Torsten Asmus

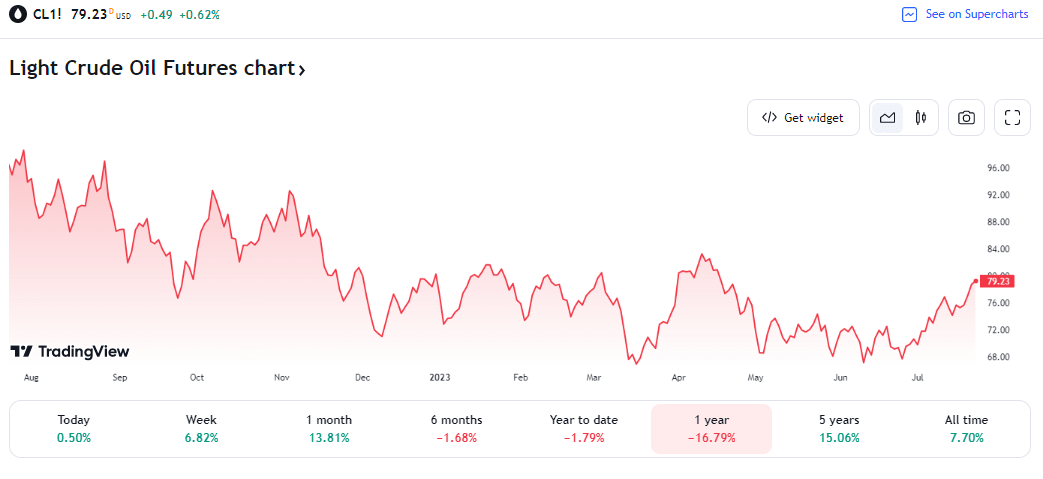

July US Consumer Confidence rose by much more than economists had expected. Could a reversal of optimistic fortune be in the offing, though? Domestic crude oil has climbed to its highest price since April, nearing the $80 mark. That is bad news for commuters, but a profitable trend for oil drillers.

I have a buy rating on shares of Chord Energy Corporation (NASDAQ:CHRD) for its low valuation, robust growth outlook, high free cash flow, but its technical chart leaves something to be desired.

Energy Prices On the Rise

TradingView

According to Bank of America Global Research, CHRD the second largest oil and natural gas producer in the Williston, formed from the merger of Oasis and Whiting and Petroleum in 2022. Management estimates that it has approximately 1,000 to 1,100 ‘core’ locations assuming an average two-mile lateral length. Pro forma, it has estimated 2021 proved reserves of 577 MMboe, (approximately 56% oil and 76% PDP).

The Houston-based $6.3 billion market cap Oil and Gas Exploration and Production industry company within the Energy sector trades at a low 3.3 trailing 12-month GAAP price-to-earnings ratio and pays a somewhat high 3.3% forward dividend yield. Ahead of earnings due out next week, the stock features a 40% implied volatility percentage (a bit on the elevated side) and a material 5.6% short interest.

Back in May, Chord topped bottom-line earnings expectations with a $4.49 EPS figure, above the $4.29 consensus estimate. The oil & gas name also bettered revenue forecasts with a more than 37% year-on-year increase in sales. It was actually a whopping revenue amount versus expectations due to per-day oil production verifying on the high-end of its guidance for Q1. Its base-plus-variable dividend amounted to more than $3.

The firm is on the growth hunt as evidenced by a key strategic acquisition of Williston Basin assets from Exxon in a $375 million deal. The move looks like a good fit and a decent use of cash, though just recently, Cohen came out cautious on Chord due to its valuation. But with a more than 10% free cash flow yield and a solid dividend, I see the stock attractive fundamentally. Key risks include adverse oil price differentials emerging, higher capex spending requirements, and poor execution of newly acquired assets.

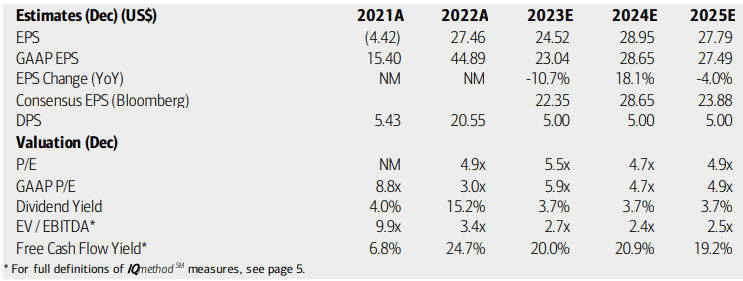

On valuation, analysts at BofA see earnings falling by more than 10% this year while 2024 per-share profits are expected to snap back before a small 2025 retreat. The Bloomberg consensus forecast is slightly less optimistic, however. Chord’s dividends, meanwhile, are expected to hold at $5 annually through ’25. Following its 2020 merger between Oasis Petro and Whiting Petro, the company’s management team is focused on both free cash flow and shareholder return. With more than $40 of trailing 12-month free cash flow per share, there’s ample room for more shareholder accretive actions.

Chord: Earnings, Valuation, Dividend, Free Cash Flow Yield Forecasts

BofA Global Research

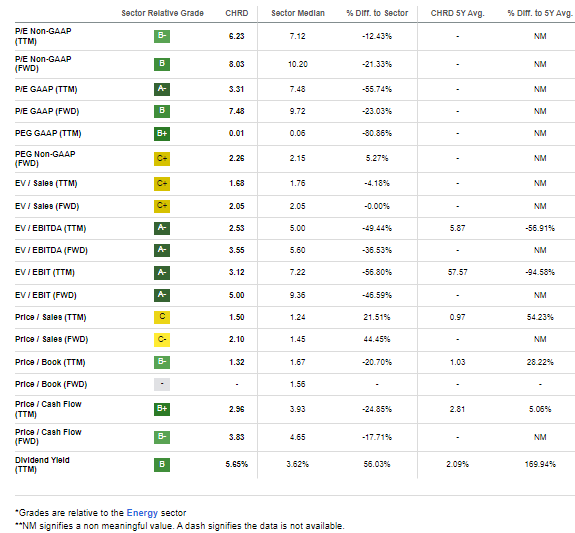

If we assume normalized annual EPS of $23 and a P/E of 8, then shares should trade near $184. With a stymied growth outlook, I assert that the earnings multiple should remain at a discount to the sector median. Also, a higher P/E would result in a lofty price-to-sales ratio.

CHRD: Compelling Valuation Metrics

Seeking Alpha

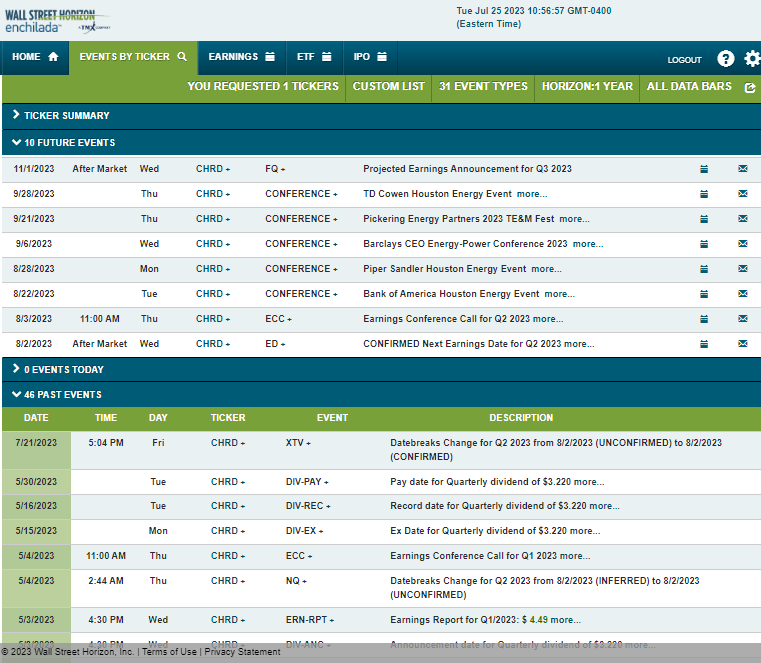

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q2 2023 earnings date of Wednesday, August 2 AMC with a conference call the following morning. You can listen live here. After that, volatility could continue to run high as the management team is expected to present at five different industry conferences from August 22 through the end of September.

Corporate Event Risk Calendar

Wall Street Horizon

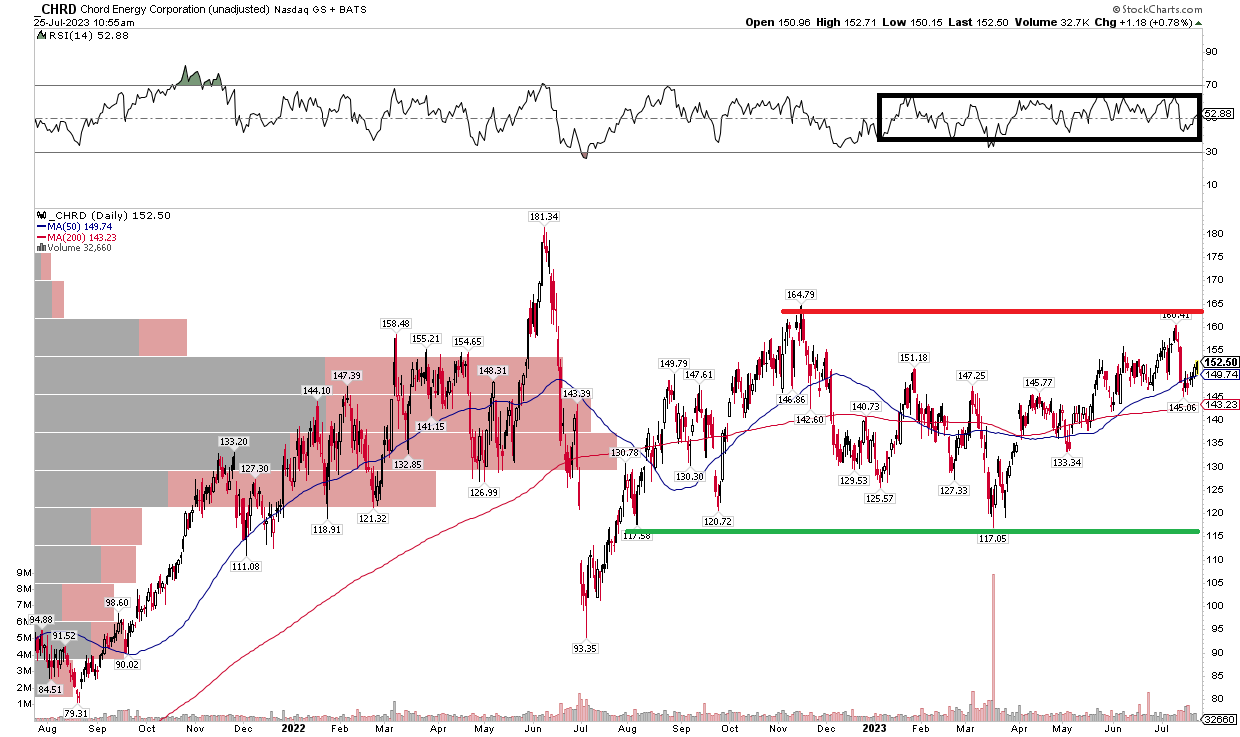

The Technical Take

While I like CHRD’s free cash flow and valuation, the chart is very lukewarm. Notice in the graph below that shares have done virtually nothing since the spike high in June last year. With an ongoing range between $117 and $165, I would like to see a definitive breakout before turning bullish from a technical perspective.

Also take a look at the RSI momentum indicator at the top of the chart – it, too, is stuck in neutral, further supporting the case that it’s a battle between the bulls and bears. With a generally flat 200-day moving and high volume by price in this frustrating zone, this is by no means a buy when ignoring the fundamentals.

CHRD: Sideways Price Action, Neutral Momentum

Stockcharts.com

The Bottom Line

In this case, I will weigh the valuation and macro factors more than CHRD’s lackluster chart. So, I have a soft buy rating on the firm. Perhaps the earnings report next week will be the catalyst for a breakout above the $160 to $165 area.

{kind=link}