ShyLama Productions

Introduction

This will be our 4th article on MEG Energy (OTCPK:MEGEF) (TSX:MEG:CA). I encourage you to read my past articles for deep background on this company. We are going to stick to operations, Q-1 financials, and guidance for the rest of 2023 and 2024 with a goal of determining the plan ahead of the earnings release, July 28th.

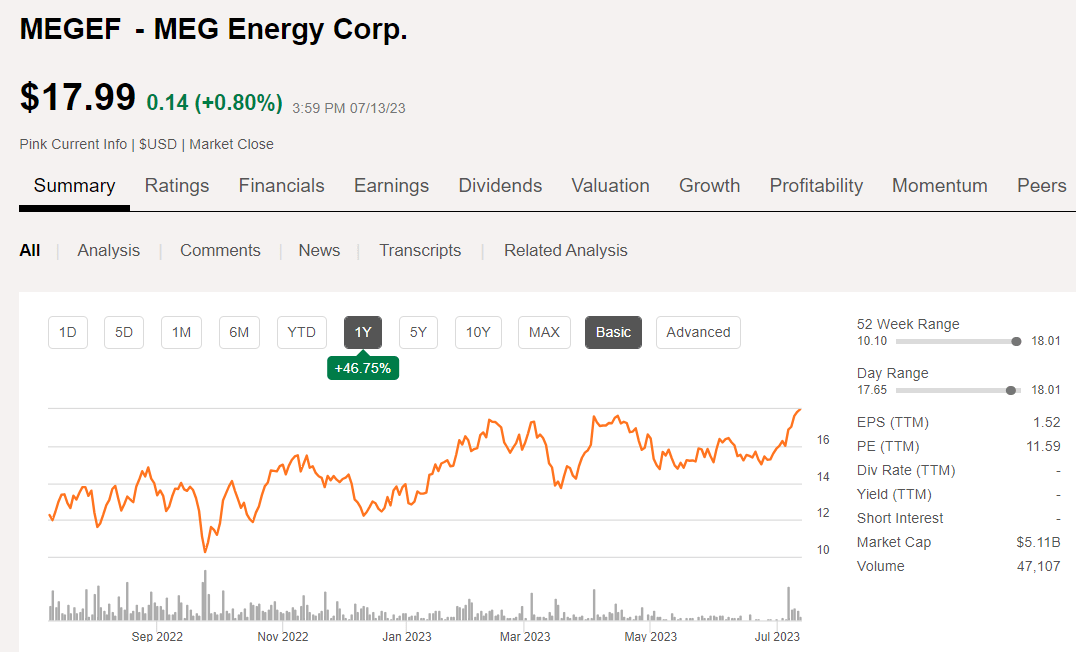

MEG Price Chart (Seeking Alpha)

MEG has rallied strongly since our last article in January of 2022, rising from the $12’s to nearly $20, a one year high. Interestingly, the company seems to have avoided the sharp sell-off that has befallen many energy companies in the last few quarters. Activity like that is always interesting and invites a fresh look.

Although we’ve tipped our hand with the call, please keep reading for the complete assessment of this Canadian heavy oil producer.

The thesis for MEG Energy

A bit of preamble. Inventories took a step back this week and took some steam out of the price of WTI, still hanging about in the upper $70’s. We are choosing to follow the structural trends-end of SPR releases, curtailed production from OPEC, Saudi, and Russia, flattening growth in shale output against increases in global demand for refined products, which will drive inventories lower as we close out the year. That’s not just me talking, but folks with access to Kepler tanker data and Rystad Air traffic data are saying that inventories are going to dive. Here is a link to a podcast on the subject by Eric Nuttall of Nine Point Partners. It is well worth a listen, as it is 30 minutes of pure gold as regards the energy markets. I have other sources as well, and they all lead to the same conclusion. Oil is structurally undersupplied in the physical market, and soon the paper market is going to figure it out.

One final point, I am tired of waiting for this recession. I don’t think it is coming, in spite how badly some folks seem to want it. More importantly to our topic, it doesn’t matter to oil inventories (which is all that matters). Eric touches on a critical historical fact – “in recessions what usually happens is not a fall-off in oil demand, but a fall-off in the rate of growth for oil demand.“

Ok on to MEG.

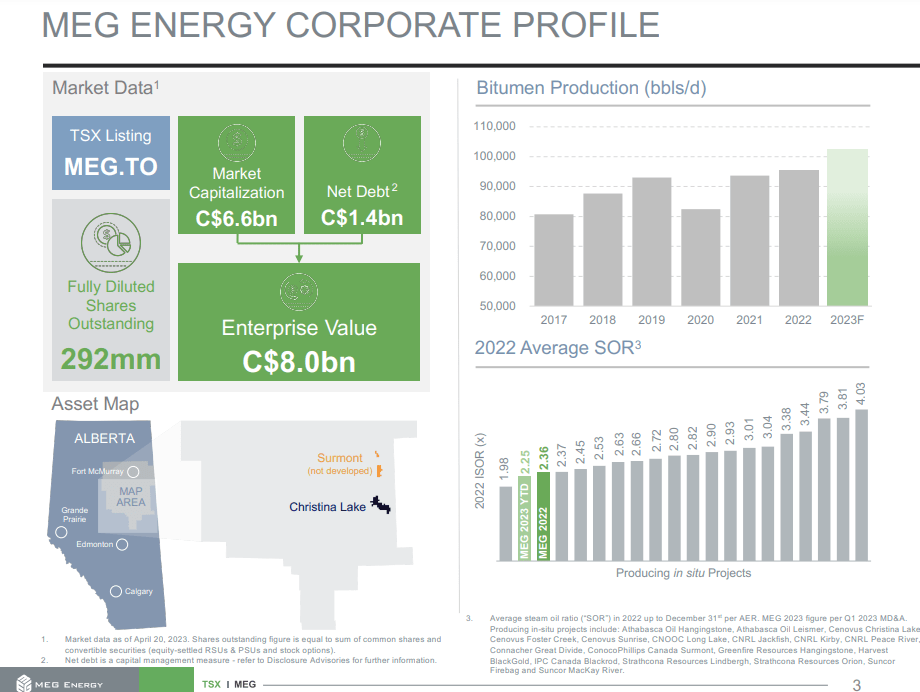

MEG is a heavy oil (bitumen) producer at Christina Lake, in Northern Alberta province, Canada. Its output is sought for blending with lighter shale oil, the traditional sources of which, Mexico and Venezuela, have been reduced in recent years. MEG’s production has some potentially high cost inputs as the oil it produces must be steam-flooded out of the rock. Technology can play a big role on the impact of steam generation, and you should have a look at one the past articles for a run down on MEG’s technology. The graph in the lower RH corners shows a definite advantage for MEG in the 2022 steam to oil ratio-SOR, against competitors.

MEG corporate profile (MEG)

MEG is now benefiting from narrower WCS differentials and low fuel costs for steam generation, and this is having a positive impact on financial results. MEG’s capital allocation priorities are 50% to debt reduction, ~$1 bn, a decline of some $600 mm, and 50% to shareholder returns, rising to 100% of free cash once the debt target is met.

Expectations are for daily output to have dropped in the second quarter to 84-88K BOPD, due to turnaround scheduled for the quarter in Phase 1 and 2 facilities. The impact for the entire year is expected to equate to 6K BOPD, and the company anticipates a YE exit of ~100-105k BOPD.

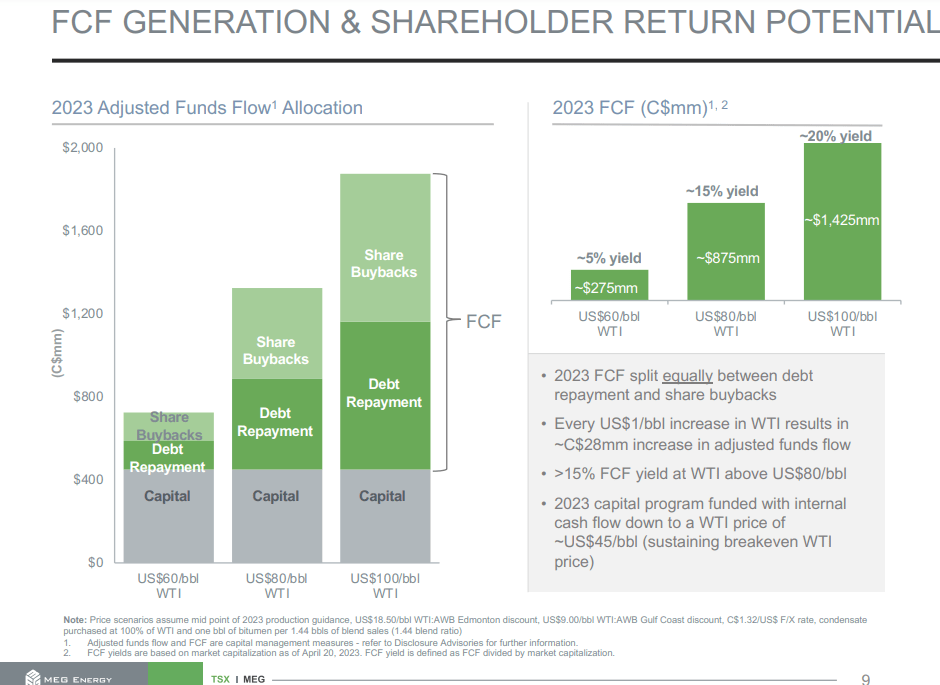

MEG FCF Generation (MEG)

Long term catalysts for MEG

MEG has the footprint to be in the business for decades without any significant acquisitions. With 35 years of 1P reserves and 55 years of 2P reserves at Christina Lake. When oil prices rerate (assuming inventories decline) these reserves will be rebooked at higher rates. This should also help boost the stock price.

Longer term they have a similar resource at Surmont and what they term their “Growth Properties” to the west of Christina Lake.

MEG Footprint (MEG)

Q-1, 2023 and guidance

MEG tallied $274 million of adjusted funds flow or $0.94 per share in the first quarter of 2023. A 6% production increase YOY from 2022 was more than offset by a 49% decrease in their bitumen realization after net transportation and storage expense. As a result, cash operating netback declined to $34 per barrel from $70 per barrel in the first quarter of 2022. Ouch.

In Q-1,2023, MEG sold 56% of its AWB (Dilbit) blend in the U.S. Gulf Coast, generating a $2.25 per barrel premium relative to the Edmonton AWB Index. In addition, operating expenses net of power revenue declined to $6.13 per barrel, reflecting a 78% increase in their realized power price and lower natural gas prices compared to the first quarter of 2022.

Crown Royalties also declined to $3.18 per barrel as a result of lower bitumen revenue. It had been estimated that the Christina Lake project would reach royalty payout late in the first quarter. However, advanced expenditure timing provided additional royalty shelter during the quarter and moved that time into early Q2. We will touch on the potential for this impact in the risks section.

After funding $113 million of capital expenditures, MEG generated $161 million of free cash flow for debt reduction and share buybacks in the first quarter of 2023. The company repurchased $86 million of senior notes and ended the quarter with $1 billion of net debt. In addition, they bought $103 million or 4.9 million MEG shares in the quarter at a weighted average price of $20.88.

Guidance

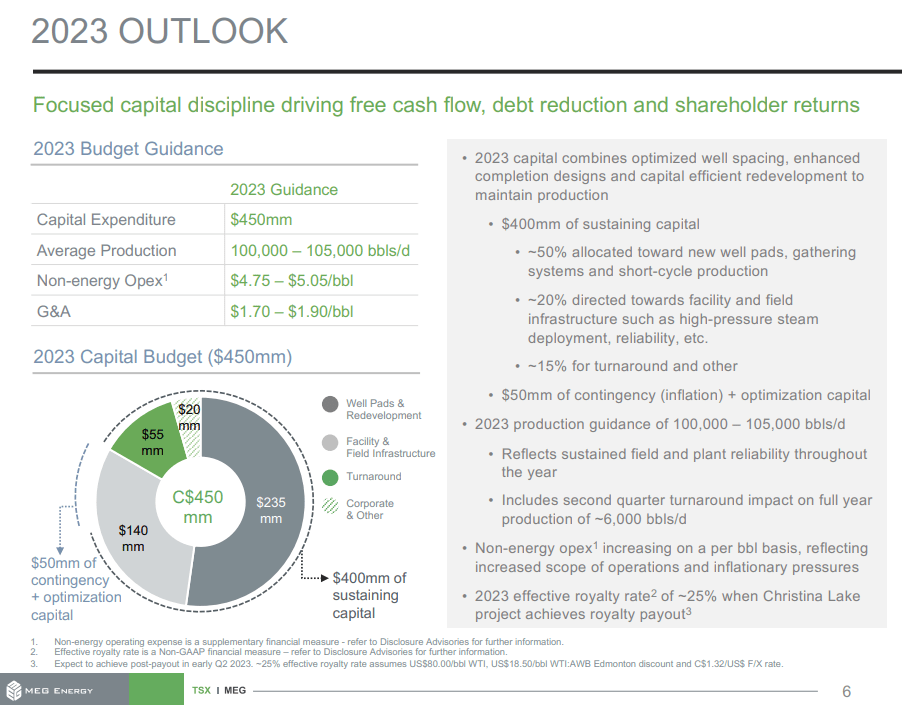

The infill and redevelopment drilling program is underway that will support YE 2023 production guidance of up to 105K BOPD. There should be an uplift from the narrower WCS discount as well. Netbacks for Q-2 should be on the order of $45 per bbl for Q-2, if this holds up or an uplift of about $10 per barrel times their daily production.

MEG 2023 Outlook (MEG)

Risks

One of the things that is driving higher netbacks for MEG is low fuel-gas costs. There is no reason to think this will change much in 2023, as noted in the Weekly Gas Storage report put out by the EIA. This week we injected 49 BCF, down from 62 BCF the week before, so there is definitely an observable down slope here that may be aggravated by a fall-off in drilling. We will see.

The narrower WCS discount is also core to this thesis. The discount has narrowed thanks to anticipation of the end of the SPR releases, an increase of refinery demand in the summer months, and perhaps increased purchases to refill the SPR – we will see about that as well. If inventories do tank as prognosticated, oil will be outside the range the administration has said it will buy.

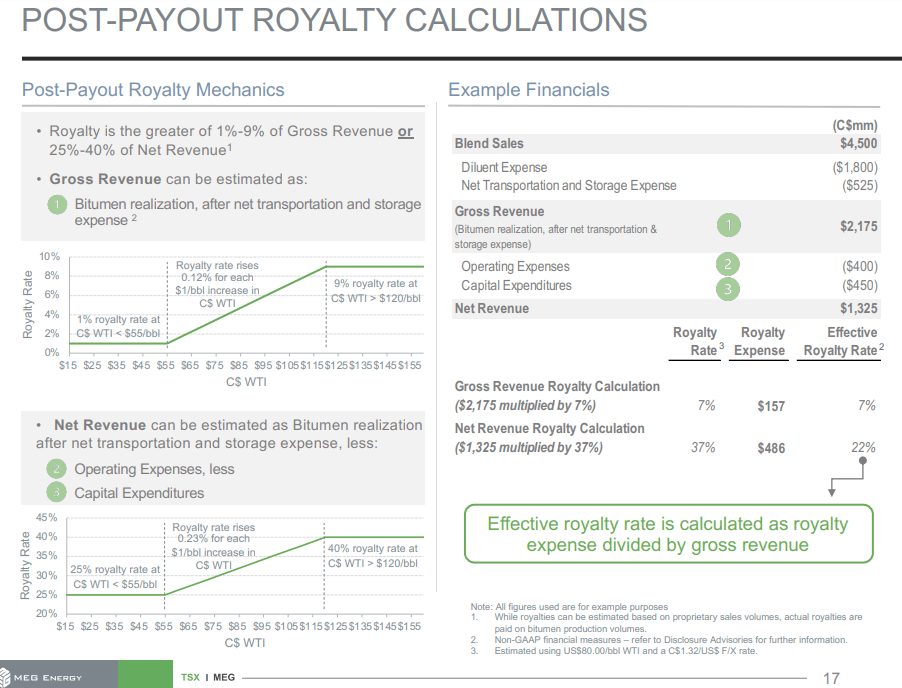

Company facilities at Christina Lake are moving to a post-payout structure that will increase the government’s take on Bitumen. The slide below breaks down a sample calculation. For reference MEG paid about $225 mm CAD in 2022 with a reference price of $122 for WTI. This is another reason we are rating MEG a hold, to see the actual effect the post-payout royalties have on AFF for Q-2.

MEG Post-Payout Calcs (MEG)

Your takeaway

MEG is currently trading at 5X EV/EBITDA and $57K per flowing barrel. Neither of those are off-putting, but we should take into account the hit, the turnaround will deliver to daily output.

With daily production of as low as 84K BOPD, EBITDA could decline below $211K for Q-1, and raise the EBITDA multiple by several points on a forward basis, and the P/FB to $64K per barrel. When you combine the increases in royalties are going to be due henceforth, there are just too many variables in play right now to accurately assess cash flow or AFF.

On that basis, I think the plan is to hold at current levels, to see how this comes out, and be ready to scoop up shares of MEG afterward.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

{kind=link}