The possibility that Saudi Arabia will lift the “floodgates” on its oil production has climbed in recent weeks, fueled by “deteriorating cohesion” among the group of major oil producers known as OPEC+, according to a report from Capital Economics released Monday.

A “sense of frustration is clearly building,” Kieran Tompkins, climate and commodities economist at Capital Economics, wrote in Monday’s note. “Although the focus in the oil market has shifted to geopolitical risks and potential short-term supply disruptions, just as importantly, we think the possibility that Saudi Arabia could open the floodgates has increased in recent weeks alongside reports of deteriorating cohesion among OPEC+ members.”

Most Read from MarketWatch

Producers in OPEC+ — comprised of the Organization of the Petroleum Exporting Countries and its allies — who have been implementing voluntary production cuts have overproduced by as much as 800,000 barrels per day, he said.

Earlier this month, the Wall Street Journal reported that Prince Abdulaziz bin Salman, Saudi Arabia’s oil minister, warned fellow producers in a conference call that oil could drop to $50 a barrel if they don’t comply with agreed production cuts. OPEC said on X, however, that the article falsely reported that a conference call took place. “The OPEC Secretariat categorically refutes the claims made within the story as wholly inaccurate and misleading.”

Tompkins also pointed out that a Sept. 26 article from the Financial Times suggested that Saudi Arabia would comfortably weather a period of lower oil prices through alternative funding measures. That “strikes of a not-so-subtle reminder it has the ability to ‘punish’ ‘cheating’ producers,” said Tompkins, who titled his note: “It is when, not if, Saudi Arabia opens the oil taps.”

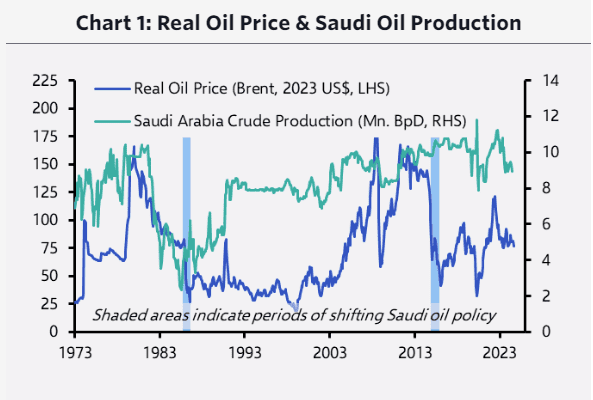

In the past, marked shifts in Saudi Arabia’s oil policy, in the mid-1980s and mid-2010s, led to declines in oil prices.

In a note last month, Capital Economics’ James Swanston, a Middle East and North Africa economist, had also said that the case for Saudi Arabia to ramp up oil output was strengthening. A ramp-up, he said, would result in some economic pain and require Crown Prince Mohammed bin Salman to reverse course on his approach to oil policy since coming to power, but it would “enable the Kingdom to recapture market share.”

For now, the current oil-market backdrop probably does not suggest that a big shift in oil policy is imminent, said Tompkins. Saudi Arabia’s current situation is “nowhere near as dire as it has been in the past,” he said. For example, the Saudis had cut oil production by 75% in the lead-up to their reversal on oil policy in the mid-1980s, but since September 2022, it has cut output by nearly 20% — suggesting that the Kingdom “isn’t in quite as concerning a position now.”

If Saudi Arabia did ramp up production to its capacity of 12.5 million barrels per day, from around 9 million bpd, it would require a sizeable fall in oil prices below $50 a barrel for its oil export revenues to be “markedly worse than they are today,” said Tompkins.

In Monday dealings, global benchmark Brent crude’s December contract BRN00 BRNZ24 traded at $77.60 a barrel on ICE Futures Europe, down $1.44, or 1.8%.

“All told, the risks to our view that Saudi Arabia open the spigots and ramps up output at some point have increased, perhaps to around a 30% chance by end-2025,” Tompkins said.

The OPEC+ meeting scheduled for Dec. 1 will be key. In September, OPEC+ agreed to extend voluntary production cuts by two months to the end of November and then gradually phase out the cuts on a monthly basis at the start of December.

“One of the lessons from 2014 and 2020 was that a breakdown of negotiations around these meetings led to Saudi shifting tack,” Tompkins said. “The December meeting could be a potential flashpoint.”