The Hydrogen industry is generating significant interest in the US and attracting a lot of capital. Developers are actively building projects in many locations, but some locations, like Texas and Louisiana, have far cheaper forecasted costs of production than others. By using levelized cost of hydrogen (LCOH) calculations derived from the US Department of Energy, National Renewable Energy Laboratory, and Energy Information Administration numbers, we were able to develop some simplified US maps to illustrate the current cost expectations on a state-by-state basis.

We designed the maps to act as a visual guide for relative costs, with states colored from green to red, and low to high LCOH, respectively. The scale of the maps ranges from $1 to $8 per kg of hydrogen and includes data for all 48 contiguous states.

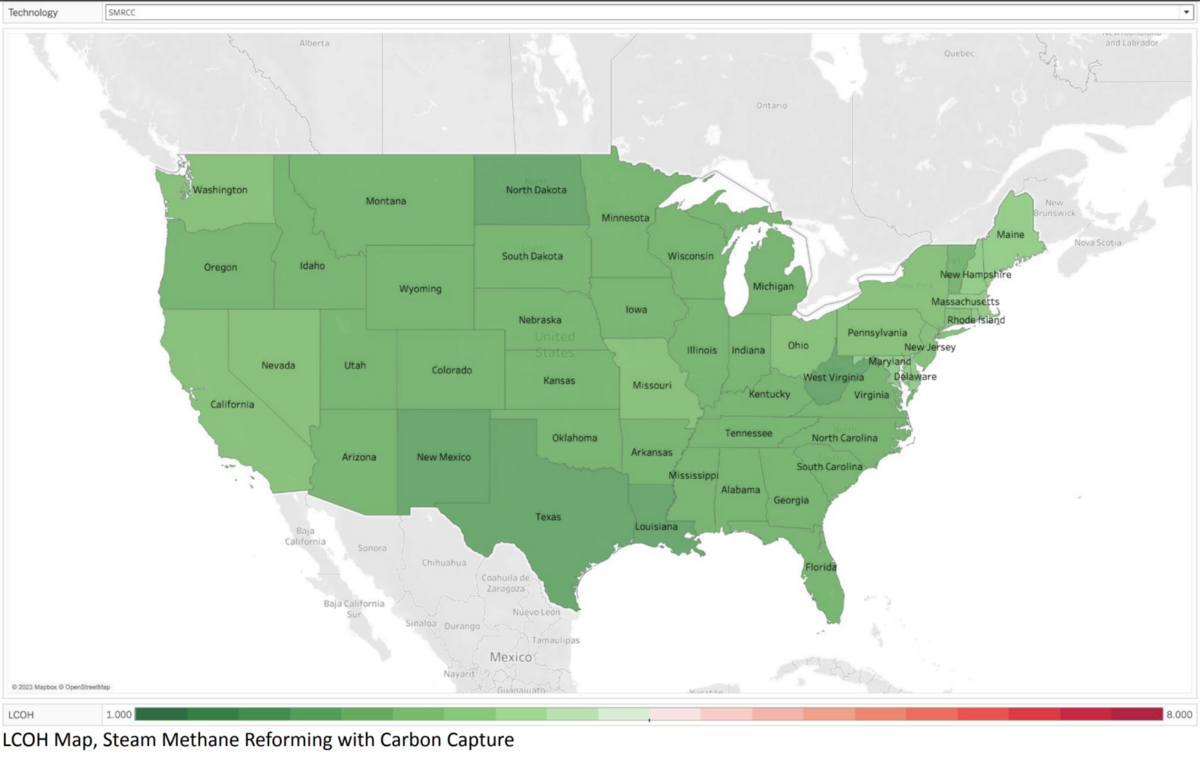

The five cheapest states for electrolysis are Louisiana, New Mexico, Tennessee, Kentucky, and Washington, with LCOH numbers ranging from $3.70 to $4.46 per kg (US maximum is $12.97). The five cheapest states for steam methane reforming with carbon capture (SMRCC) are Texas, Louisiana, North Dakota, West Virginia, and New Mexico, with LCOH numbers ranging from $2.22 to $2.38 per kg (US maximum is $3.39). Electricity, water, and natural gas prices form the primary drivers/differentiators of these costs.

It should be clear, with a cursory look at both maps, that steam methane reforming with carbon capture is currently roughly half the price of electrolysis. While a lot of studies show electrolysis at a lower price, those studies ignore the opportunity cost associated with the electricity they use. If the models in question assume the electricity is free, because, for example, it comes from vertically integrated wind or solar, they are ignoring the cost of not selling the generated electricity. That loss of revenue is non-trivial and would bring them back to parity with our analysis.

This is a surface-level study focusing mostly on the required feedstocks and their respective prices in each state. To qualify as low- or zero-emission hydrogen, companies would need the ability to transport carbon dioxide to storage facilities (they can afford to pay up to $225 per ton for carbon dioxide transportation; the referenced LCOH numbers already include capture and storage costs), or access to low- or zero-emission electricity (this is not ubiquitous). This study does not evaluate the availability of either requirement. We intend to produce further articles on Enerdatics to expand on this analysis.

Because we cannot guarantee the ability to make these projects fully net-zero, these numbers do not reflect the impact of any 45V production tax credits, which may or may not be applicable, depending on the project. If we include those tax credits, they will reduce the LCOH numbers by up to $2.25 per kg (assuming the credits last for the first 10 years of the project’s life as currently stipulated by the Inflation Reduction Act of 2022, and the producers earn the full $3 per kg production tax credit).

{kind=link}