deepblue4you

Crude oil has seen a bounce in price as global demand is expected to reach a record high this year. Even with the slowdown in economic activity from industrialized nations production cuts from Saudi Arabia and Russia appear to be a major factor in stabilizing oil prices.

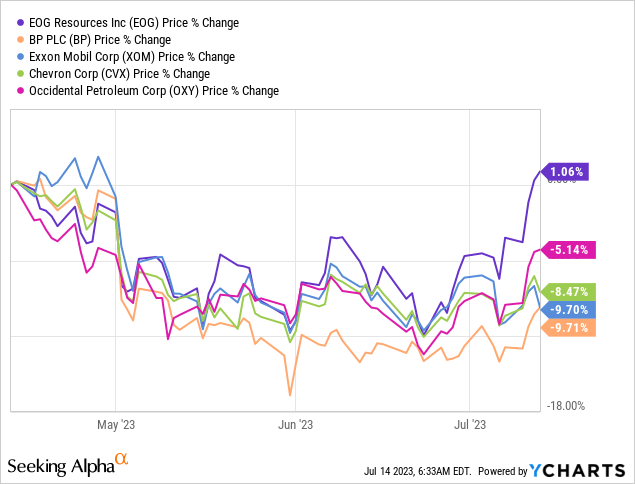

Of the major oil-related holdings in John and Jane’s portfolio, we are still looking at all of them (with the exception of EOG Resources) (EOG) being underwater compared to their stock price three months prior.

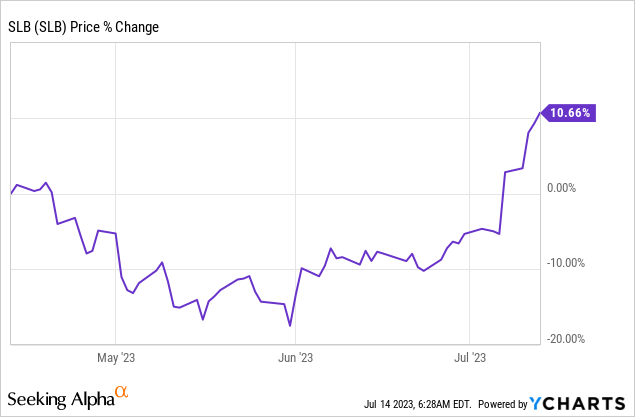

Meanwhile, oil service provider Schlumberger (SLB) has seen a significant turnaround in its stock price and it is now closing in its five-year high stock price.

A few years ago I think there was a lot of talk about the energy sector and whether or not it was going to exist in its current form. From my perspective, there was too much optimism (or completely unrealistic expectations) of how green energy was going to displace our need for hydrocarbon energy. The idea that experts were telling us five years ago about the fall of oil is ironic considering the direction of global demand.

John and Jane are already heavily invested in the energy sector so we aren’t looking to add at the current prices. I think another key takeaway is that the quality of a company like EOG has the potential to move the needle more on positive news (increasing oil prices) compared to many of the large oil companies.

Background

For those interested in John and Jane’s full background, you can find at least three articles a month published for the last five years detailing the performance of their portfolio. I have continued to evolve the report over time by adding and removing information/images to make the updates more useful to the average investor. Here are the key details that should be understood when reading these updates.

- This is a real portfolio with actual shares being traded. This is not a practice portfolio which is why I include screenshots from Charles Schwab to document every change that is made.

- I am not a financial advisor and merely provide guidance based on a relationship that goes back several years.

- John retired in January 2018 and has collected Social Security income as his regular source of income. John also currently withdraws $1,000/month from his Traditional IRA.

- Jane retired at the beginning of 2021 and decided to begin collecting Social Security early and has not made any withdrawals from her retirement accounts yet.

- John and Jane began drawing funds from the Taxable Account in 2022 at $1,000/month. After speaking with them this amount has been increased to $1,700/month. This withdrawal is still covered entirely by dividend and interest income.

- John and Jane have other investments outside of what I manage. These investments primarily consist of minimal-risk bonds and low-yield certificates.

- John and Jane have no debt or monthly payments other than basic recurring bills such as water, power, property taxes, etc.

The reason why I started helping John and Jane with their retirement accounts is that I was infuriated by the fees they were being charged by their previous financial advisor. I do not charge John and Jane for anything that I do.

The only request I have made of John and Jane is that they allow me to publish their portfolio anonymously because I want to help as many people as I can while holding myself accountable and improving my thought process.

I started this series to address issues I have had when reading other authors with similar types of updates (I am not saying they are wrong but I found myself questioning their actual performance because they never provided enough information to cover loose ends).

Here is My Promise to Readers:

- I aim to give as much information as needed so readers can feel confident that what I do is real.

- Even if you agree the results are real this does not mean I expect you to agree with me and I will always answer constructive criticism whenever possible. I will respond with the same genuine intent that the question was asked with.

- I am very transparent about the portfolio and consistency is a significant goal of mine. All of my data points (unless noted otherwise) are derived from month-end statements from Charles Schwab. Even when things aren’t looking great (Spring 2020 for example) you will know because I provide enough information that it would be impossible for me to manipulate.

- This article is not intended to be advice or a call to action and is for informational purposes only (I am not a financial advisor and I don’t claim to be one). My goal is to challenge conventional thinking and empower you to take control of your investments (if that’s something you want to do).

While many authors require paid subscriptions to see their portfolio, I do not want to go that route and will continue to publish this series for free as long as there is enough interest to make it worth my time (and I spend A LOT of time on these articles).

Generating a stable and growing dividend income with an emphasis on capital preservation has become the primary focus of this portfolio. I am least concerned about capital appreciation which is why the decisions made will seem pretty conservative most of the time. I may measure the performance of the portfolio relative to indexes and ETFs but the key metric I am focused on is delivering a more stable source of cash flow to John and Jane over time that allows them to live a comfortable retirement that includes minimal stress related to finances.

Dividend Decreases

No companies in Jane’s Traditional and Roth IRA accounts eliminated or reduced their dividend during the month of June.

Dividend Increases

Three companies paid increased dividends/distributions or a special dividend during the month of June.

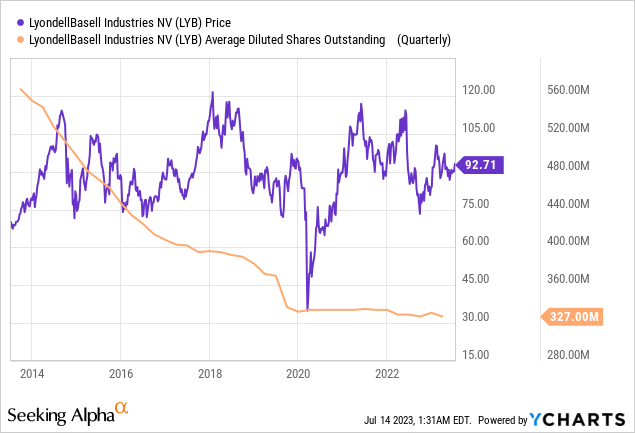

LyondellBasell – LYB has spent the better part of the last three months fluctuating around the $90/share range. LYB is in the process of a transition with regard to focusing on “building a profitable circular and low-carbon solutions business” which also means exiting fossil fuel-related industries such as oil refining (this was recently delayed). I think LYB had a great quarter but they have also used the cash flow to maintain cash reserves of $1.8 billion and additional liquidity of $5.8 billion.

One of the more interesting things about LYB’s management is that they have been incredibly favorable to shareholder returns with an annual target of 70% of free cash flow returned to shareholders. It’s pretty impressive to consider how much shareholders have benefitted from the dividend growth and special dividends but LYB also has one of the best track records of repurchasing shares with the number of shares outstanding less than 60% of where they were 10 years ago.

The dividend was increased from $1.19/share per quarter to $1.25/share per quarter. This represents an increase of 5% and a new full-year payout of $5.00/share compared with the previous $4.76/share. This results in a current yield of 5.37% based on the current share price of $92.71.

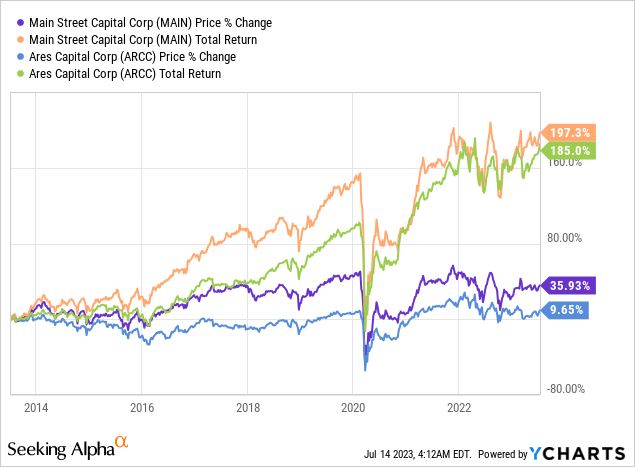

Main Street Capital – The most recent quarter resulted in new quarterly records for net investment income (NII), distributable net investment income (DNII), and net asset value (NAV) on a per-share basis. This has allowed MAIN to continue making regular increases to the dividend and also to issue supplemental dividends when the additional NII becomes even more than what is needed to fund new investment opportunities.

Growing NII and DNII are both good signs for a company like MAIN but another important metric to take note of every quarter is the NAV. At the end of Q1-2023 came in at $27.23/share compared with $25.89. This is probably the most controversial metric in the sense that shares are always selling for around 150% of NAV which means if the company was liquidated there is only enough asset value to justify 67.3% of the current share price. Part of the reason for the significant premium is that the stock is generating dividend and NAV returns that are above average and so MAIN can command a premium which is why buying on pullbacks is so important.

John and Jane both have a pretty significant exposure to MAIN (900 shares in total between all of their retirement accounts) so we aren’t biting at the current price but would definitely look to add more if shares were to drop to $35/share. I used Ares Capital (ARCC) as a comparison below and the major difference in what seems like comparable performance is that during the same time frame (Q1-2022 vs Q1-2023) ARCC’s NAV decreased from $19.03 to $18.45. This means that a significant amount of ARCC’s value proposition is coming from the dividend received because the share price over the last ten years is only up 9.65% (or less than 1% per year) even though the total return is 185% when dividends are included.

A supplemental dividend of $.225/share was issued during the month of June.

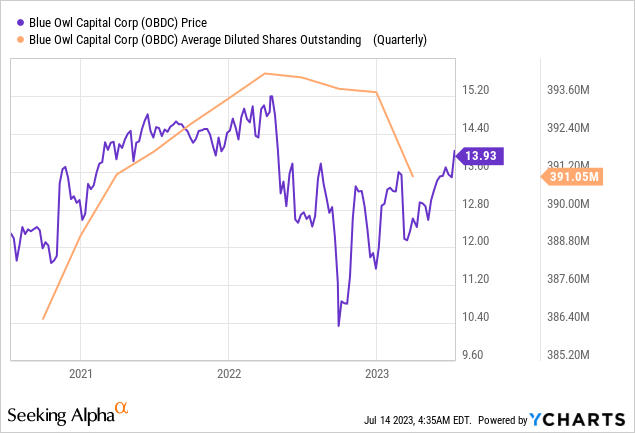

Blue Owl Capital Corporation – Recently changed from Owl Rock Capital (ORCC) to Blue Owl Capital Corporation (OBDC) due to some turmoil between the founders with the goal of aligning the company under Blue Owl Capital (OWL). The name change is the least interesting thing to happen to OBDC as the company has seen a surge in the NII generated which came in at a record of $.45/share for Q1-2023 compared with $.31/share for Q1-2022. For those who are interested in better understanding how this situation evolved check out my article Owl Rock Capital – Build A Position Before Q3 2022 For Maximum Upside from May 28th, 2022 where I explain how the value proposition of OBDC was set to improve significantly.

Although future rate hikes are likely to be more tame, OBDC is still set to benefit for the next few years from the increased NII which is likely to result in reasonably small dividend increases with the issuance of supplemental dividends when needed.

Another interesting item is that with NII so strong it looks like OBDC is going to be able to truly fund new investment activities from the NII created by its investments whereas it has been reliant on issuing more shares in the past to grow its holdings because the NII generated compared with the quarterly dividend payment were quite slim.

A supplemental dividend of $.06/share was issued during the month of June.

Retirement Account Positions

There are currently 38 positions in Jane’s Traditional IRA and 22 in Jane’s Roth IRA. While this may seem like a lot, it is important to remember that many of these stocks cross over in both accounts and are also held in the Taxable Portfolio.

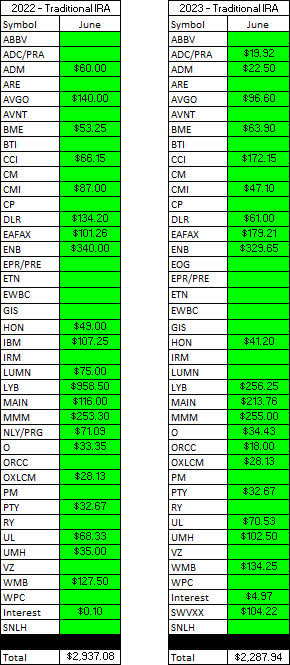

Below is a list of the trades that took place in the Traditional IRA during the month of June.

Traditional IRA – 6-2023 – Trades (Charles Schwab)

Below is a list of the trades that took place in the Roth IRA during the month of June.

Roth IRA – 6-2023 – Trades (Charles Schwab)

I apologize ahead of time regarding my tardiness in writing the article explaining my recent trades especially when it comes to Digital Realty (DLR). I do plan on writing this article soon but I recently had to spend all of my free time rebuilding a large retaining wall that encroached on my neighbor’s property. With the important part of that project behind me, I do plan on getting back to writing more than just my usual Saturday articles.

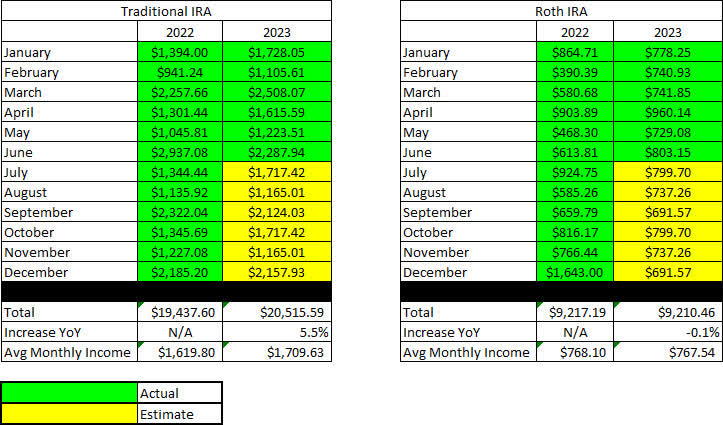

June Income Tracker – 2022 Vs. 2023

The account is set for modest dividend growth in the Traditional IRA and a slight decrease in the dividend income generated by the Roth IRA. Similar to the Taxable Account, the number of special dividend payouts in 2022 increased the yield of the portfolio at a faster pace (16.9% and 29.6% growth, respectively). While it’s possible we could see more special dividends in 2023 I think it’s more likely that management will focus on deleveraging the balance sheet or stock buybacks in most cases.

The Traditional IRA is expected to generate an average of $1,709.63/month of dividend income in 2023 compared to the average monthly income of $1,619.80 generated in FY-2022. The Roth IRA is expected to generate an average of $767.54/month of dividend income in 2023 compared to the average monthly income of $768.10 generated in FY-2022.

Remember that these figures above are provided as a snapshot in time and do not include dividend increases that have not occurred and err on the side of a more conservative payout. Almost every month when I update these numbers there is growth over my original projections, some of which, are related to human error because it’s possible I forgot to increase/update the dividends expected in future months. With higher yields on money markets and CDs, I expect we will see a very light increase in dividend income for the year of around 3-4% (Roth & Traditional IRA combined growth).

At this point, Jane has decided she will not be making any withdrawals from these accounts which means that the dividends will be collected as cash and potentially reinvested when it makes sense.

SNLH = Stocks No Longer Held – Dividends in this row represent the dividends collected on stocks that are no longer held in that portfolio. We still count the dividend income from stocks no longer held in the portfolio, even though it is non-recurring. All images below come from Consistent Dividend Investor, LLC. (also referred to as CDI as the source below).

The tables below represent which companies paid dividends in May and how that income source has changed compared to the same month of the previous year.

**It should be noted that the main reason for the dividend income being higher in June 2022 was due to a large special dividend issued by LYB. Without this special dividend, the income generated in June 2023 would have been higher than in June 2022.

Traditional IRA – 2022 V 2023 – June Dividends (CDI)

Roth IRA – 2022 V 2023 – June Dividends (CDI)

The table below represents all income generated in 2022 and collected/expected dividends in 2023.

Retirement Projections – 2023 – June (CDI)

Below gives an extended look back at the dividend income generated when I first began writing these articles. I find this table to be most useful when comparing how dividend income has improved for a specific month over the course of six years.

Retirement Projections – 2023 – June – 6 YR History (CDI)

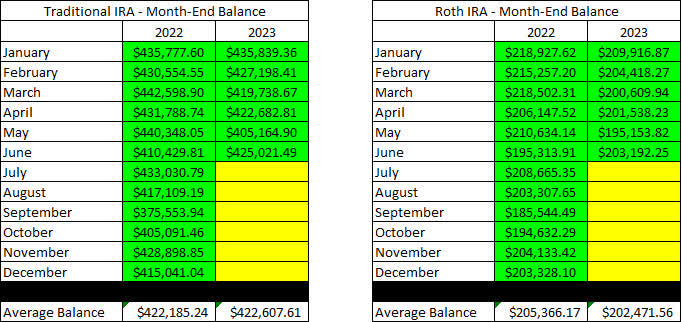

The balances below are from June 30, 2023, and all previous month’s balances are taken from the end-of-month statement provided by Charles Schwab.

Retirement Account Balances – 2023 – June (CDI)

The next image is also pulled from the end-of-month statement provided by Charles Schwab which shows the cash balance of the account.

**Please note that cash balances may fluctuate based on CD renewal dates and the use of SWVXX because I only count the cash that is 100% liquid. There were larger fluctuations in 2019 and 2020 that we the result of deposits and withdrawals being made. There will be no contributions made into either account in 2023 now that Jane is no longer working.

Retirement Projections – 2023 – June – Cash Balances (CDI)

The next image provides a history of the unrealized gain/loss at the end of each month going back to the beginning of January 2018.

Retirement Projections – 2023 – June – Unrealized Gain-Loss (CDI)

I think the table above is one of the most important for readers to understand because it paints a story of volatile markets and why we employ the strategy of generating consistent cash flows to overcome the uncertainty of the market. If we were dependent on selling shares to generate income for John and Jane’s retirement, they would have to be much more considerate of when they withdraw and how much they choose to withdraw.

For example, a withdrawal in 2020 where shares must be sold would destroy more value by locking in losses or poor performance by stocks being sold compared to making the same withdrawal in 2021.

In an effort to be transparent about Jane’s Accounts, I like to include an unrealized Gain/Loss summary. The numbers used are based on the closing prices from July 14th, 2023.

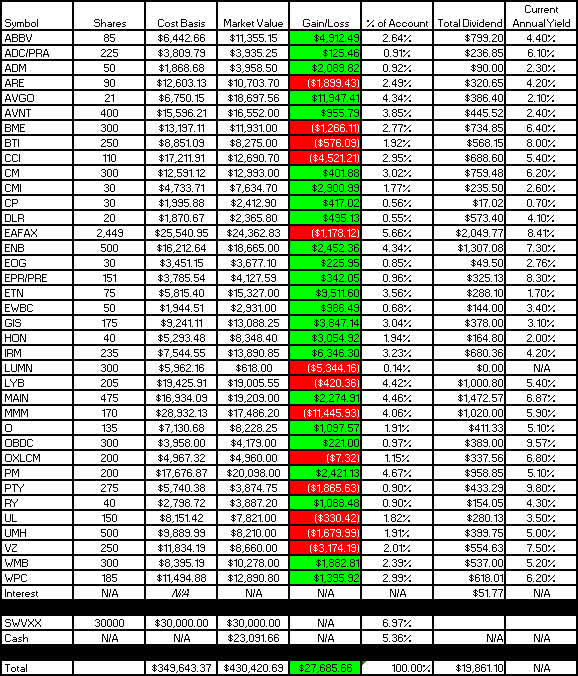

Traditional IRA – 2023 – June – Gain-Loss (CDI)

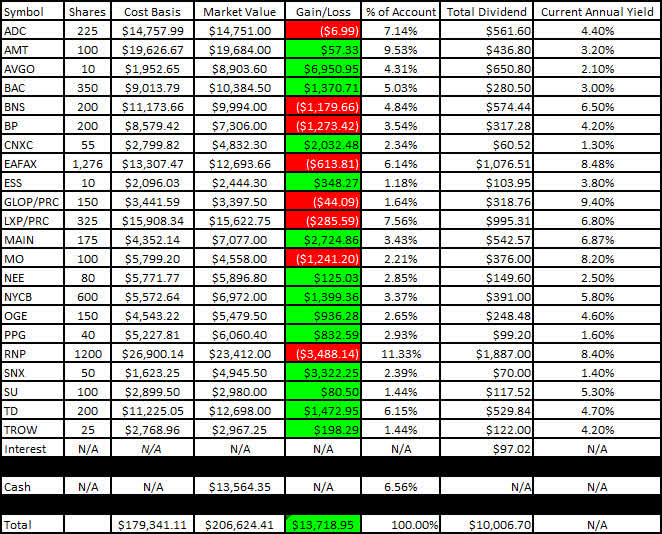

Roth IRA – 2023 – June – Gain-Loss (CDI)

**I received some feedback on the yield column and have updated the column to now reflect the actual yield of the stock based on the most recently updated share price.

Conclusion

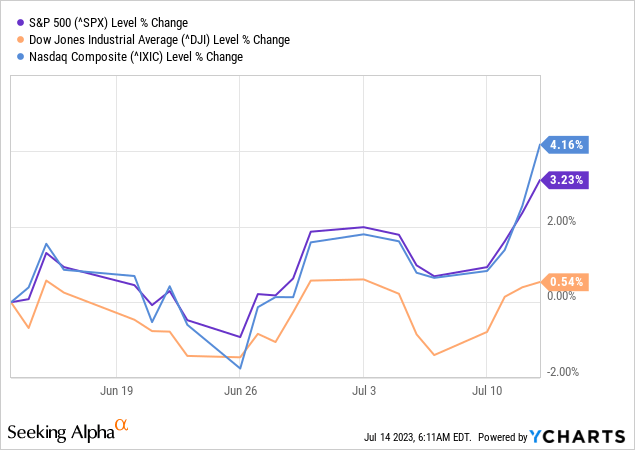

The month-end balances associated with the Traditional and Roth IRAs are both doing quite well compared to the balances at the end of May. The Gain-Loss tables also show that the account balances are still performing well halfway through the month of July with the balances up several thousand compared to the balances at the end of June.

The increase in account balance is tied to the market value of the holdings. Looking at the three most common indexes we can observe that the increase in value lines up with the changes we have seen over the last month in the S&P 500 (SPX), Dow Jones Composite (DJI), and Nasdaq Composite (IXIC).

Expect to see more sales coming soon as we use the current momentum of the market to increase the cash holdings and invest in more “risk-free” holdings such as Schwab Money Market (SWVXX), CDs, and Treasuries.

June Articles

I have provided the link to the June 2023 Taxable Account below.

The Retirees’ Dividend Portfolio: John And Jane’s June 2023 Taxable Account Update

In Jane’s Traditional and Roth IRAs, she is currently long the following mentioned in this article: AbbVie (ABBV), Agree Realty (ADC), Agree Realty Preferred Series A (ADC.PA), Archer-Daniels-Midland (ADM), Broadcom (AVGO), Avient (AVNT), Bank of America (BAC), BlackRock Health Sciences Trust (BME), Bank of Nova Scotia (BNS), BP (BP), British American Tobacco (BTI), Canadian Imperial Bank of Commerce (CM), Cummins (CMI), Concentrix (CNXC), Digital Realty (DLR), Eaton Vance Floating-Rate Advantage Fund A (EAFAX), Enbridge (ENB), EOG Resources (EOG), EPR Properties Preferred Series E (EPR.PE), Eaton Corporation (ETN), East West Bancorp (EWBC), Essex (ESS), General Mills (GIS), GasLog Partners Preferred C (GLOP.PC), Honeywell (HON), Iron Mountain (IRM), Lexington Realty Preferred Series C (LXP.PC), Lumen Technologies (LUMN), LyondellBasell (LYB), Main Street Capital (MAIN), 3M (MMM), Altria (MO), NextEra Energy (NEE), New York Community Bank (NYCB), Realty Income (O), OGE Energy Corp. (OGE), Blue Owl Capital Corporation (OBDC), Oxford Lane Capital Corp. 6.75% Cum Red Pdf Shares Series 2024 (OXLCM), Philip Morris (PM), PPG Industries (PPG), PIMCO Corporate & Income Opportunity Fund (PTY), Cohen & Steers REIT & Preferred Income Fund (RNP), Royal Bank of Canada (RY), Schwab Value Advantage Money Fund (SWVXX), TD SYNNEX (SNX), Toronto-Dominion Bank (TD), T. Rowe Price (TROW), Unilever (UL), UMH Properties (UMH), Verizon (VZ), Williams Companies (WMB), W. P. Carey (WPC).

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

{kind=link}