Sean Gallup/Getty Images News

Introduction

In 2022, the energy market faced numerous challenges. The conflict in Ukraine, coupled with a lack of investment in the energy sector since 2014, led to a significant increase in energy prices. Consequently, governments intensified their efforts to prioritize energy security. One notable consequence was the shortage of gas supplies in Europe due to reduced imports from Russia, which resulted in a shift towards coal usage and subsequently higher coal prices. Additionally, there was a substantial surge in demand for liquefied natural gas (LNG) from Europe, with approximately 60% higher demand compared to previous years. This increased demand is expected to continue throughout 2023.Golar LNG (NASDAQ:GLNG), recognizing the changing dynamics of the LNG shipping market, made strategic moves to adapt. They exited the LNG shipping market and subsequently sold their remaining Floating Storage and Regas Units (FSRU) to SNAM, an Italian infrastructure company. As a result, Golar LNG shifted its focus towards FLNG operations. By being involved in delivering floating solutions that produce LNG, Golar LNG has positioned itself to capitalize on opportunities that arise as a permanent solution for European energy security is sought after.

Golar business structure

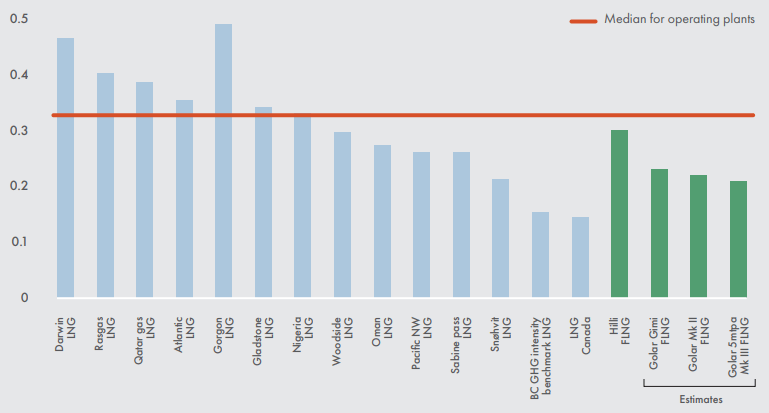

By the end of 2022, Golar FLNG Hilli experienced a significant increase in LNG production, with 50% of its cargoes being delivered to Europe. Additionally, the FLNG Golar Gimi project is set to contribute additional LNG to the market, which is targeted to sail in the third quarter of 2023. Golar has achieved notable milestones, including the development of the world’s first Floating Storage Regasification Unit (FSRU) and Floating Liquefied Natural Gas unit (FLNG). These innovations have allowed new markets to access cleaner energy sources through FSRUs and enabled the capture and monetization of associated gas resources through FLNGs. It is worth mentioning that these solutions have resulted in one of the lowest carbon footprints relative to their size. Figure 1 illustrates that Golar Hilli FLNG, Gimi, Mk II, and Mk III are estimated to have significantly lower carbon footprints compared to operating plants’ median values, while Darwin LNG and Gorgon LNG exhibit the highest carbon footprints.

Figure 1 – Golar’s solutions have the lowest carbon footprints for their size

2022 ESG report

During the first quarter of 2023, Golar successfully repurchased New Fortress Energy’s (NFE) interest in the FLNG Hilli, resulting in an annual increase of $70 million in Distributable Adjusted EBITDA until 2026. However, Golar experienced a decline in Distributable Adjusted EBITDA from FLNG Hilli, dropping from $114 million at the end of 2022 to $94 million in 1Q 2023 due to lower Brent oil and Dutch Title Transfer Facility (TTF). In addition to this, Golar has entered into a Memorandum of Understanding (MOU) with NNPC, the largest oil producer in Nigeria. NNPC has a strategic plan to expand Nigeria’s gas exports and is currently a significant player in Africa’s gas and LNG market. Nigeria is producing 33 million tons of LNG, while exporting 23.3 million tons. As a result, collaborating with NNPC on a project could bring numerous financial benefits for Golar. Furthermore, Golar has made a sale and acquisition that will contribute to cost efficiency. The company sold the older vessel Gandria from 1977 and acquired the newer vessel Fuji from 2004. This acquisition not only reduces re-conditioning costs but also provides increased capacity and larger deck space on Fuji, leading to improved efficiency and flexibility for Golar.

Golar’s financials

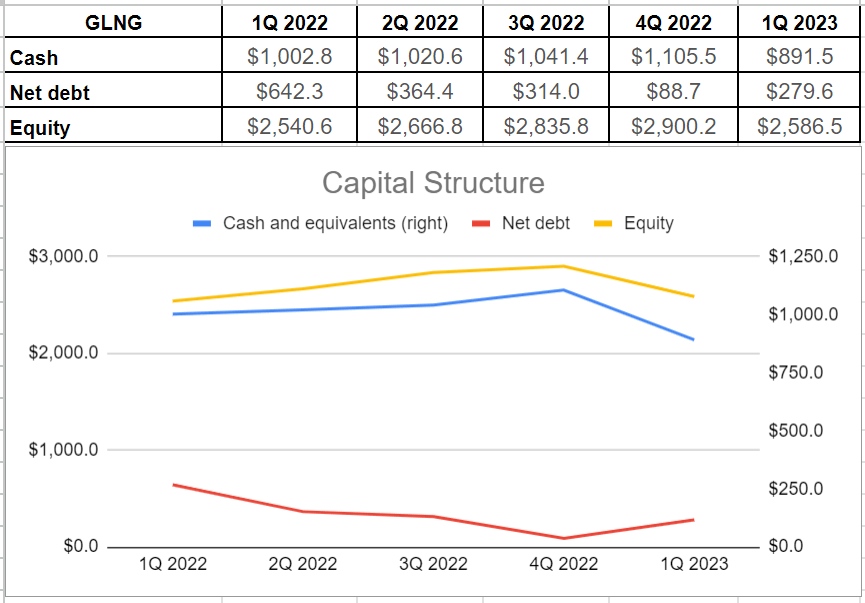

Golar’s cash generation in the first quarter was approximately $891.5 million, which was lower than the $1 billion recorded in the same quarter of 2022. Albeit if we include $113 million of restricted cash, it would be approximately $1 billion. This decline can be attributed to lower commodity prices compared to the previous year. However, the company managed to reduce its net debt level by around 56%, reaching $279.6 million in 1Q year over year, compared to $642.3 million in 1Q 2022. It is worth noting that Golar’s debt level is significantly lower than its equity level of over $2.5 billion. Additionally, Golar achieved other notable milestones such as obtaining credit approval for paying off their existing Hilli deb facility and repurchasing $20 million worth of Unsecured Bonds maturing in 2025. These accomplishments will strengthen the company’s balance sheet and enhance their financial flexibility (see Figure 3).

Figure 3 – GLNG’s capital structure (in millions)

Author

Additionally, Golar’s cash condition has significantly improved compared to the same quarter of 2022. The company achieved approximately $59.8 million in operating cash flow, while incurring $26 million in capital expenditures. Consequently, they were able to generate $33.6 million in free cash flow, which is a remarkable accomplishment when compared to the negative free cash outflow of $40 million in 1Q 2022. The generated free cash flow is sufficient to cover their dividend payment of $0.25 per share for the outstanding number of 107,400,000 common shares, resulting in a total dividend payment of $26.85 million (see Figure 4).

Figure 4 – GLNG’s cash structure (in millions)

Author

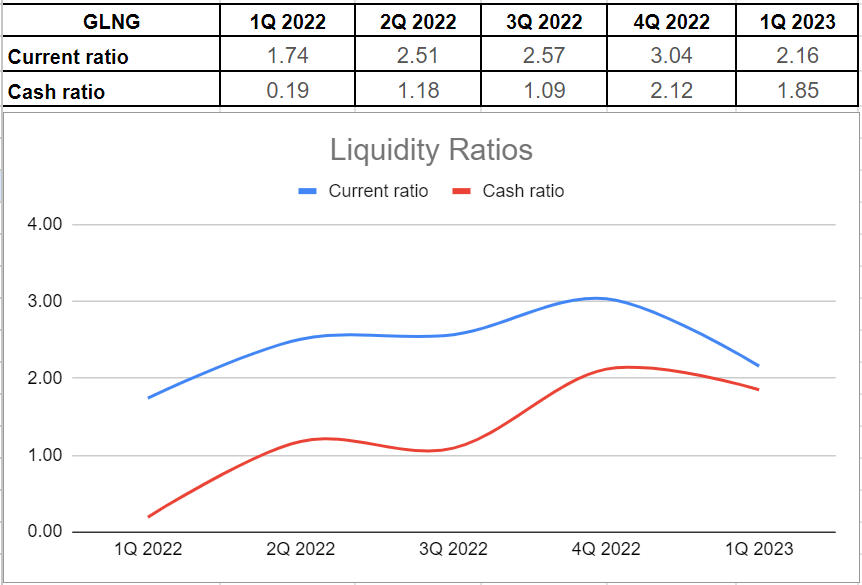

In my previous article on Golar LNG, I analyzed the company’s leverage condition and demonstrated that its low leverage ratios indicate strong solvency and the ability to meet current and future obligations. In this article, I have examined the company’s liquidity condition across the board of its current and cash ratios. Figure 5 illustrates that Golar LNG has achieved a solid and improved liquidity position in the recent quarter compared to the same period in 2022. The current ratio for GLNG has increased by 24%, rising from 1.74x in 1Q 2022 to 2.16x in 1Q 2023. Additionally, GLNG’s cash ratio has shown an impressive surge, reaching 1.85x year over year, compared to just 0.19x in the first quarter of 2022.

Figure 5 – GLNG’s liquidity condition

Author

Market outlook

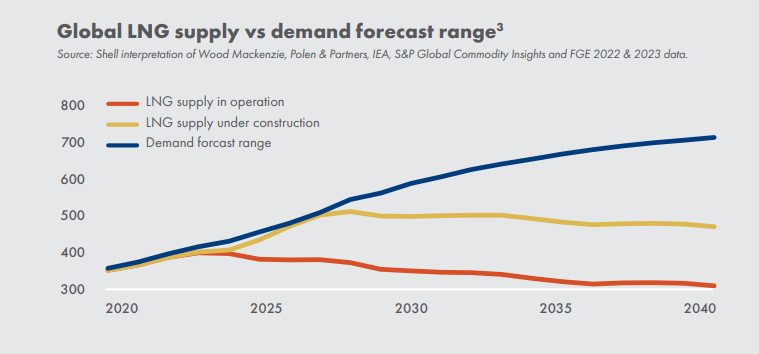

While achieving the Paris Agreement goal remains the ultimate objective, transitioning directly from coal and oil to renewables without incorporating gas poses several challenges. These include the high cost of critical materials, limited supply, manufacturing capacity constraints, and storage issues. Despite the growing demand for renewable energies, it is important to recognize that gas and LNG will continue to play a crucial role in the energy transition as approximately 81% of global energy needs are met by hydrocarbons. It is worth mentioning that Golar has developed a platform that is expected to provide commercial solutions for transforming diesel into gas/EV within the next year. If investments in clean energy do not accelerate in line with established policies, an additional investment of nearly $650 billion per year until 2030 would be required in oil and gas to prevent further price volatility. It represents over 50% increase versus recent years. The implementation of robust policies promoting natural gas usage to mitigate pollution and meet rising energy demands driven by growing populations means that emerging and developing markets in Asia are projected to import more natural gas. Additionally, Europe aims to replace Russian pipeline gas with LNG imports. S&P Global estimates that global LNG demand will surge by 362 mtpa by 2040, surpassing existing or currently under construction supply capacities (see Figure 6).

Figure 6 –

2022 ESG report

Why I might be wrong

The company’s results of operations and financial condition depend on the demand for LNG and FLNGs. The demand for LNG and FLNGs can be negatively affected by various factors such as geopolitical unrest, price, and availability of natural gas, crude oil, and petroleum products, changes in the cost of natural gas derived from LNG relative to the cost of natural gas, insufficient or oversupply of natural gas liquefaction, and increases in the production of natural gas in areas linked by pipelines to consuming areas. Thus, Golar LNG’s cash generation potential may decrease in significant way if the demand for LNG and FLNGs decreases due to the mentioned factors. In such a condition, the company may not be able to obtain new financing, meet its debt obligations, or pay dividends. It is important to know that even if Golar LNG could manage to escape from the negative effect of the previously mentioned political, macroeconomic, and microeconomic factors, the ability of certain parties to satisfy their obligations to Golar LNG could decrease, affecting the company’s financial condition and results of operations in a significant way.

Conclusion

Golar LNG has demonstrated strong performance in the first quarter of 2023. The company’s capital and cash structures are robust, and the management’s efforts to enhance their business operations will provide increased financial flexibility in the upcoming quarters. Furthermore, GLNG’s liquidity condition is solid, supported by a favorable LNG market and successful FLNG operations. Consequently, there is potential for significant improvements in the company’s financial results over the next few years. Based on these factors, I recommend a buy rating for GLNG stock. I welcome your opinions.

{kind=link}