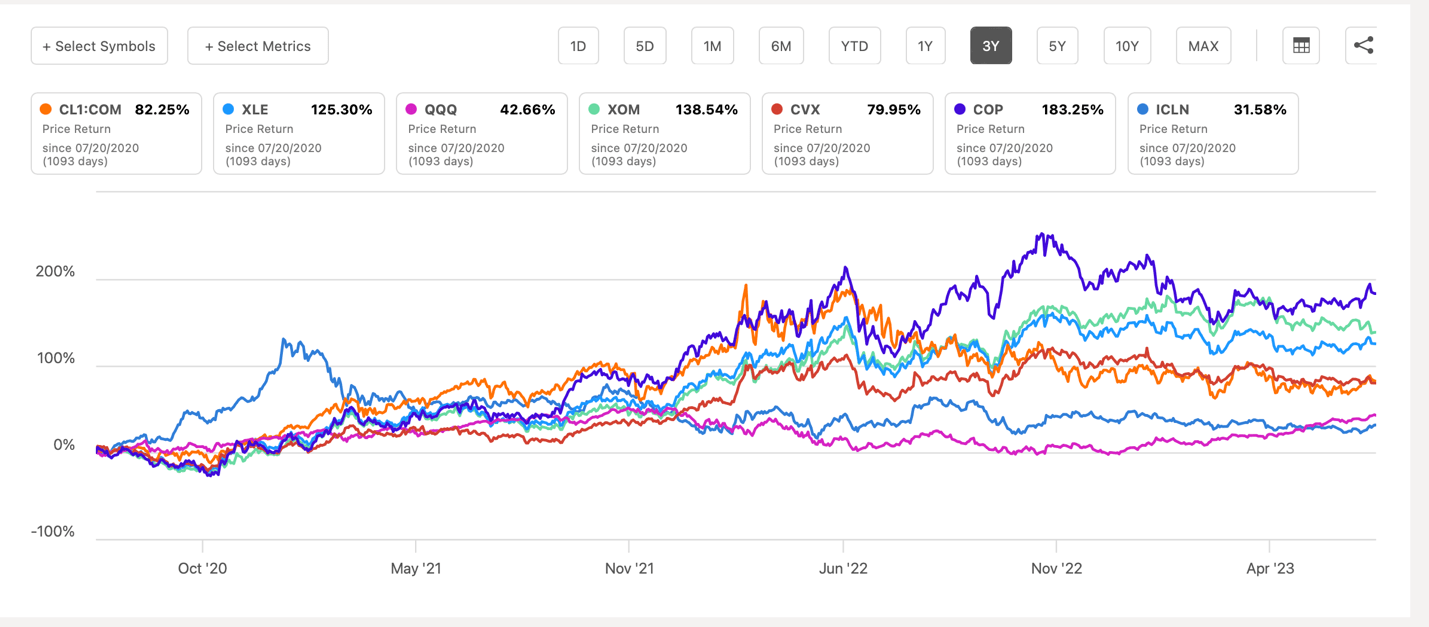

Back to energy, and the representative XLE. The tide will likely shift again for energy once Nasdaq’s rebalancing is over and people simply forget — realizing that tech is a means to an end, and then are reminded once oil prices rise again. A three-year timeframe reveals some interesting energy and oil market dynamics.

Select energy and tech stocks, 3-years (Seeking Alpha)

What has become more clear is that inflation seems to be abating in the U.S. generally. What’s not clear is the continued lag effects and how investment flows are changing. Political rhetoric is destabilizing, but one must look past the noise. Energy has a floor for the moment, an important strength for the U.S. and global economy.

Other references include:

US Energy Powers… (link)

Interview about markets (Concept Elemental)

){kind=link}