Last year was, as the English football saying goes, a game of two halves. And just like in an exhilerating 3-3 score draw, 2023 ended much in the same place it started — Europe again has a comfortable buffer of gas held in winter storage and hub prices are testing multi-month lows. So, what does 2023 tell us about where gas and LNG prices might head in 2024, and what are the major factors that could upset the outlook?

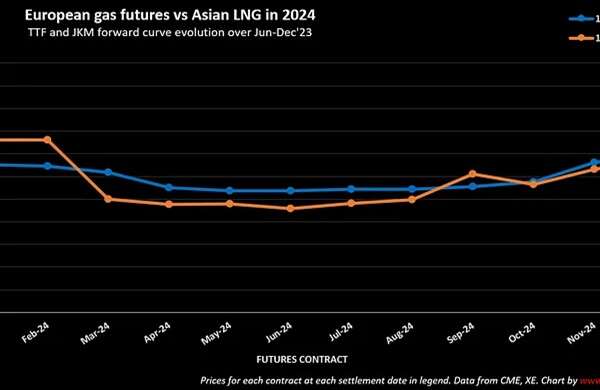

Europe started last year in the midst of a steep correction, with natural gas prices on the Dutch Title Transfer Facility (TTF, the European benchmark) falling from the equivalent of ~$24 per million British thermal units (MMBtu) to less than $7/MMBtu by June. The Japan-Korea Marker (JKM, the Asian LNG benchmark), lagged as it followed TTF down that curve. The reality of Europe’s structurally lower gas demand profile took some time to sink in.

Read entire article at Energy flux.

{kind=link}