I’m in Copenhagen talking with a few key stakeholders and seeing why this might be and what can be taken actions can be taken to put things right similar travails have happened in the UK’s regional wars and COVID have taken their toll on the supply chain leaving many turbine companies suffering and those behind providing incentives scratching their heads as to why traditional means of driving down costs

The Danes are leaders in the energy transition and that is reflected in name changes as Danish Oil and Gas, DONG, transitioned into Orsted the world’s most sustainable company with stakeholders ranging from global banks to regional pension funds. We await stateside developments under the new administration with those bidding in recent BOEM rounds likely to face a tough battle to progress

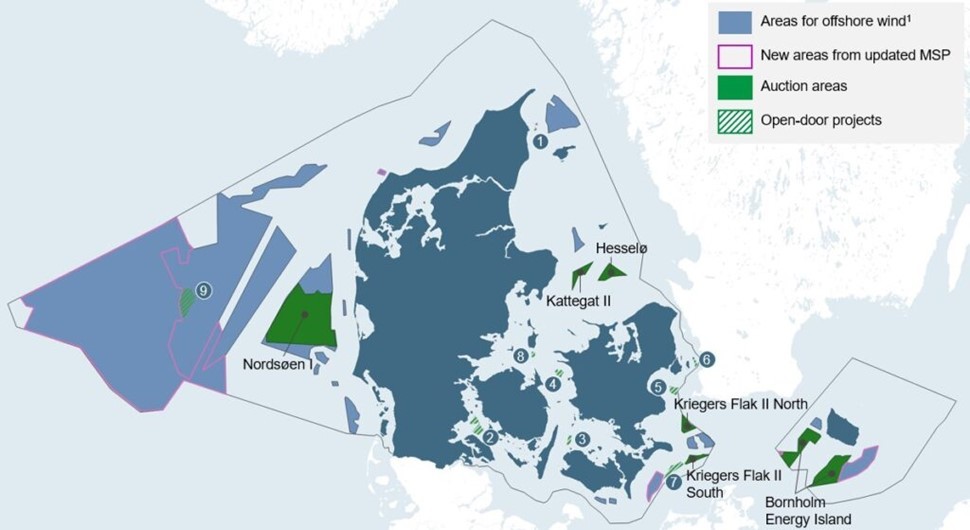

The auction model was modified by the Danes who came up with a ‘society-minded’ new-look leasing model as the Danish Energy Agency (DEA) announced the country’s much-vaunted ‘open door’ scheme was being shut down due to fears of a possible breach of EU rules, stranding some 15GW of projects, and prompting Orsted CEO Mads Nipper to entreat the Danish climate and energy minister make sure Brussels didn’t “stand in the way for accelerating green power in Denmark and Europe”.

Within weeks, the Danish government had unveiled plans for new auctions totalling 9GW in five areas to help dampen the impact of the pivot away from the ‘old’ model, which was as credited with speeding up the pace of build-out off the coast of Denmark by allowing subsidy-free offshore wind farms to be constructed without waiting on government auctions.

In May it was revealed that overall design of the coming auctions would have a new-look framework that was lease-based rather than underwritten by government subsidy, but fresh crosswinds blew up last month when an updated marine spatial plan (MSP) was published that put a halt to some 20GW of offshore wind projects already underway.

A couple of aspects of the Danish situation is that the some of the Nordic companies have generous export guarantee underpinnings which enable the supply chains to have surety that they will be paid where the projects proceed or not and give them first place in the queue when it comes to the gaining of pressurised resource including offshore wind vessels other countries have got sovereign wealth funds which are increasingly viewed by global investors as a mechanism to promote the energy transition.

In the UK the idea is that of the offshore wind sector can actually provide many lessons for the nation’s hydrogen sector not least the clustering approach and in the way that accept that can almost bootstrap it – if the seed funding is applied in the right manner at the right time.

As the tumbleweed goes round Copenhagen this may be due for a challenge especially as in some parts of the world the fossil fuel sector is showing signs of recovery using the energy security argument to make sure that their shareholders prevailed.

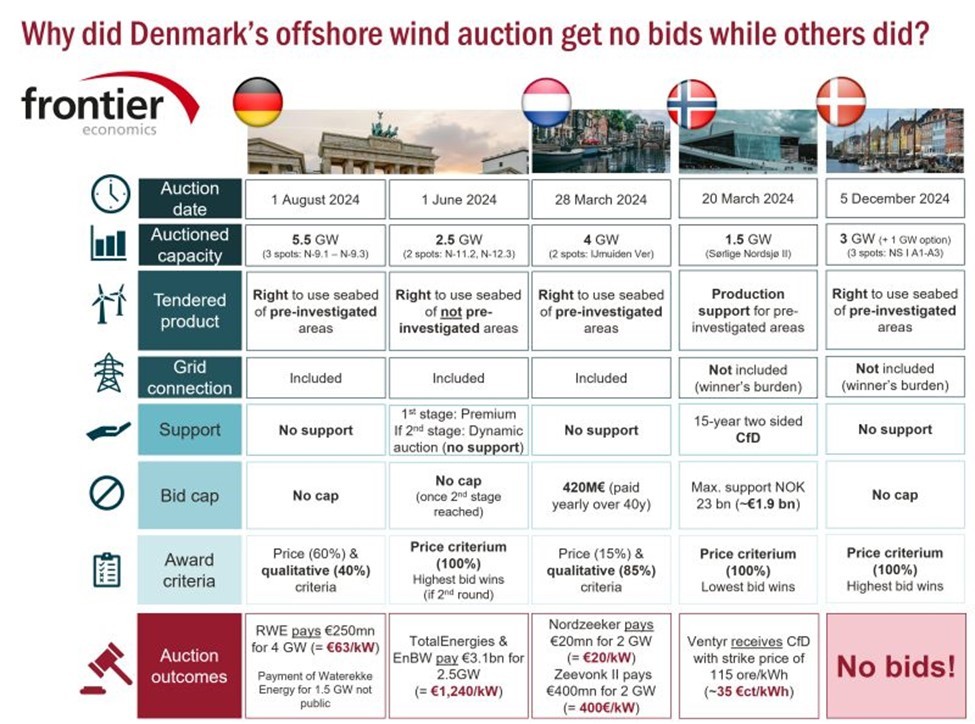

Several observers blame this on the lack of subsidy or revenue stabilisation mechanism that come with the auction. Instead, project developers had to bid how much they are willing to pay for the right to build the wind farm, and there is no bid cap and no qualitative award criteria.

The notion of auctions themselves also appears to be encountering problems in recent weeks are shared an informative article by former Crown Estate man Matthew Bleasdale indicating that the model itself may be fundamentally flawed and acting as a brake on a sector which should be ready for global take off.

Clearly, project developers prefer to receive a premium or a Contract-for-Difference that guarantees a certain electricity price (‘strike’) rather than to pay to the government and remunerate these payments and development costs via market revenues alone. Countries such as UK, Norway or Belgium indeed use CfDs. As for the auction system, which Bleasdale questions; hydrogen-auction-design-report in 2024 developers where willing to pay to the government in Germany TotalEnergies and bp with €12.6 billion for 7 GW in not pre-investigated areas in 2023, and TotalEnergies and ENBW €3.1 billion for 2.5 GW in 2024.

Denmark’s 1 GW Thor wind farm was previously contested by developers willing to pay for the rights that the winner the German RWE won via a follow up lottery.

Why so different this time for Denmark?

Everything of course comes down to cost. These increased substantially due to rising commodity prices and interest rates. Supply chain challenges create additional uncertainties. In Denmark, unlike in Germany or the Netherlands, successful bidders have realise the grid connection, adding substantial extra costs – and risk.

it’s a case now of reassessing and how to make it work something similar happened in the UK wherever lower prices to the consumer meant projects are not actually being delivered and the consumer losing out in the long run. Sticking plaster solution emerged with a New Labour government increasing the various prices for the baseline price which enable some of the round four round 5 projects to proceed

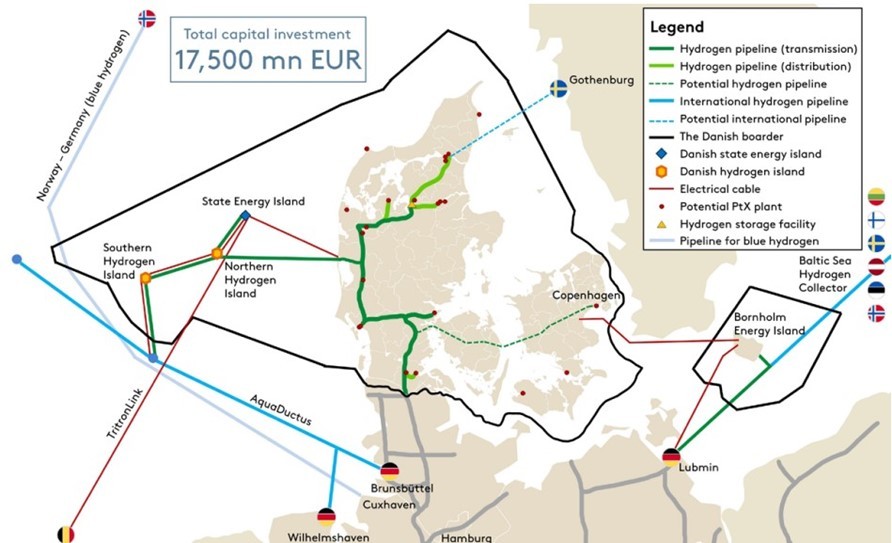

To achieve its goal of adding 6 GW offshore wind by 2030, Denmark has now to consider adapting the auction design for the next 3 GW auction (bids due in April 2025) and re-tender the 3 GW from the last auction. One additional question is whether the northern arm of the European Hydrogen Backbone can play a role to reduce electrical connection costs and increase revenue perspectives as may be easier to store and transport as a gas.

Charley Rattan Associates operate at the forefront of sectoral developments, click through https://lnkd.in/eMx4PHv4 to view our Hydrogen training and advisory services

Season’s greetings and a happy New Year

Stay informed at the moderated focus-group; Offshore Wind and Hydrogen