The natural gas industry is currently at a crossroads, and factors ranging from weather conditions to geopolitical tensions significantly impact it. With the U.S. storage levels lower than expected and European inventories reaching multi-year lows, the market is poised for fluctuations that could impact both consumers and industries. Concerns over tariffs, high LNG exports, and trade tensions add further complexity to this situation. So, this analysis will explore key factors driving natural gas prices and assess how they could affect the market dynamics in the coming months.

Storage Levels. United States

According to the latest EIA report released on April 10, 2025, working natural gas in underground storage in the Lower 48 states totaled 1,830 billion cubic feet (Bcf) as of April 4. This represents a net weekly increase of 57 Bcf, signaling the early phase of the spring injection season. However, storage levels remain 450 Bcf below last year and 40 Bcf below the five-year average of 1,870 Bcf for this time of year. The largest weekly increases were observed in the South Central region (+31 Bcf) and East (+12 Bcf), but overall, the U.S. enters the refill season with inventories on the low side, which could support gas prices if injections fall short or demand surprises to the upside.

The U.S. has just concluded its winter withdrawal season, and attention is turning to storage refill. Lower-than-average storage can put upward pressure on prices because more gas needs to be bought and stored in the coming months. However, the impact on price will also depend on how fast production can refill the gap and what summer demand looks like.

Storage level. Europe

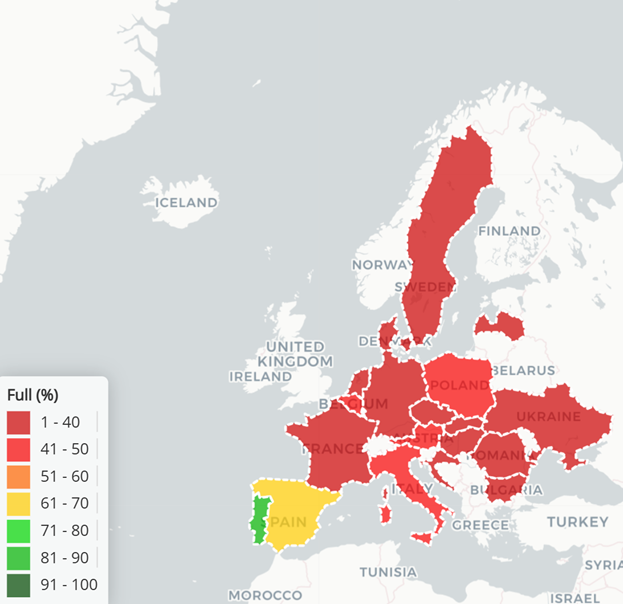

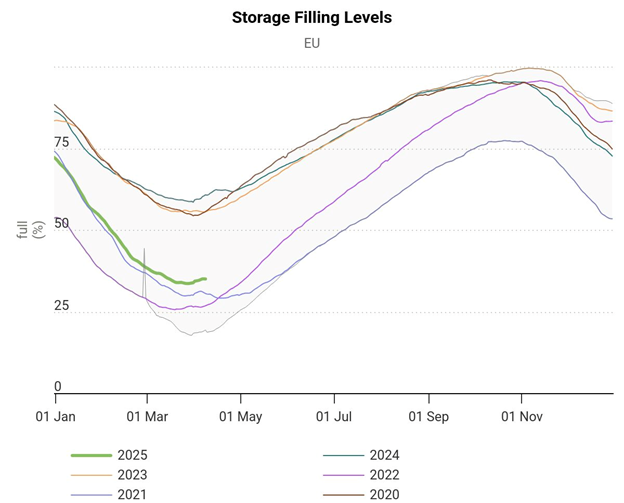

In contrast to the U.S., Europe’s gas inventories are at relatively low levels coming out of winter. European storage sites were drawn down significantly due to the extended cold and the need to replace reduced pipeline flows (as Europe continues to diversify away from Russian gas). By early April, EU storage facilities were reported to be only around 30% full, a multi-year low for the season.

Source: https://agsi.gie.eu/data-visualisation/filling-levels-country/map

This is well below the unusually high levels seen a year ago (Europe had entered spring 2024 with storage still ~50% full, thanks to a mild winter). The low inventories now are a bullish indicator for demand: Europe will have to aggressively refill storage over the spring and summer to prepare for next winter. That means Europe will be importing large volumes of gas (via both pipeline and LNG). European buyers are already booking LNG cargoes for delivery in the coming months to catch up on storage needs. This strong refill demand from Europe provides underlying support for natural gas prices globally, as it ensures that a key source of consumption (European utilities) will remain in the market for gas even during the off-peak season.

Source: https://agsi.gie.eu/data-visualisation/filling-levels/EU

Weather Conditions in the United States and Europe

In the United States, parts of the country have experienced colder-than-normal temperatures in early April. A late-season cold snap in the Midwest and Northeast has boosted heating demand for natural gas in those regions. This unusual chill has extended the heating season slightly beyond its typical end, leading to higher residential and commercial gas usage than would normally be expected in spring. In contrast, other areas of the U.S. are beginning to warm up with the advance of spring. Milder conditions in the South and West are reducing overall heating needs, helping to offset some of the increased demand from colder regions. As April progresses, the balance between lingering heating demand and the onset of early cooling demand (for example, in warmer climates where air-conditioning might ramp up) will continue to influence natural gas consumption. If we look at the temperature forecast, we see a favorable picture for many parts of the United States.

Source: https://www.cpc.ncep.noaa.gov/

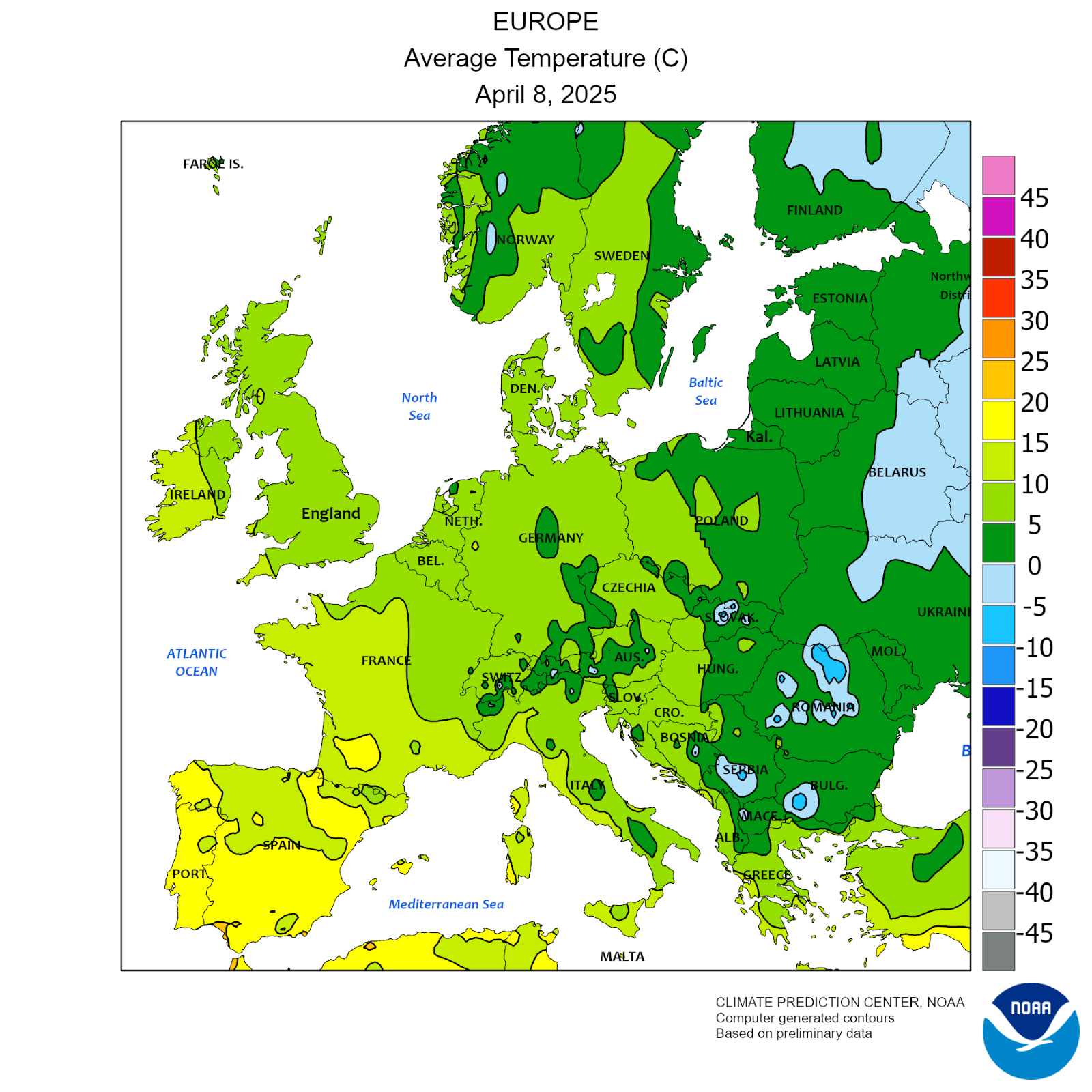

In Europe, the tail end of the winter has also seen cooler weather in certain areas, which has kept heating demand elevated later than usual. Some European countries faced a colder-than-average March, resulting in continued withdrawals from gas storage into early April. However, Europe is now gradually transitioning into milder spring conditions. As temperatures rise, heating demand is tapering off across much of the continent. This seasonal demand swing is critical because Europe relies heavily on natural gas for heating.

Source: https://www.cpc.ncep.noaa.gov/products/JAWF_Monitoring/Europe/temperature.shtml

U.S. Tariffs on Gas and Impact on China

Concerns about a potential recession are emerging as a bearish factor for natural gas demand. Rising trade tensions and the introduction of new tariffs have fueled fears of an economic slowdown, which could lead to a broader decline in industrial activity and overall energy consumption. In a recessionary environment, demand for electricity and heating typically weakens, reducing the need for natural gas across multiple sectors — from manufacturing to power generation. This uncertainty may weigh on gas prices, offsetting some of the upward pressure from structural demand growth drivers like LNG exports.

A major policy development affecting global gas markets is the prospect of new U.S. tariffs on liquefied petroleum gas (LPG) and liquefied natural gas (LNG) exports. The U.S. government is considering tariffs on outbound LPG and LNG cargoes. This move is partly rooted in ongoing trade tensions and aims to address perceived imbalances. China, as one of the world’s largest importers of LPG and a significant buyer of LNG, is directly impacted by this. Anticipation of the tariffs has already begun shifting trade flows: Chinese importers are reportedly scaling back purchases of U.S. LPG/LNG in expectation of additional costs. Instead, they are exploring alternative suppliers – for instance, sourcing more LPG from the Middle East and LNG from other exporters like Qatar or Australia.

On April 9, 2025, China imposed an 84% tariff on U.S. liquefied petroleum gas (LPG) imports, forcing Chinese petrochemical plants to consider production cuts or shutdowns. In response, the U.S. raised tariffs on Chinese imports, including energy products, to 125%, following successive increases from 10% in February and 54% in early April. The measures are raising trade tensions and affecting global gas flows, including a shift in U.S. exports to Europe and Southeast Asia.

The ripple effects on global gas markets could be substantial. If Chinese buyers pull back from U.S. exports, those U.S. cargoes will need to find other homes. Europe is a likely destination for displaced LNG, given its ongoing demand for gas, as are other Asian nations without tariff barriers. In the short term, such a rerouting could reduce shortages in certain markets (which could put pressure on prices in Europe or other regions) while reducing supplies to China. For example, European gas prices could face downward pressure if more U.S. LNG heads their way, whereas Asian spot LNG prices might rise if China’s usual suppliers divert volumes to cover the gap.

U.S. Production and Storage Trends

American natural gas production remains robust and continues to trend near record highs. According to data from S&P Global Commodity Insights, the average total supply of natural gas increased by 2.0% (2.2 Bcf/d) compared to the previous report week. This growth was driven by a 0.5% rise in dry natural gas production, which reached an average of 105.8 Bcf/d, and a 35.8% increase in net imports from Canada, adding an additional 1.7 Bcf/d to the supply. Compared to the same period last year, supply levels are notably higher, ensuring ample domestic availability. This elevated supply continues to act as a stabilizing force on prices, helping to cushion the market against sharp upward moves during periods of increased demand.

High U.S. LNG Exports

The United States has become one of the world’s top LNG exporters, and export levels are currently very high. In recent weeks, feed gas deliveries to U.S. LNG export terminals have been hovering around 13.0–13.5 Bcf/d, close to the operational capacity of those facilities. This is a record or near-record level of LNG exports for the U.S., up from roughly 11–12 Bcf/d a year ago. Essentially, U.S. export terminals are running full out. Strong demand from Europe and Asia for LNG has kept U.S. export volumes maxed despite it being spring.

These high exports have several implications for the domestic market. First, they act as a release valve for U.S. production: a significant portion of U.S. gas output is being pulled off the domestic market and sent overseas. This can tighten the domestic supply-demand balance and lend support to U.S. prices, especially in regions connected to LNG export facilities. For example, natural gas prices in the Gulf Coast area have occasionally been stronger than Henry Hub because of the pull from LNG terminals. Second, high LNG exports contribute to the lower storage levels mentioned above – gas that might have gone into U.S. storage is instead cooling into liquid and boarding tankers. As long as global gas prices (like European TTF or Asian spot LNG) remain higher than U.S. prices, U.S. LNG exports will stay robust. In the short term, scheduled maintenance at LNG terminals in spring could slightly dent export volumes, but so far export demand has been relentless. This means the U.S. market will need to balance via production increases or demand adjustments, because the international outlet is effectively running at full capacity.

Conclusion

Natural gas prices have shown notable volatility over the past couple of weeks, with a recent downward trend replacing the modest gains seen earlier in April. As of April 9, 2025, the Henry Hub spot price had dropped by 62 cents from $4.05 per MMBtu the previous Wednesday to $3.43/MMBtu. Similarly, the May 2025 NYMEX front-month futures contract declined by 24 cents, from $4.055/MMBtu to $3.816/MMBtu, while the 12-month strip (averaging May 2025 through April 2026 contracts) fell by 29 cents to $4.267/MMBtu. This recent pullback comes despite ongoing support from strong LNG exports and prior weather-driven demand.

The U.S. Energy Information Administration’s Short-Term Energy Outlook released this week projects that natural gas prices will gradually rise later in the year. This implies some upside from current levels. However, the next few weeks are a shoulder season with generally mild weather, which could cap significant price rallies in the very short term.

If injections into storage turn out to be very strong (due to high production and moderate demand), prices could stall or even pull back temporarily in late April and May. On the other hand, any early heat waves or unplanned supply outages (for example, a surprise drops in production or a hiccup at a major processing plant) could cause short-term price spikes.