In 2020, energy fund manager Danilo Onorino forecast mergers would come for an industry struggling to survive pandemic fallout. It took a few years, but these days those tie-ups are all about “opportunistic bolt-on acquisitions.”

And that wave is not finished Onorino, portfolio manager of the Swiss-based Dogma Renovatio Credit Fund, said in an interview earlier this week.

The latest ripple came from Chevron Corp.’s

CVX,

-0.72%

$53 billion acquisition of smaller rival Hess Corp.

HES,

-0.79%

announced on Monday that gives the oil major a Guyana oil field and another U.S. shale stake. Weeks before, Exxon Mobil

XOM,

-0.91%

agreed to pay $59.5 billion to be a dominant producer in the Permian Basin via purchasing Pioneer Natural Resources

PXD,

-0.86%.

“So you have the largest oil company listed, Exxon, and the second largest, Chevron, that are buying smaller companies. So [what] they are buying is like a bolt-on acquisition and not a transformation acquisition. What that means is that if you buy oil companies in the market it’s much better than starting your own capex. So your profitability is basically better to buy paper oil instead of buying new projects.”

What he means is that these big companies had time to think through the metrics, which were saying “buy paper oil assets.” The Chevron/Hess deal was apparently in the works for a while, executives from both companies indicated in a Bloomberg interview following the deal.

And now, he says only ConocoPhilips

COP,

-1.74%

is among the top U.S. listed oil companies left to grab for a similar acquisition. Onorino says infrastructure group Williams Cos.

WMB,

+0.35%

or pure Permian Basin plays, oil and gas explorer Diamondback Energy

FANG,

-1.80%,

would be sought after because of their exposure to E&P assets that are clearly cheaper and less risky than any other new project. Occidental Petroleum

OXY,

has long remained a target of Italian energy giant Eni

ENI,

+0.87%,

he said.

Onorino has been an analyst since 1998 and was one of the industry’s youngest portfolio managers starting in 2000, as a portfolio manager at asset manager Arca SGR of Milan. He said for oil companies to go for anything other than bolt-on acquisitions puts them at risk for future lower oil prices and demand due to the boom for electric vehicles (EVs).

Earlier this week, International Energy Agency predicted that demand for coal, oil and natural gas would peak this decade, thanks to rising use of EVs and renewable energy.

He notes global auto sales remain lower than it was before the pandemic. “And the oil demand seems to be almost at the same level as before COVID ” — the demand lost in three months took three years to recover. And big oil producers like Saudi Arabia are aware of these numbers and putting money in green energy projects.

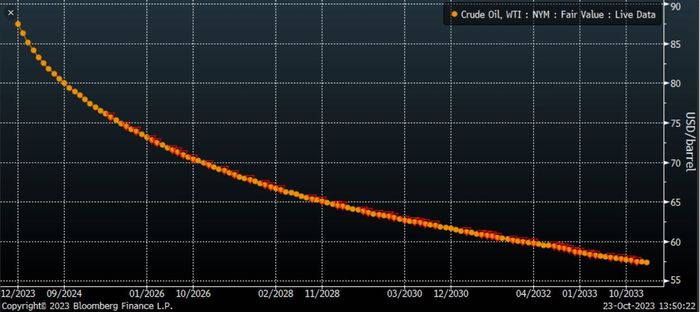

“So basically they have interest in investing in the transition, but at the same time they need to squeeze as much money as possible from oil,” and are keeping oil prices artificially high for now, even though crude is projected to go below $60 a barrel by 2033, he says, offering up another chart:

Long-term projections for long-term crude.

Bloomberg/Dogma

“So this is why the oil companies are preferring to invest into producing oil. That execution risk is much lower starting today a new project for the next 10 years in front of those uncertainties from energy transition,” said Onorino.

The shares of most oil majors have struggled for traction this year, as opposed to 2022, when climbing prices drove gains. The Energy Select Sector SPDR Fund

XLE

is flat this year, after a 57% gain in 2022 and a 46% climb in 2021. Crude oil prices

CL.1,

+1.66%

are up 7% year to date.

International oil companies in the U.S. are “exploiting a cost-of-equity advantage to buy high quality assets,” a team of Citigroup analysts led by Alastair Syme, told clients in a note Wednesday.

“In the case of Chevron-for-Hess, we think there is little that Chevron can bring to the table to enhance the value of the key asset (Guyana) given that the asset-operator is already doing what we believe is an impressive job. Chevron is not exploiting a competency arbitrage, it is is exploiting a financial one: we estimate Chevron is funding at an 8% CoE and Hess perhaps 10%+,” Citi said.