spooh

The nice thing about stocks is that there is almost always something on sale, no matter how high the broader market index is trending. That’s why investors like Warren Buffett prefer to invest in stocks rather than physical real estate, which is almost always fairly priced unless if you want to put sweat equity into a fixer upper.

One stock that now appears grossly undervalued is TC Energy (NYSE:TRP), which as shown below, has fallen materially since the start of July and is trading 37% below where it was a year ago. I last covered TRP here back in March, highlighting its valuable assets and strong demand trends. In this article, I provide an update and discuss why now may be an opportune time to layer into this high-yielding stock.

TRP Stock (Seeking Alpha)

Why TRP?

TC Energy is a Canadian midstream giant that owns pipelines, storage, and power generating assets across North America. Its gas pipelines supply 25% of North America’s demand, liquids pipelines support 20% of Canadian crude oil demand, and power generating assets provide 4,300 MW of capacity, approximately 75% is emission-less.

TRP enjoys stable robust cash flows that are supported by 96% investment grade customers, and management projects 2-3% annual EBITDA growth between now and 2026 with very minimal sustaining capital requirements. This was supported by 4% YoY EBITDA growth during the second quarter (10% YoY growth on a six month basis), driven by strong performance in the liquids pipeline business.

Moreover, TRP is seeing strong demand for natural gas in the U.S., achieving record LNG feed gas deliveries of 3.8 Bcf, representing over 30% of current U.S. LNG export. It’s also making steady progress in projects in Mexico and expects to complete the lateral section of its Villa de Reyes pipeline by Q3 of this year.

So far this year, TRP has placed CA$2.1 billion worth of assets into service, with the anticipation of $6 billion of assets into service by the end of the year. Importantly, TRP’s long anticipated Coastal GasLink project is now 91% complete and management expects mechanical completion by the end of this year and to be in-line with its prior CA$14.5 billion estimated budget.

The Southeast Gateway pipeline is also on track against its US$4.5 billion estimated budget. Being on target with budget mitigates need to raise dilutive capital from equity and debt markets, and management expects full year 2023 EBITDA to be 6% higher at the midpoint.

TRP’s balance sheet is supported by its recent partial sale of a 40% stake in the Columbia Gas asset to GIP. This will help TRP deleverage from 5x debt to EBITDA to 4.75x by the end of 2024.

The biggest news, of course, is management’s planned spin-off of its liquids pipeline segment in order to simplify its remaining natural gas and power generation businesses. This includes 3,000 miles of liquids pipelines, of which 88% of EBITDA is contracted and 96% of volumes is underpinned by investment grade customers.

The liquids business is expected to grow its EBITDA at a slower 2-3% forward annual rate, as opposed to the 5-7% rate for the rest of the business. Moreover, the spin-off is expected to be a tax-free transaction for shareholders. While I don’t really see the value of the spin-off as it relates to the long-term outlook for either entity, it doesn’t appear to be a negative for the company, either, as nothing really changes for shareholders from an asset base perspective.

Importantly for income investors, TRP expects a 3-5% annual dividend growth rate for the RemainCo and a 2-3% growth rate for the Liquids business post-spinoff. This would build upon TRP’s existing 23 consecutive years of dividend growth. The present dividend rate is also well-protected by a 50% payout ratio as a percentage of cash flows.

Risks to TRP include execution risks as it relates to capital projects. Higher than expected interest rates can also pressure the bottom line. Plus, while the vast majority of TRP’s customers are investment grade rated, volatility in commodity prices raises counterparty risk.

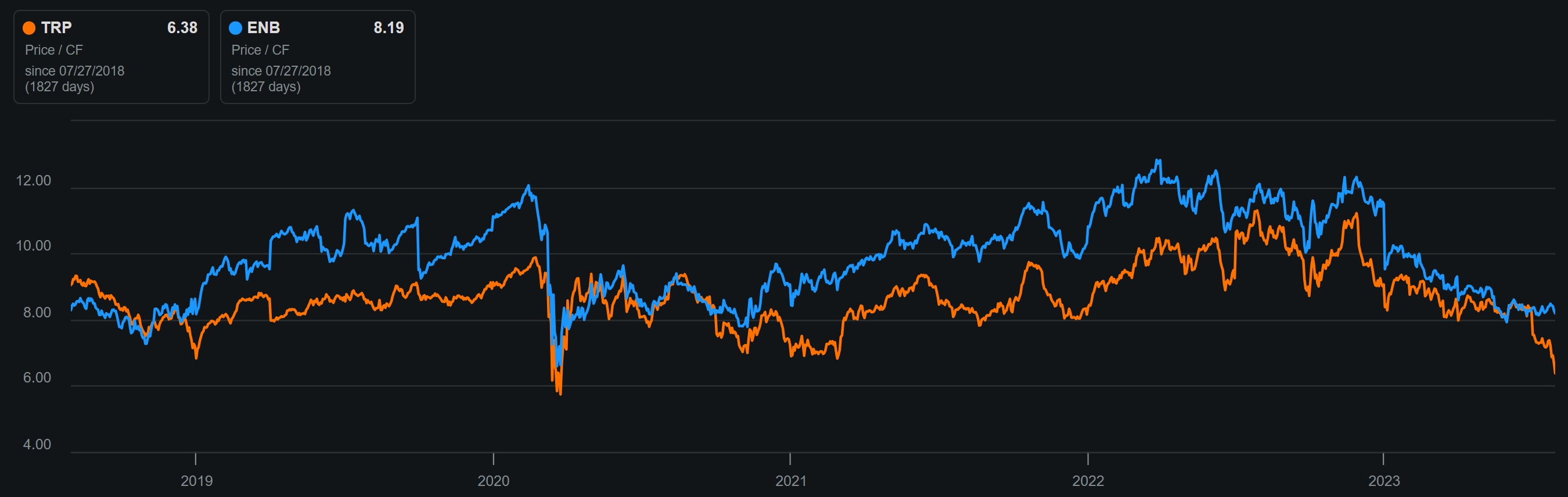

Lastly, it appears that plenty of risks have already been baked into the current share price of $34.17 with a price to cash flow of just 6.4. As shown below, this sits close to TRP’s pandemic low in 2020 and the valuation gap with Canadian peer Enbridge (ENB) has significantly widened over the past week. As such, investors could see strong-double digit total returns even if TRP returns to a still modest price to cash flow of 7.5x.

TRP and ENB Price-to-Cash Flow (Seeking Alpha)

Investor Takeaway

TRP’s share price has fallen significantly since the start of July and is now down 37% year to date. This creates a compelling entry point for value-oriented investors looking to pick up a high-yielding stock with strong assets, robust cash flows, and long-term EBITDA growth visibility. Lastly, the sum of the RemainCo and Spin-off businesses should be worth more than what the combined entity is currently trading for now, creating a value opportunity for income and capital appreciation potential.

{kind=link}