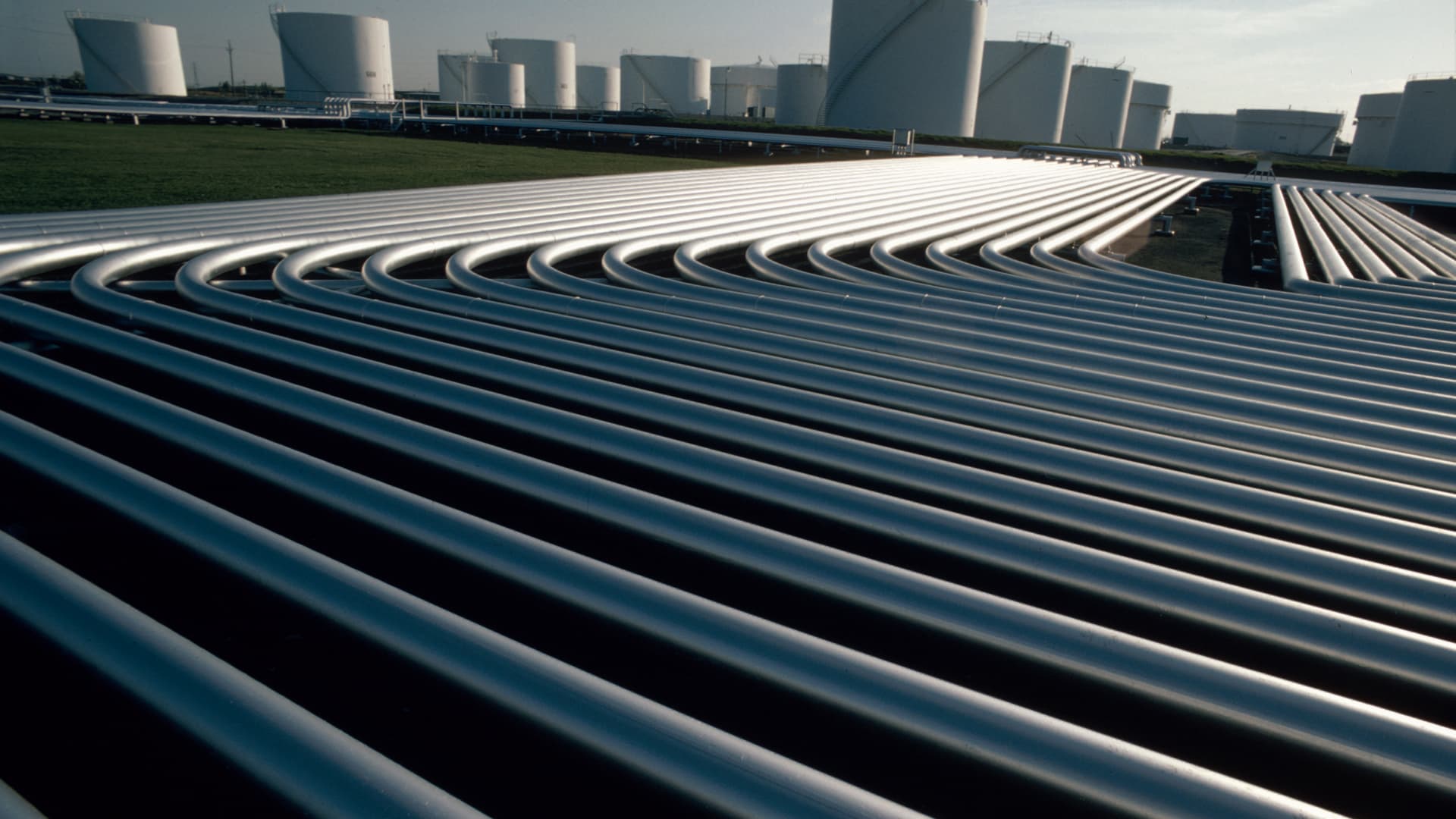

Pipeline operator Williams Companies offers a way for investors to play rising natural gas prices as demand grows due to the transition away from coal, according to the research firm Argus. Argus upgraded Williams to buy on Thursday with a price target of $47 per share, which implies 17% upside from Tuesday’s close if the company’s 4.5% dividend yield is included. “Our upgrade largely reflects our more bullish stance on natural gas prices,” analyst Bill Selesky told clients in a research note Thursday. Demand for natural gas should rise due to hot weather conditions and the transition from coal to gas, while supply is constrained and inventories are low, the analyst said. Williams operates a gas pipeline network in the U.S. that spans more than 30,000 miles, connecting needed supply to key demand regions, Selesky said. Williams hit a 52-week intraday high of $42.60 on Thursday, with the company’s stock nearly 22% this year. The pipeline operator has rallied as natural gas prices have bounced back 70% over the past two months. The bounce back comes after the stock cratered to a low of $1.482 per thousand cubic feet on April 26. The early summer heat wave through much of the U.S. drove natural gas prices up to $3.09 per thousand cubic feet on June 10, the highest level since January, as electricity demand increased. At the same time, gas production is expected to fall by 1% in 2024 due to the recent period of very low prices, according to the Energy Information Administration. WMB 1Y mountain Williams stock over the past year. “Williams is a great company,” Jenny Harrington, CEO of Gilman Hill Asset Management, told CNBC’s “Halftime Report” on Thursday. “They are a direct beneficiary from the demand in energy and the demand in power.” “There’s a lot of opportunity in midstream, and I like being in midstream because you get away from the commodity exposure,” Harrington said. Wells Fargo upgraded Williams earlier this month to overweight with a price target of $40.98, which implies 10% upside — or 14.6% including the dividend — from Tuesday’s close. Natural gas demand is expected to grow over the next few decades due to increased electricity demand from artificial intelligence , the return of manufacturing to the U.S., and the electrification of the U.S. vehicle fleet, according to Wells. Williams CEO Alan Armstrong told analysts on the company’s May earnings call that the current period of low natural gas prices offers a bargain for utilities that are forecasting electricity load growth. “The power-hungry world we live in is rapidly turning to natural gas to generate this power,” Armstrong said. “This, compounded with the hard-to-miss growth in LNG exports and data centers, as well as the continued drumbeat of electrify everything and re-shore it, is accelerating demand and the expansions of our uniquely placed infrastructure will demand a premium,” the CEO said. Half of Wall Street analysts currently rate Williams the equivalent of a buy, while 45% are recommending a hold on the pipeline operator’s stock. About 4.5% say sell, according to FactSet. The company’s stock has already outpaced an average price target of $41.89. Shares closed Thursday at $42.40.

This pipeline stock could surge 17% on rising natural gas prices and coal phaseout, Argus says

About the author

Related Articles

-

Energy Department Extends Emergency Order in New England Ahead of Second Winter Storm

-

Las Vegas teen charged after alleged brutal group sexual assault on private school field trip caught on video

-

Energy Department Extends Emergency Orders in the Carolinas and Mid-Atlantic Ahead of Second Winter Storm

{kind=link}