Oil production cuts this year by the Organization of the Petroleum Exporting Countries and their allies have given the U.S. the price incentive it needed to lift domestic output to its highest level on record, and maybe even helped fuel the recent mergers among the big oil companies.

Risks tied to hostilities in the Middle East, meanwhile, have provided another reason for the U.S. to boost oil production, defying efforts by other major producers to limit market supplies and keep prices high — and potentially setting up a fresh global fight for oil market share.

“The war in the Middle East and the risk of supply disruptions are long-term factors favoring investment in U.S. oil production,” Alex Kuptsikevich, senior market analyst at FxPro, wrote in recent commentary.

The countries that are part of OPEC+, which is comprised of the Organization of the Petroleum Exporting Countries and their allies, “have the spare [output] capacity but artificially limit production to support the price,” said Kuptsikevich. Perhaps they also see this trend of factors supporting oil investment, he said.

“” This could be a prologue to a shift in focus from the battle for profits and the final price of crude, to a war for market share.” ”

“This could be a prologue to a shift in focus from the battle for profits and the final price of crude, to a war for market share,” he said.

U.S. oil moves

In the U.S., oil production has climbed to 13.2 million barrels a day, according to the Energy Information Administration. That’s the highest based on data going back to 1983.

Read: U.S. oil production hits record as Israel-Hamas conflict stokes global supply fears

Data from Baker Hughes

BKR,

-1.33%

have also shown two consecutive weekly increases in the number of active U.S. rigs drilling for oil to total 502 as of the week ended Oct. 20.

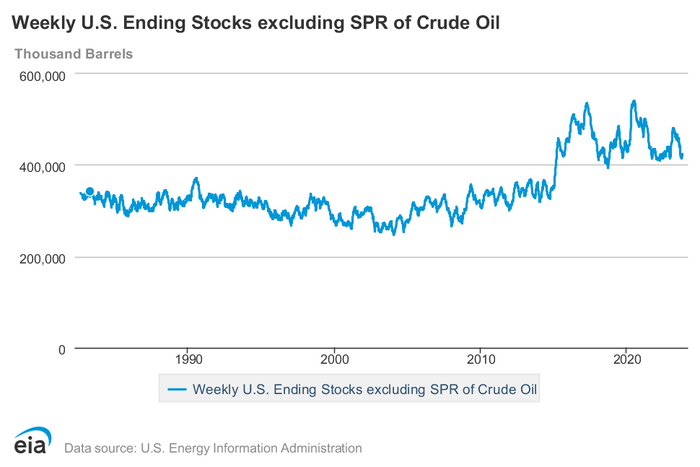

U.S. producers may have been spurred on by the fact that crude-oil inventories are now 4% lower than a year ago and close to their lowest since 2015, when the shale boom was in full swing, said Kuptsikevich.

Weekly U.S. commercial crude supplies dropped in late September to their lowest level since early December.

U.S. Energy Information Administration

They may also be encouraged by the U.S. government’s move to buy oil for the Strategic Petroleum Reserve, he said.

The U.S. Energy Department announced last week that it will post monthly solicitations to purchase oil for the reserve through at least May 2024 in an effort to replenish it following historic drawdowns last year.

Major oil companies have also announced mergers in recent weeks.

Exxon Mobil Corp.

XOM,

+0.18%

announced a deal on Oct. 11 to buy shale driller Pioneer National Resources Co.

PXD,

+0.09%

in an all-stock deal valued at $59.5 billion. Then on Oct. 23. Chevron Corp.

CVX,

-0.50%

said it reached an all-stock deal valued at $53 billion to buy Hess Corp.

HES,

-0.53%.

“Now it’s clear what the U.S. oil majors have been saving up for,” said Kuptsikevich.

Oil company mergers

The mergers among big oil companies has been “mostly driven by continued capital discipline with major themes being lower cost of production, and large, untapped reserves,” Dan Pazar, executive vice president at investment consultant Taiko, told MarketWatch.

Exxon is “continuing to leverage operating efficiency and pointing resources to some of the highest returning wells in the U.S.,” he said. With the purchase of Pioneer, it continues to “get more efficient in the cheapest part of the U.S. to produce a barrel of oil,” he said, noting that Pioneer produces oil at $35 a barrel.

For Chevron, by acquiring Hess, it’s continuing to diversify its portfolio, said Pazar. It gets additional shale assets in the Bakken “with infrastructure to boot…and access to the Guyana bonanza right there with Exxon.” Chevron has called Hess’s Stabroek block oil project in Guyana an “extraordinary asset.”

Overall, U.S. oil companies are “in great strategic positions and if they have the capacity to turbo charge production if oil prices see $130, they would probably look to take advantage of that if other producers (countries) didn’t,” said Pazar.

Middle East risks

The Oct. 7 Hamas attack on Israel, meanwhile, has increased volatility, as well as the potential for the oil market to see sudden disruptions and price spikes.

The Israel-Hamas conflict “remains top of mind and the threat to the region’s oil resources and infrastructure continue to warrant a fear bid in the oil market,” said Tyler Richey, co-editor at Sevens Report Research. “However, the lack of material escalation since the initial attacks by Hamas has seen some of that fear bid unwind as the conflict has been largely contained up to this point.”

Oil prices have climbed since the start of the conflict, but haven’t managed to climb back to the highs of the year reached in late September.

“Noise around geopolitical events” have been causing “small but not withstanding adjustments in price,” said Katy Kaminski, chief research strategist at AlphaSimplex.

On Wednesday, U.S. benchmark West Texas Intermediate crude

CL.1,

+1.85%

CLZ23,

+1.85%

saw its December contract end the session at $85.39 a barrel on the New York Mercantile Exchange, up 2% for the session. Global benchmark Brent crude’s December contract

BRN00,

-0.17%

BRNZ23,

-0.13%

climbed by 2.3% to settle at $90.13 a barrel on ICE Futures Europe.

“In the end, the oil price range seems mostly driven by supply and demand imbalances,” said Kaminski. “The supply side will likely be driven to action should prices move out of range, while demand will be much more dependent on whether economic conditions begin to contract due to tighter policy.”

OPEC+ cuts

Before the war began in the Middle East early this month, OPEC+ agreed in June to extend previous production cuts through the end of 2024.

Saudi Arabia had said at the time that it would voluntarily cut oil production by an additional 1 million barrels a day in July and has since extended that cut to the end of the year. Russia had pledged to cut its exports by 500,000 barrels a day from March through year end.

“Some of the bullishness surrounding the prolonged and disciplined OPEC+ output cuts has been tempered by the meaningful rise in [U.S.] production in recent months as a significant portion of those cuts is being offset by new barrels being lifted in the U.S.,” said Richey.

OPEC+ hasn’t hinted at any changes to its plans. The next official ministerial meeting is scheduled for Nov. 26.

Oil prices are “artificially” high right now because of the supply cuts led by Saudi Arabia and Russia, said Richey. Those higher prices are “inviting capitalists in the U.S….to take the risk of getting into the oil business and investing in oil production…to benefit from the strong oil-price environment,” he said.

For now, Richey believes OPEC+ producers realize that “giving up a modest amount of market share to the U.S. amid still rising global demand is worthwhile, as they will get to enjoy having a ‘slightly smaller piece of a much larger pie’.”