- Oil prices have defied the announcement of extended supply cuts from the OPEC+ alliance with brisk declines.

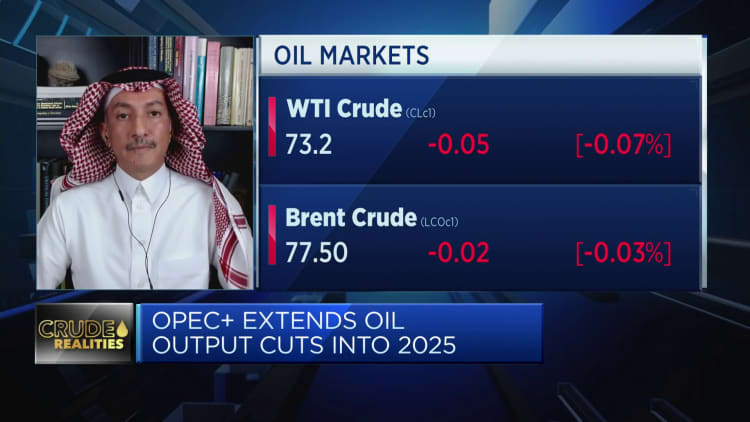

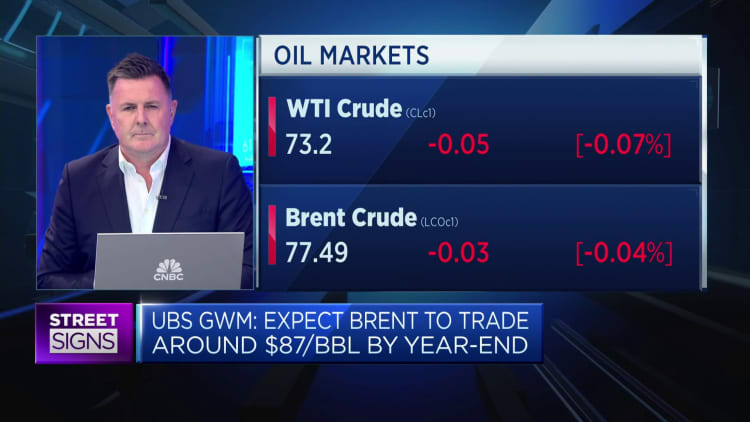

- Oil prices bowed below $80 barrels per day despite this prospect of market tightness, with the Ice Brent contract with August expiry at $77.59 at 11:14 a.m. London time Wednesday, up 7 cents per barrel from the Tuesday close.

- The front-month Nymex WTI contract was at $73.28 per barrel, higher by 3 cents per barrel from the Tuesday settlement.

Oil prices defied the announcement of extended supply cuts from the OPEC+ alliance with brisk declines, with analysts and traders faulting certain trading strategies and the demand picture for the downturn.

“There is a sentiment among traders of changing and repositioning their short versus their long positions, and that is how the price movement is actually giving the signals,” energy consultant Abdulaziz Almoqbel told CNBC’s Dan Murphy on Wednesday. In this case, short positions refer to activity in the futures markets that profits when prices decline, while their opposite long positions cash in when prices move higher over an extended period.

“I would say that what the market is going through currently is going into an oversold, technically oversold market that is pushing the prices down,” he noted.

On Sunday, the Organization of the Petroleum Exporting Countries and its allies — collectively known as OPEC+ — decided to extend its existing formal cuts that were due to end this year, as well as a roughly 1.66 million-barrels-per-day voluntary reduction that also covered the period. These curbs will now carry through into the whole of 2025.

Several OPEC+ members also stretched out 2.2 million barrels per day of additional voluntary cuts from the second quarter of 2024 into the third one, with a view to gradually return these volumes to the market by September 2025 thereafter.

“I think there is a great deal of commodity trading advisors … as well as [algorithms], and the options market, which is a substantially large market of contracts that is influencing the latest price movement,” Almoqbel added.

“If you look at every OPEC+ meeting that was held over the past 36 months, you will notice that following every meeting, there is a downward movement of prices.”

Oil prices bowed below $80 barrels per day despite this prospect of market tightness, with the Ice Brent contract with August expiry at $77.59 at 11:14 a.m. London time Wednesday, up 7 cents per barrel from the Tuesday close. The front-month Nymex WTI contract was at $73.28 per barrel, higher by 3 cents per barrel from the Tuesday settlement.

“Oil prices have fallen by almost USD 5/bbl since last Friday. While some blame the OPEC+ meeting for the drop, we believe other factors — such as the option market—have played a role,” UBS strategist Giovanni Staunovo said in a Tuesday note to clients.

“Prices are likely to remain volatile in the near term. Renewed inventory draws are needed to push oil prices higher, in our view.”

Within oil markets, options are often used as hedging mechanisms to protect against price changes.

Protective “put” and “call” contracts — types of financial derivatives — can set a downside and upside limit for the range in which a price can vary before a position is terminated. Futures hedging can also be applied to defend the value of crude production or of transacted cargoes in the physical market.

The OPEC+ weekend output strategy decision has so far failed to boost prices, given the voluntary cutters’ early announcement of how they plan to reinstate their 2.2 million barrels per day of supplies after the end of the third quarter. The meeting offered a “bearish surprise” to the market and has boosted the downside risk for Goldman Sachs’ forecast that Ice Brent will hit a range of $75 to $90 per barrel, Daan Struyven, head of oil research at the investment bank, told clients in a note.

Also looming large is an uncertain outlook for demand that has put the OPEC Secretariat and Paris-based IEA at opposite ends of a wide spectrum. OPEC’s latest Monthly Oil Market Report of May projects a 2.25 million barrel-per-day increase this year, while the IEA forecasts just a 1.06 million-barrel-per-day demand hike. Demand typically picks up during the summer because of higher gasoline consumption amid a seasonal increase in driving — and the end of maintenance at refineries in China, the world’s largest crude importer.

Yet three crude traders, who could only speak anonymously because of confidentiality agreements, told CNBC that the call on crude from Asia has been low, with one adding that a part of the forthcoming demand increase has already been “borrowed,” as some physical crude volumes would have been carried forward.

“If you look at the latest price movements, you are under the impression that we are in an oversupplied market. However, if you look at the supply restraints and the reroute of dynamic in the global energy supplies, you would clearly understand that this market is definitely not in a surplus,” Almoqbel said. “And so, it really depends on where you want to look, whether you’re focusing on the supply picture or the demand picture to really tell.”

{kind=link}