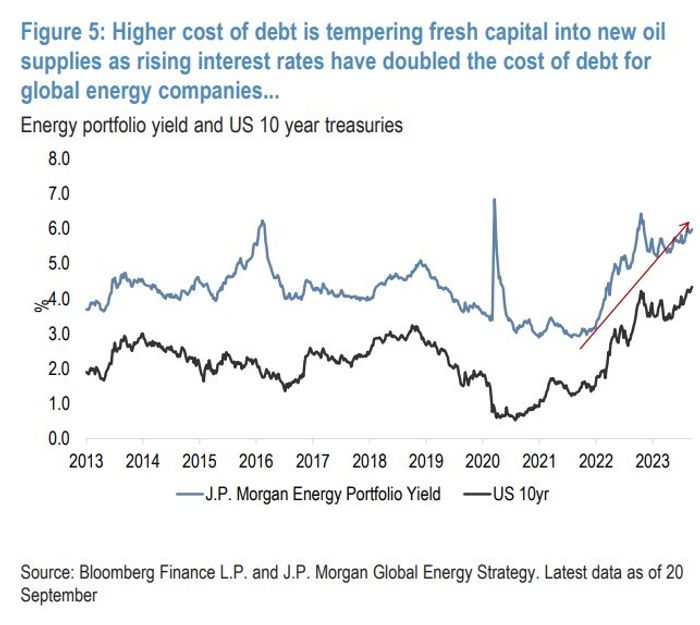

JPMorgan on Friday pounded the table for energy stocks, as higher-for-longer interest rates further squeezes the flow of capital into new supply.

Europe’s energy stocks

XX:SXEP

have only gained 10% since June while oil prices

CL.1,

+1.14%

have jumped 30%. JPMorgan said it’s recommending the majors over midcaps, upgrading Eni

ENI,

+0.81%

to overweight, reiterating overweights on Shell

SHEL,

+0.60%,

TotalEnergies

TTE,

-0.16%

and Neste

NESTE,

+1.86%,

and lifting Repsol

REP,

+0.35%

to neutral. The bank raised its rating on global energy stocks to overweight from neutral, as it sees an emerging supply-demand gap beyond 2025, coupled with strengthening sector fundamentals.

Globally, it said the key stocks to outperform are Eni, Shell, TotalEnergies, Saudi Aramco

2222,

-0.58%,

Exxon Mobil

XOM,

-1.41%,

Marathon Petroluem

MPC,

+1.38%,

Tenaris

TS,

-2.32%,

Baker Hughes

BKR,

-2.07%,

Cenovus

CVE,

-2.10%,

Prio , PetroChina

601857,

+1.50%,

Beach Energy

BPT,

+0.31%

and Ampol

ALD,

+2.11%.

“Dear generalists, put your seatbelts on,” said analysts led by Christyan Malek. “While we believe the sector is in a structural up-cycle and oil should normalize higher, we expect prices and by extension energy equities to trade in a wider range, discounting an effective higher weighted average cost of capital associated with elevated price volatility and concerns around ESG/peak demand.”

The analysts do not share the peak demand fears, at least on its investment horizon that runs through 2030, saying the clean energy system is not mature enough to capture and distribute to end customers. “As a result, this places greater pressure on traditional fuels to fill the gap and meet rising EM-led demand growth. However, without increasing oil and gas capex, we risk energy deficits and acute inflation across the commodities complex.”

“This may lead to multiple oil-led energy crises in this decade, potentially much more severe than the gas crisis seen in Europe in 2022. Moreover, it serves to position OPEC firmly at the steering wheel of the global oil market, to take greater share of demand growth, while helping mitigate sharp price moves in either direction.”

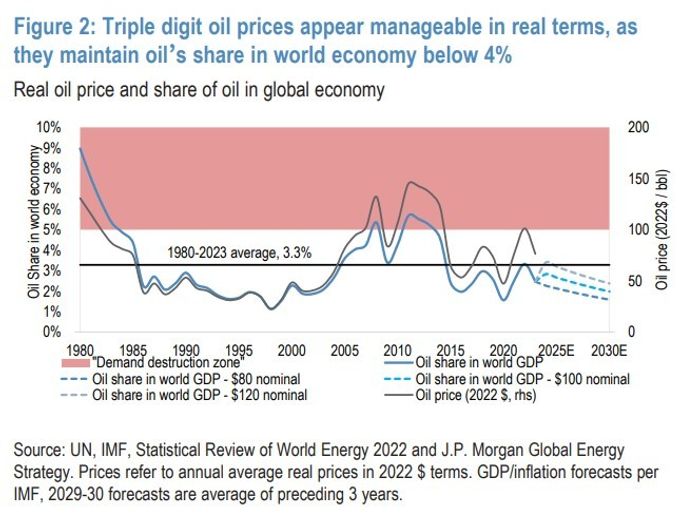

One interesting note is that the analysts do not find oil prices in the $100-to-$120 range to be demand destructive, as it would still imply oil’s share of the world economy below 4%.

Friday saw a catching down of European stocks to the sharp decline on Thursday on Wall Street, even though U.S. stock futures pointed to a stronger start.

The U.K. FTSE 100

UK:UKX

was flat while the German DAX

DX:DAX

fell 0.5% and the French CAC 40

FR:PX1

lost 0.9%.

Ubisoft Entertainment shares

UBI,

+3.58%

rose 4% after the U.K. competition regulator provisionally blessed the Microsoft-Activision deal that would see the French video games maker get cloud rights to Activision

ATVI,

-0.23%

games.

AstraZeneca stock

AZN,

+2.35%

added 2% as it and partner Daiichi Sankyo said a Phase III trial of a breast cancer drug showed statistically significant progression-free survival benefit. “This was another pivotal readout for [datopotamab deruxtecan] and could reinvigorate sentiment about this drugs broader potential to replace systemic chemotherapy across a range cancers whilst also providing another important read on safety,” said Dr. Sean Conroy, an analyst at Shore Capital.