Oil has seen a lot of ups and downs in the last two years, but following the outbreak of wars between Russia and Ukraine in 2022, and Israel and Hamas last year, prices have also stuck to a tight trading range after short-lived bouts of volatility.

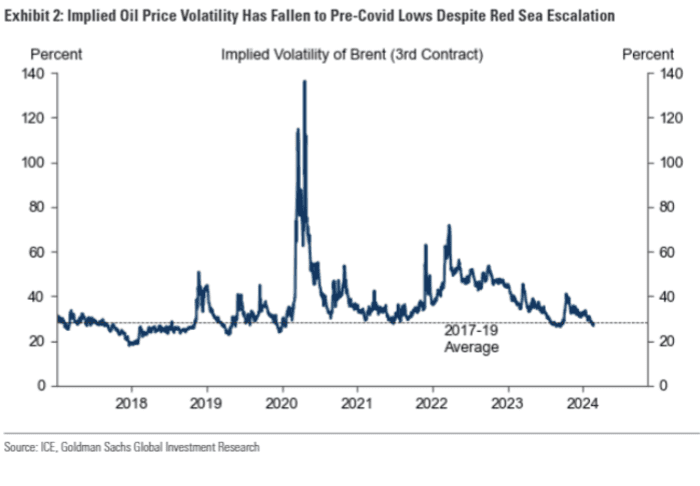

The “muted” swings in global benchmark oil prices, despite wars in the Middle East and Eastern Europe, reflect a modest geopolitical risk premium and the “stabilizing forces of elevated spare capacity and the OPEC put,” said analysts at Goldman Sachs, in a note dated Sunday. The OPEC put refers to the ability of the Organization of the Petroleum Exporting Countries to place a floor under prices by making adjustments to production.

Volatility in Brent oil prices has calmed in recent months.

ICE, Goldman Sachs Global Investment Research

They also attributed the muted price volatility to the “near balance between growth of non-OPEC supply and demand, which both remain robust.”

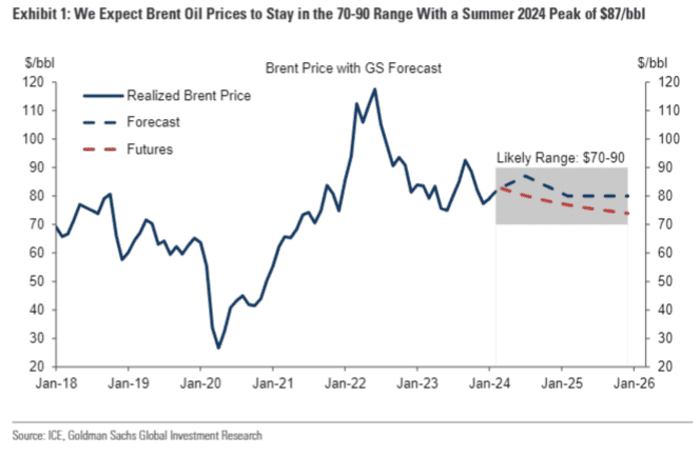

Brent oil prices have traded within a roughly $20-a-barrel range since mid-2022, and more recently, an even tighter $10 range since the start of this year, but the potential for a price breakout in either direction — under the right conditions — remains.

Stuck in a range

So far this year, Brent crude prices

BRN00,

+0.69%

BRNJ24,

+0.76%

have edged up by around 7% as of Monday, trading between a low of $74 and a high of $84.

The geopolitical risk premium remains modest, with only a $2-a-barrel boost to Brent from Red Sea shipping disruptions and unaffected crude production, said analysts at Goldman Sachs.

Read: ‘Fear alone is not enough’ to drive oil prices higher. Here’s why.

Attacks on ships in the Red Sea by Iran-backed Houthi rebels have led to higher costs for shipping an insurance, and longer shipping times, but haven’t resulted in big disruptions to supplies, the analysts have said.

The Goldman Sachs analysts also pointed out that the “OPEC put,” has limited downside risk, while spare production capacity limits upside price risk.

Non-OPEC supply growth, meanwhile, has been “robust” and is likely to “nearly keep pace with solid global demand growth,” the analysts said.

Goldman Sachs expects Brent oil prices to stick to a $70 to $90 price range in 2024 to 2025.

ICE, Goldman Sachs Global Investment Research

Given all that, the Goldman Sachs analysts said they’re sticking to their $70 to $90 Brent “range call” for this year and next, with a likely summer peak this year of $87 and the global oil benchmark forecast to average $80 in 2025.

OPEC+ output

Production cuts by OPEC and its allies, together known as OPEC+, show that the group can set a floor for Brent oil prices at $70 a barrel, wrote strategists at BofA Securities, in a note dated Monday.

At the same time, an increase in spare production capacity to around 5 million barrels a day, due to volume cuts, and substantial non-OPEC+ supply growth over the next few years can help cap oil prices below $100 a barrel, they said.

That means oil prices should stay “anchored near term,” the strategists said, reiterating their forecast that Brent will average $80 a barrel or so this year and next, down from $82 in 2023.

Further out, they see Brent averaging $60 to $80 through 2029, with the oil picture over the medium term not expected to change substantially, they said.

Against a backdrop of slowing global demand, annual non-OPEC supply growth should average 700,000 barrels a day in 2024 to 2029, down from the historical average of 900,000 barrels a day in 2017 to 2022, the BofA strategists said.

Breakout potential

Analysts have pointed a number of factors that could lead oil prices to finally break out of their trading range.

In terms of the potential for oil to break out of Goldman Sachs’ $70 to $90 Brent price range call, geopolitical shocks to OPEC’s ability or desire to deploy its spare production capacity pose the ”sharpest” upside risks, its analysts said.

A longer extension of OPEC+ cuts implies moderate upside, they said, while a sustained drop below $70 would require much weaker demand and a shift in Saudi strategy.

Strategists at BofA said refilling strategic oil reserves could support prices for the oil in the next five years.

The U.S. Energy Department on Monday announced plans to buy about 3 million barrels of oil for delivery to the nation’s Strategic Petroleum Reserve in August. That marked a continuation of its efforts to refill the reserve following a historic drawdown of the emergency reserve in 2022 in the wake of Russia’s invasion of Ukraine.

Looking at global oil inventories, however, government stocks among the Organization for Economic Cooperation and Development industrialized nations remain near the lowest levels in decades, and low government stockpiles “reduce the buffer against upside price risks,” including “sticky inflation” that lifts oil production costs, robust OPEC+ cohesion, and a major slowdown in electric-vehicle sales, strategists at BofA said.

Downside risks for oil prices, meanwhile, include an extended period of structural weakness in global economic growth, “unforeseen” improvements in U.S. shale productivity, and a “faster-than-expected” move away from thermal fuels,” they said.