INTRODUCTION:

India enjoys about 5000 trillion kWh of solar energy with most parts receiving 4-7 kWh per sq. per day. Solar photovoltaic power is being harnessed to combat climate change as it has a potential for 748 GW lessening 3% wasteland areas. The 175 GW by 2022 has been escalated to 500 GW by 2030 which by far is world’s largest expansion plan in renewable. With 60.4 GW India has overtaken Germany (59.2 GW) for the first time.

Major initiatives and policies:

Starting with world’s largest solar park of 30 GW solar-wind hybrids is under installation in Gujarat, it has 5 operational solar parks of 7 GW capacities. In addition, various schemes like, Solar Park Scheme, VGF Schemes, CPSU Schemes, Defence Schemes, canal bank and canal top Schemes, bundling Schemes, Grid Connected Solar rooftop Schemes are encouraged in this regard. Renewable Purchase Obligation is an important policy measure to promote solar.

The total capacity crossing 200 GW to account for 46.3% of the country’s total installed capacity to scale up clean energy infrastructure. India is blessed with about 300 sunny days annually – States like Rajasthan, Gujarat and Madhya Pradesh are power hubs hosting some of the largest solar projects globally – Bhadla Solar Park 2.2 GW (Rajasthan) is the third largest worldwide. The milestones set by India represent its efforts to lessen the reliance on imported fuels and secure energy future to support global climate initiatives.

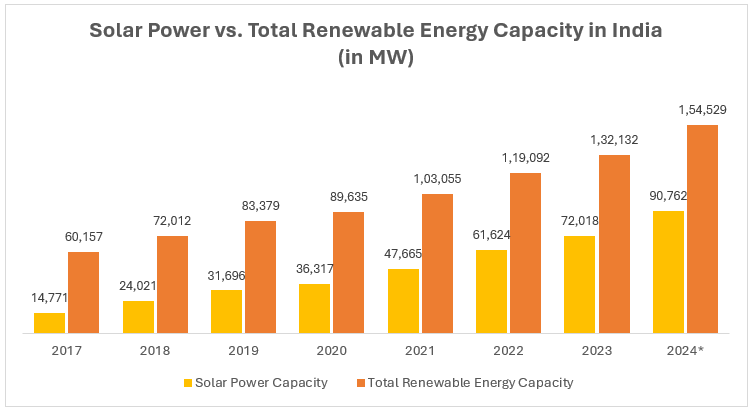

Source: National Power Portal, *- As of September 2024

Policy framework supported by government initiatives, financial incentives and regulatory support have played a major role in the solar growth in India. Large solar parks enjoy financial aid in the states. Competitive tariff is achieved through solar power auctions thus resulting in cost-effective energy sources. Often, the rates have fallen below Rs. 2.50 (US $*0.030) per kWh much cheaper than coal-fired power. Association with International Solar Alliance (ISA) attract foreign investment and shared expertise to its solar industry.

PM Suryodaya Yojana 2024 later rebranded as PM Surya Ghar has benefited the middle-class population – the objective is to install solar panels on ten million homes enabling them to generate their own electricity thus reducing the cost of electricity and to render them self-sufficient (rooftop solar panels receive 300 units free each month). Additionally, they earn between $196 – 207 annually by selling surplus electricity.

Monocrystalline and polycrystalline PV modules offering higher efficiency are deployed in India and are exploring the possibility of bifacial solar modules that generate electricity from both sides. Solar powered agriculture pumps and rooftops further assist in rural and underserved regions. They claim that floating solar helps reducing evaporation and save land resources – 100 MW floating solar in Ramagundam is one of the largest. These technological improvements and advancement enhance solar infrastructure in laying good foundation for a sustainable energy future.

ALTERNATIVES:

In addition to solar, India is forging with a broad mix of wind, hydro, biomass and even emerging option of green hydrogen. Such a diversified approach understandably strengthens energy security and builds resilience to ensure balanced grid in adapting to regional resources and fluctuating demands.

The above policy and technological advancement in the solar sector seem to ensure remarkable growth in the renewable energy sector. Lithium-ion and solid-state batteries (storage) clubbed with micro grids and floating solar enhances integration of renewable into the grid. Digital tools and AI optimise energy management and forecasting for a more responsive and efficient energy system. Intermittency, land acquisition and import reliance present opportunities for innovation and investment in local manufacturing and decentralised solutions.

FUTURE CHALLENGES:

Rare earth elements are characterised by their unique electronic, optical and magnetic properties making them invaluable for solar energy technologies. The 15 lanthanides include lanthanum, cerium, neodymium and europium while scandium and yttrium with similar properties are also often grouped with them. It is believed that it does not go by its ‘Rare’ title as they are in abundance in the Earth’s crust – rarely found in economically exploitable concentrations. This combined with complex extraction processes is attributed to their high market value.

Crystalline silicon solar cells, the most common benefits from addition of Rare Earth Elements (REE) – enhanced efficiency (neodymium used in high-performance magnets are essential for solar tracking systems; europium and terbium utilized in phosphors improves light absorption capability of solar cells. Integration of REEs can also be seen in inverters and batteries crucial for storage and conversion.

China dominates with 60% of global supply as they possess vast reserves of REEs and has developed extensive mining and processing capabilities – they however present concerns about geopolitical risks and supply chain vulnerabilities. Australia, the United States and Russia are the other countries in REEs while India and Brazil are exploring their resources to serve as alternatives.

While recycling (old electronics and batteries) is another option to reduce environmental impacts, innovative technologies are being attempted to improve efficiency of recycling processes. Demand for silicon PV would rise from 39,000 tons (2020) to 8, 07, 500 tons (2040). In addition, Solar PV requires high copper and aluminium along with low cobalt, nickel, lithium and a few more.

Area required for 1 MW of solar is roughly 1.5 acres and at this rate, largest solar park of 30,000 MW in India would occupy an area of 45,000 acres of land. Extending this to projected 175 GW and the potential of 748 GW is in fact, quite considerable.

RESERVATIONS:

I have just considered just two aspects for solar progress in India – Rare Earth Elements and Land. If you look at the quantity of REE needed to achieve the projected and the potential of solar in India, the consumption is unbelievably high – which means the environmental implications of not only just the mining but, recycling/handling the waste generated from them. Secondly, land being already scarce, the land requirement for the same is again quite alarming.

If we extrapolate both these commodities to the global situation, imagine the amount of REE and land already occupied (current establishment) and projected for the future.

This is just with reference to solar only, combine the resources demand for wind and other renewables – we have already overshot one of these resources (air – polluted to the extent that one cannot evaluate) and now, adding land (soil) and water (waste dumping). The big question then is whether the future generation can sustain these burdens on the natural resources and survive healthily.

{kind=link}