Track your investments for FREE with Simply Wall St, the portfolio command center trusted by over 7 million individual investors worldwide.

-

Energy Transfer (NYSE:ET) raised its regular quarterly cash distribution and outlined a plan for sustained annual distribution growth.

-

The company announced multi billion dollar capital investments tied to pipeline expansions, including the Nederland Flexport NGL project and gas pipelines serving Texas data centers.

-

Management issued a 2026 outlook focused on infrastructure projects and distribution growth, setting out its capital allocation priorities for the next few years.

Energy Transfer enters this phase with its units trading at $17.94 and a multi year return profile that has included an 8.6% gain over the past 30 days, 8.1% year to date, and a 3 year return of 78.5%. Over 5 years, the return is 289.8%, while the 1 year figure shows a 2.8% decline, underlining how timing has mattered for unitholders.

For investors watching NYSE:ET, the combination of a higher regular cash distribution, stated annual growth targets, and detailed plans for large scale projects offers a clearer view of how management intends to balance income and reinvestment. The 2026 outlook provides a framework you can use to track how actual spending and distribution decisions line up with these goals over the next few years.

Stay updated on the most important news stories for Energy Transfer by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Energy Transfer.

How Energy Transfer stacks up against its biggest competitors

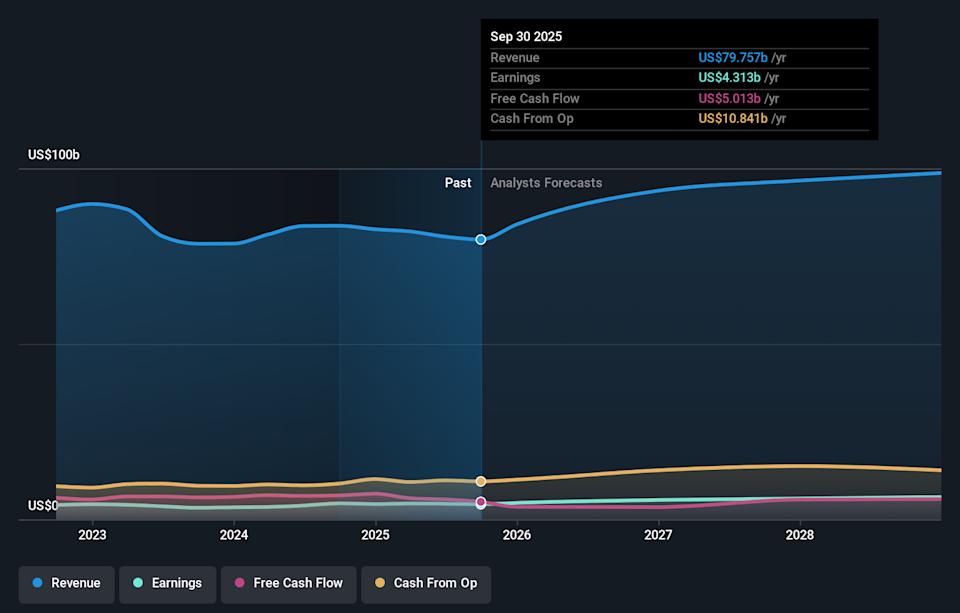

Raising the quarterly cash distribution to US$0.335 per unit, with a stated goal of 3% to 5% annual growth, signals that Energy Transfer is leaning into its income-focused identity while it commits US$5b to US$5.5b of growth capital to pipeline and export projects. For you as a unitholder, the key question is whether these large projects, such as Nederland Flexport NGL expansions and new gas pipelines for Texas data centers, convert into steady fee-based cash flows that comfortably cover both higher payouts and the partnership’s debt load.

This update lines up closely with the existing Energy Transfer narrative that emphasizes fee-based contracts, a massive pipeline footprint and new projects tied to long-term energy and data center demand. The combination of distribution growth targets and a visible project backlog reinforces that story of cash-flow-supported income, but it also raises the bar on execution compared with peers like Enterprise Products Partners and Kinder Morgan, which are often seen as more conservative on leverage and payout decisions.

-

Growing distributions, backed by fee-based assets, may appeal if you are prioritizing high current income from an MLP structure.

-

Multi-year growth projects tied to natural gas, NGL exports and data center demand could support longer-term throughput and earnings visibility.

-

Analysts have flagged that distributions and interest costs are not fully covered by earnings or free cash flow, which can limit flexibility if conditions turn less favorable.

-

Heavy reliance on multi-billion-dollar builds introduces execution, regulatory and cost overrun risks, especially in a competitive midstream space that includes large players like Enterprise Products Partners and Kinder Morgan.

From here, it is worth watching how quickly new projects are contracted, whether distribution coverage improves and how leverage trends as Energy Transfer spends heavily on growth. If you want to put this news into a broader story on cash flows, risks and long-term prospects, take a few minutes to check community narratives on Energy Transfer before making any portfolio decisions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include ET.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com