imaginima

(Note: This is a Canadian company that reports using Canadian dollars unless otherwise noted.)

Advantage Energy (OTCPK:AAVVF) is one of the few managements that detail why Tier 1 acreage is not declining. There is a steady addition to Tier 1 acreage all the time as technology continues to advance to make more acreage desirable or even commercial. The result is that most of the industry has at least as many locations to drill over time as was the case in the recent past or even currently. There seems to be no end in sight to all the possible improvements that lie ahead in the future. Should that remain the case, then mankind will have all the access it needs to oil and natural gas production for the foreseeable future.

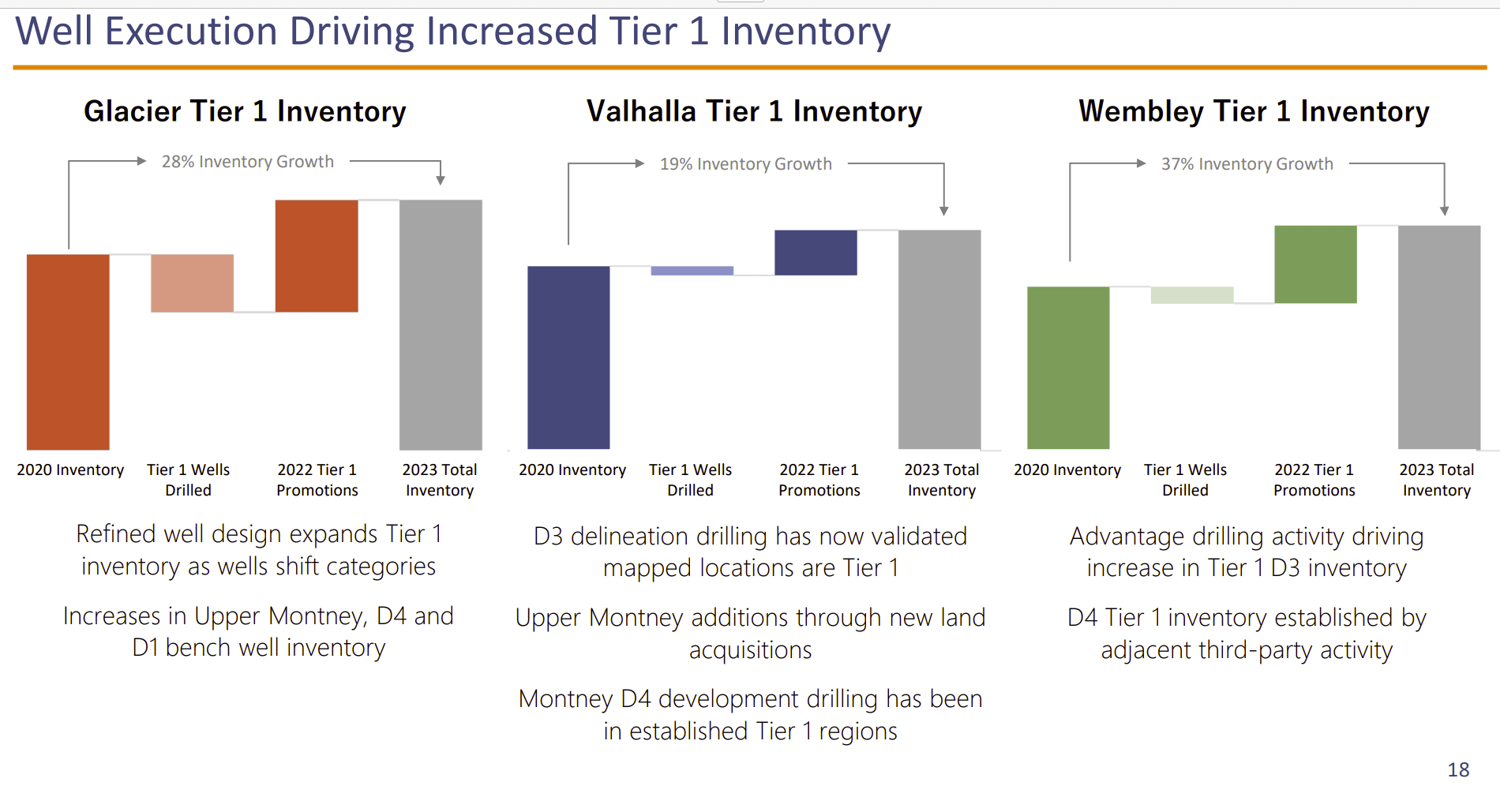

Advantage Energy Explanation Of The Tier 1 Promotion Process (Advantage Energy Corporate Presentation July 2023)

As shown above this is an annual summary of a process that is ongoing throughout the industry. What happens is that continuing improvements result in more recoverable production as well as more intervals becoming commercial.

The thing to remember about unconventional is that it is a relatively young part of the industry. Therefore, a lot of recovery numbers tend to be very low percentages compared to older established methods. That means that there is still relatively a lot of oil in place that can be recovered as the industry keeps “moving forward”. Even conventional benefits from this process to continually recover more oil.

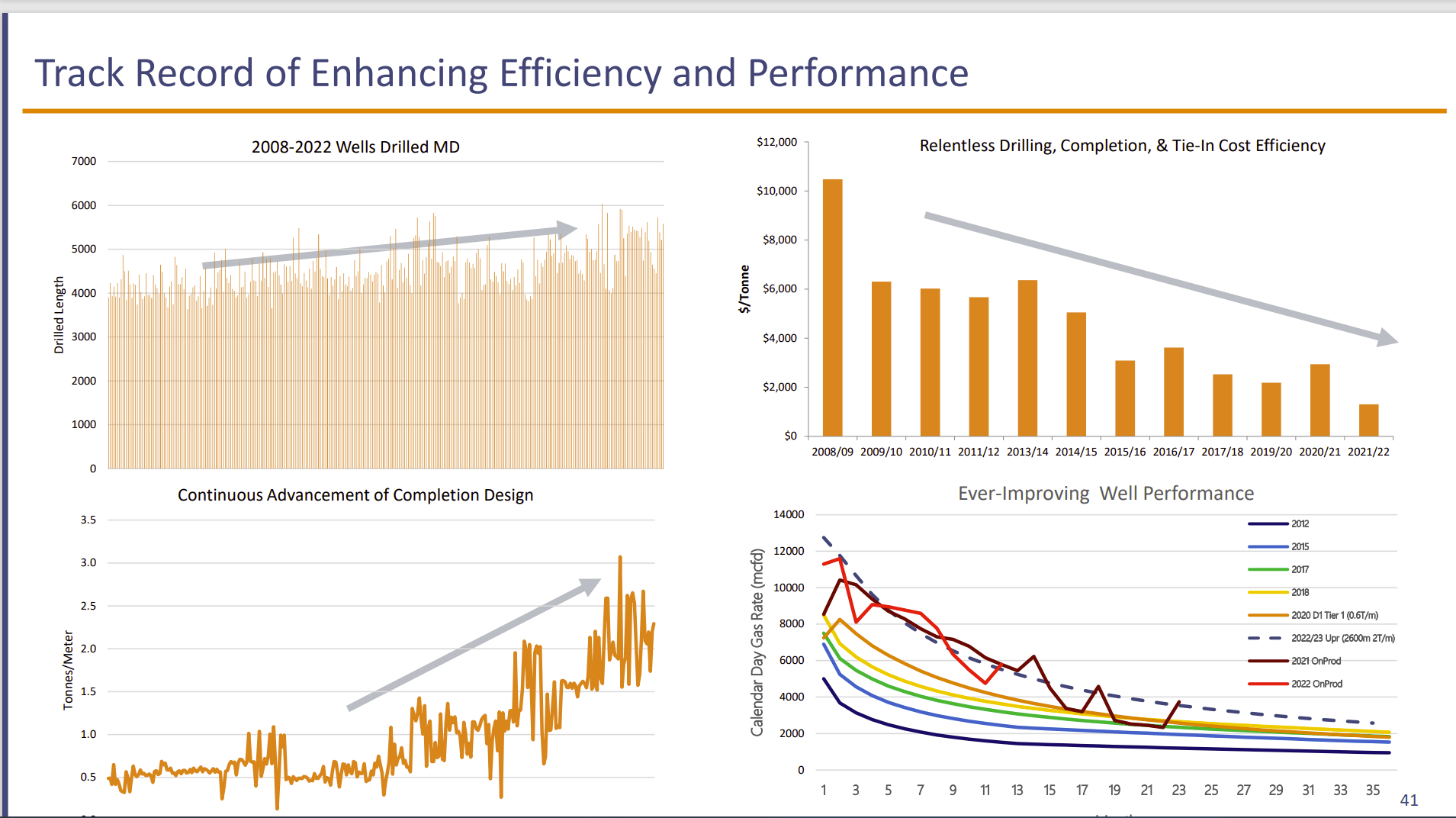

Advantage Energy History Of Improving Operations (Advantage Energy July 2023, Corporate Presentation)

As is typical with a relatively young part to this industry, rapid progress is being made. In the lower right-hand-corner graph, an observer can see where initial production has more than doubled over the years shown. This has led to more recoverable product. It has also lowered the company cost because there is more recoverable resource while the cost shown in the graph above declines at the same time more product is recovered.

What is not realized by many is a treadmill results wherein many companies budget improvements without yet having proof of those improvements. Several managements state that they know that costs have to decline by a certain amount (and production has to improve) just to maintain their competitive position.

Sometimes, one basin makes “a big jump” that makes that basin the next cost leader or production leader. The leading basin has switched several times since I began following this industry. It is likely to continue to happen in the future.

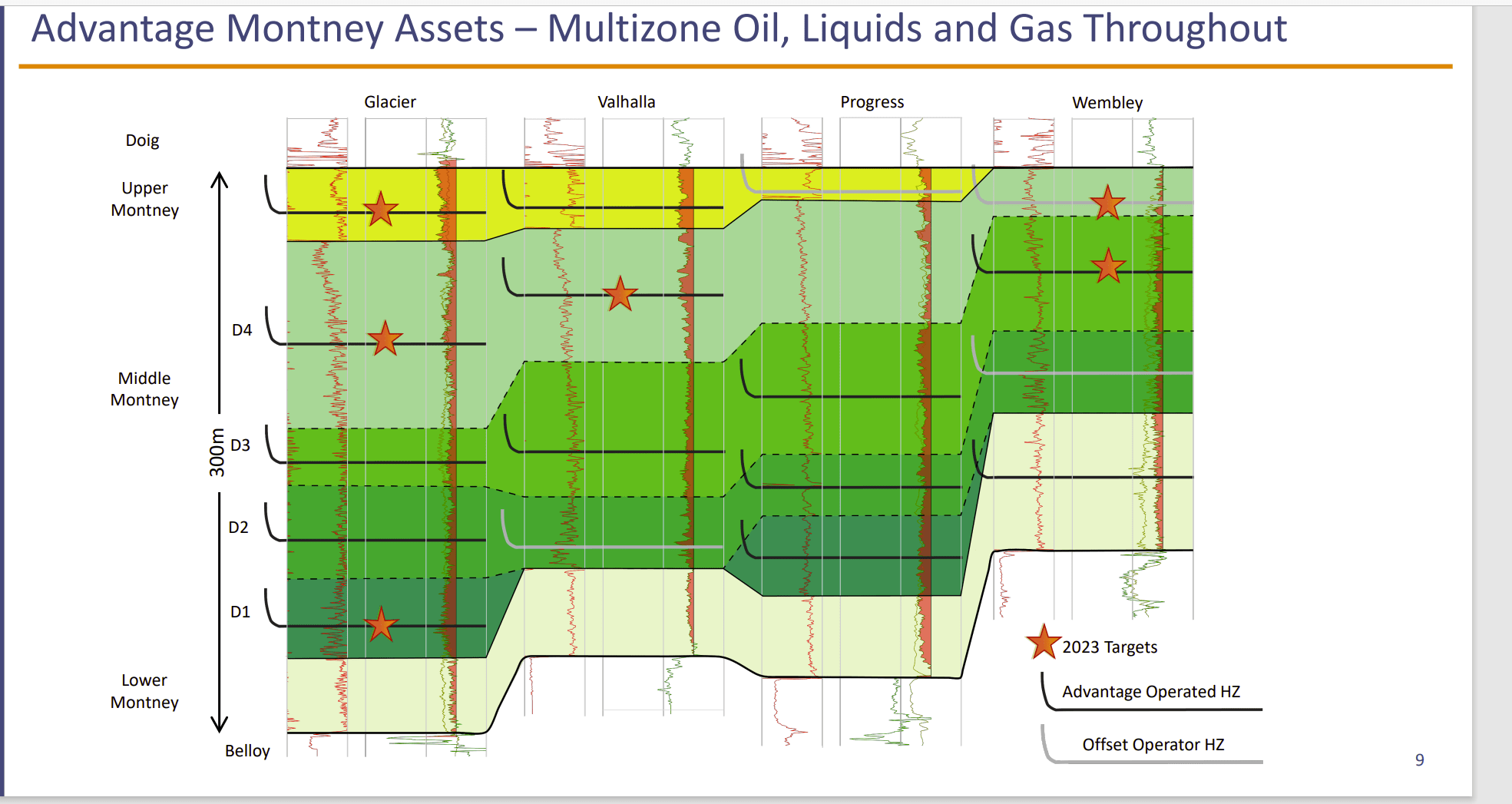

Advantage Energy Prospects For The Future By Interval And Current Production (Advantage Energy Corporate Presentation July 2023)

This management announced a “discovery” a few years back that involved the Middle Montney. Advantage remains primarily a dry gas Canadian producer to this day. However, technology advanced to the point that liquids rich intervals of the company leases are now commercial. Therefore, there is a slow transition by management to add liquids rich production which will allow profitability under a wider variety of future industry pricing scenarios.

Many of the blank spaces where there are no wells or spaces which show other operator wells are likely potential future targets. Too many investors rely upon the reserve report (which requires a good deal more certainty) to realize that many of these companies literally have decades of reserve to produce. Much of the producing acreage many of us review today has been producing long before we were around and will likely be producing long after we are gone. All that will change is the production techniques and likely the intervals produced.

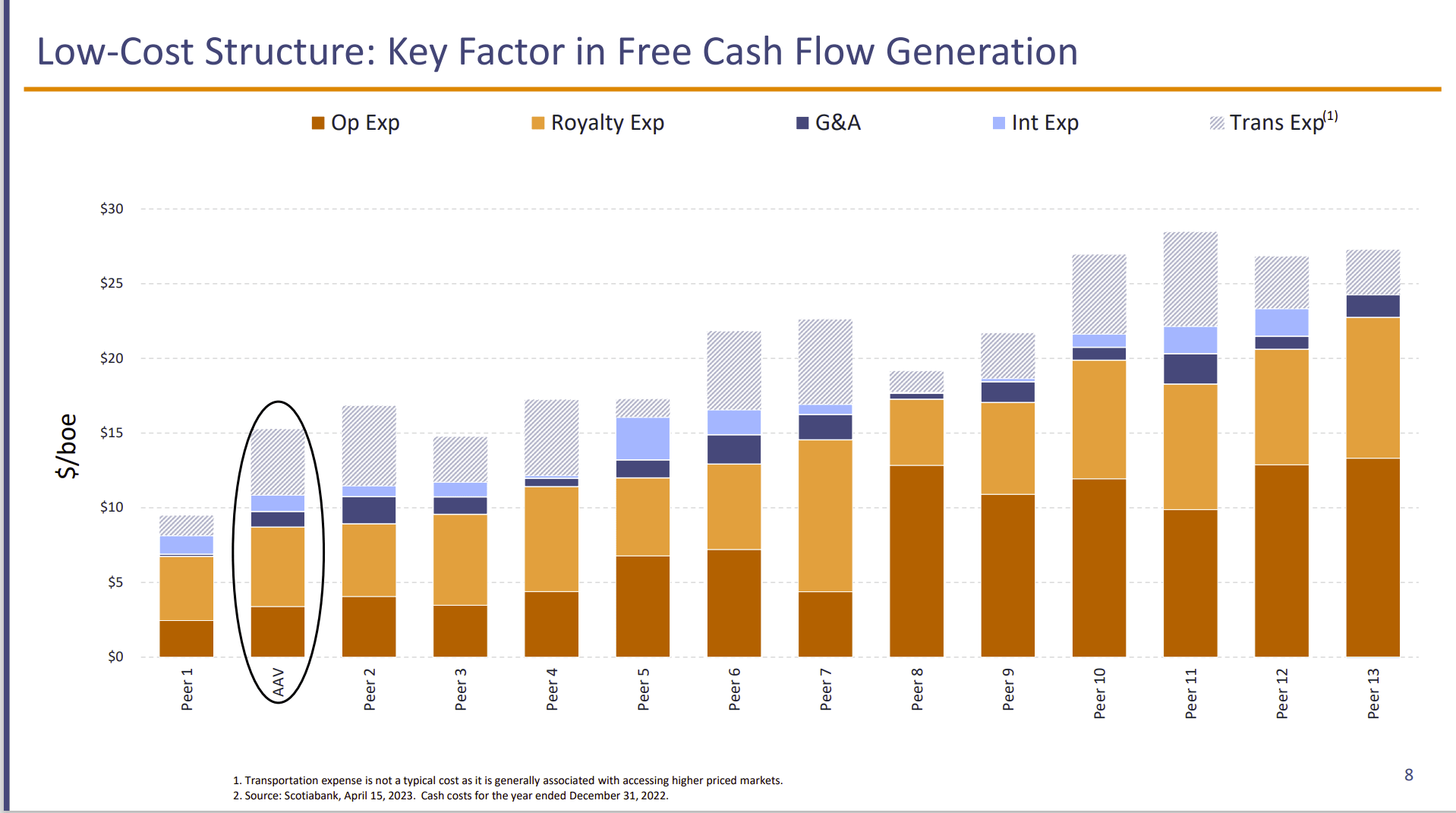

Advantage Energy Cost Comparison (Advantage Energy Corporate Presentation July 2023)

Advantage Energy does have some of the lowest costs in North America. Now the main issue with the comparison above is that often costs are compared without regard to production mix. Liquids producers often have higher costs to go with a more valuable production mix.

Advantage Energy has some very good geology. Therefore, management is trying to add liquids production while maintaining the very low costs that dry gas producers are known for. It will not be possible, for example to keep some costs like royalties as low as they are for natural gas. But management is succeeding in keeping overall costs low to keep the company competitive advantage.

The end result of this strategy (for as long as management succeeds) is that the margin will likely widen as the company increases the average selling prices because the liquids production becomes a larger percentage of the overall production. That should increase company profitability.

Many companies show costs similar to the chart above. But the real story is the margin achieved under various industry scenarios along with how fast the company recovers its costs (payback period). It is possible to have higher costs and be more profitable if the margin and volumes allow for it.

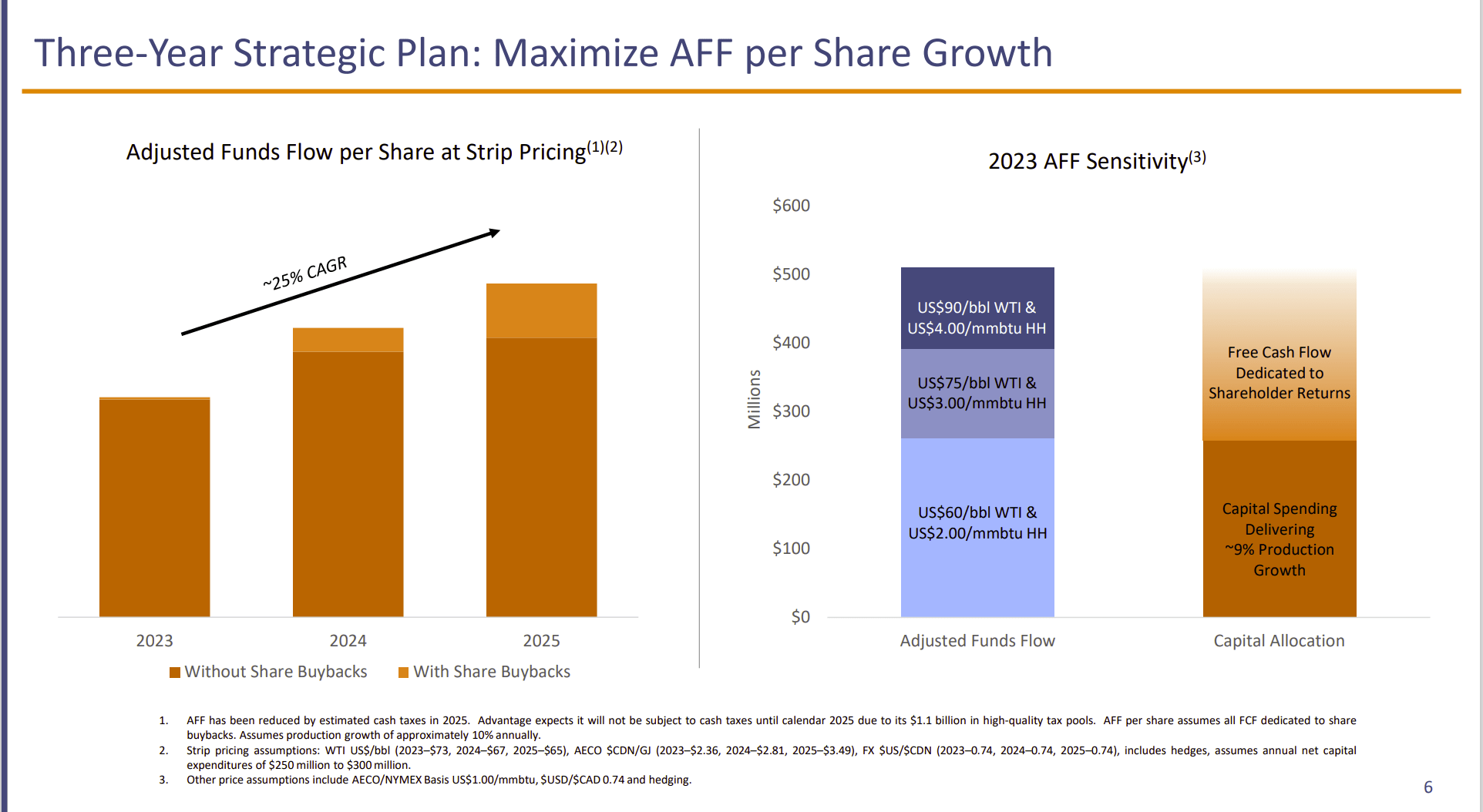

Advantage Energy Adjusted Funds Flow Per Share Growth Guidance (Advantage Energy Corporate Presentation July 2023)

Advantage Energy is a relatively small producer in Canada. It tends to be a profit leader throughout the business cycle. Therefore, growing company production so that the company attracts a wider range of investors makes a lot of sense. Investors should not expect a dividend from this company in the foreseeable future as a result.

Similarly, basin diversification is unlikely because the cost advantage where the company operates is so significant. This management tends to invest in midstream facilities to coordinate with the upstream activities to minimize overall costs. That strategy is likely to continue for some time to come. This would likely be designated a “specialist” strategy where the company grows by improving operations (and expanding operations) right where it currently is.

The oil and gas industry has had a miserable experience especially during the 2015 to 2020 period. Natural gas had a longer downturn due to the rapid growth of unconventional. Now things appear to be heading towards cycles the industry is known for. The disruptive period caused by rapid unconventional growth appears to be over.

That should make for a more profitable future than was the case in the past. This company managed to grow through much of the hostile past period. That should mean that the future will allow for more profits and potentially faster growth.

As the company has demonstrated, Tier 1 acreage is not going to be a worry for some time to come. But smaller companies like this need a patient investor because a rapid solution to the company price is unlikely.

Nonetheless, this low debt company has a lot less risk because of the low debt and low-cost leadership than is the case for many companies of the same size. Despite at least one key retirement in the last few years, this management appears to have the experience to guide the company to a larger and more profitable future.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

{kind=link}