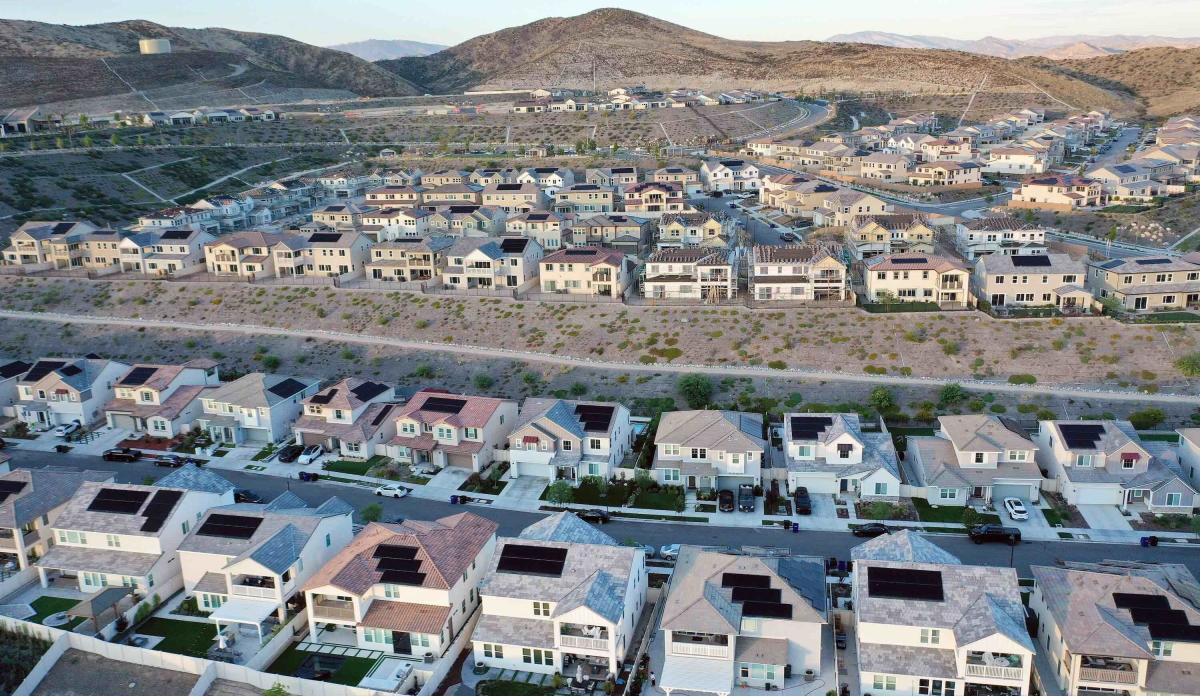

California slashed the value of rooftop solar for customers of its three biggest utilities last year — and installations of residential solar systems in the state have fallen to near-three-year lows since then.

But drawing firm conclusions about how the controversial shift in net-metering policy will shape California’s rooftop solar market over the long term — and affect the state’s grid-decarbonization and energy-equity goals — is a lot more complicated than it looks.

Just ask Galen Barbose, staff scientist at the Department of Energy’s Lawrence Berkeley National Laboratory. Last week, he released a report compiling the latest data on California’s residential rooftop solar market, including the data point showing a marked drop in installations in the first three months of 2024.

Barbose also scrutinized battery-storage attachment rates, the distribution of solar adopters by geography and income, third-party ownership, system sizing, pricing, and installer market share. The goal was to reveal “initial empirical insights into how the market has evolved over the past year, confirming some expectations while also revealing several striking surprises,” he wrote in the report.

But “we have to be careful about not overreaching from the data over this past year,” Barbose stressed in an interview with Canary Media — because “this was a strange last year.”

A year of twists and turns for California rooftop solar

There was a huge rush to apply for and secure interconnections of rooftop solar systems to the grid in the runup to April 2023, when the legacy net-metering (NEM) tariff was officially replaced by the “net-billing tariff” (NBT) that the California Public Utilities Commission imposed on customers of Pacific Gas & Electric, Southern California Edison, and San Diego Gas & Electric.

That caused installations to spike to record levels throughout the spring and summer of 2023, as all of the projects approved under the old tariff got underway. Installations under the legacy tariff continued even through the first quarter of 2024, according to LBNL data.

Backers of the CPUC’s decision to reduce compensation for rooftop solar argue that California’s solar market remains robust — just not as overheated as during the historical jump in installations last year.

“[T]he much more generous compensation for systems installed before April 15 drove a gold rush during the first three and a half months of 2023,” Severin Borenstein, head of the Energy Institute at the University of California, Berkeley’s Haas School of Business and a foe of the state’s previous net-metering regime, wrote in a blog post last month. “Many of those early-2023 buyers would most likely have been later-2023 buyers were it not for the rush to install before April 15 and lock in NEM 2.0 rules.”

But there’s also evidence that the far less lucrative economics of the net-billing tariff have severely crimped ongoing prospects for California rooftop solar installers. The rate of installations under the new net-billing tariff have lagged historical rooftop solar installation rates, averaging about 8,000 per month over the first quarter of 2024. That’s a lower rate of rooftop solar installation than in any month under net metering going back to May 2020, according to LBNL’s data.

In November, the California Solar and Storage Association (CALSSA) reported that monthly solar sales — a more forward-looking data point than installations — fell by 77 to 85 percent between May and September of last year compared to the same months in 2022.

The trade group also warned that solar installers expected to have to lay off nearly 17,000 workers, or about 22 percent of the state’s rooftop solar workforce — a level of job losses “reminiscent of the Great Depression,” according to Bernadette Del Chiaro, CALSSA’s executive director.

LBNL’s report includes forward-looking data that backs up CALSSA’s dire forecasts. One such metric is “quote activity” — requests for price quotes from customers interested in installing solar.

Quote requests from online solar marketplace EnergySage spiked before April 2023, then fell to about 60 percent of historical levels from 2019 to 2021. “While the EnergySage marketplace may not perfectly represent the California market overall, the fact that quote activity has not meaningfully picked back up is perhaps the clearest signal yet of a substantial and sustained market contraction,” Barbose wrote in his report.

LBNL also highlighted data that appears to support a key concern of CALSSA — that the new net-billing regime is harming smaller solar installers. According to the report, only half of the roughly 2,500 companies that installed at least one solar system in the past 12 months have completed a system under the new tariff structure.

At the same time, the top five installers in the state increased their market share from 40 percent during the last year of net metering to 51 percent during the first year of the net-billing tariff — largely driven by expanding market share for top U.S. residential solar installer Sunrun.

“The big question mark is, how many of the existing installation companies are going to make the leap into the net-billing market?” Barbose said.

More batteries — and more expensive projects

Sunrun and other large-scale solar and battery installers are far better positioned than their smaller competitors to capitalize on a key trend — a “pretty dramatic shift we see toward higher storage attachment rates,” or the addition of home batteries to rooftop solar installations, Barbose said.

LBNL found an “attachment rate” — the percentage of solar installs that are paired with batteries — of about 60 percent for systems installed under the net-billing tariff, compared to about 10 percent for systems installed under the old net-metering tariff. Overall, residential battery installations since November have more than doubled from historical monthly averages over the past three years.

That’s an expected and desired outcome of the CPUC’s new policy, which aims to push customers and installers from solar-only to solar-plus-battery systems. The goal is to get people to store solar power generated during midday periods, when California is awash in excess solar power, and discharge it during hot summer and autumn evenings, when the state grid faces peak electricity demands and the threat of grid emergencies.

The net-billing tariff aims to accomplish this by slashing the value of solar sent back to the grid by about 75 percent on average, with only a few exceptions during late evenings in August and September when grid export compensation rates spike.

But LBNL found that the cost of solar-plus-storage systems is rising. Inflation-adjusted install prices for paired solar-battery systems climbed by about 17 percent under the net-billing tariff compared to historical costs under the old net-metering tariff, Barbose said.

LBNL hasn’t analyzed that data to tease out all the factors that may be driving the price increase, he cautioned. One working theory is that “there’s this inrush of demand for storage systems for which there’s not enough equipment or trained installers,” driving up costs for installers and thus prices for consumers.

However, there’s a broader problem with a policy that pushes customers to invest more money by adding batteries to solar systems even though those solar systems earn less money than they would have under the previous net-metering regime. While rooftop solar systems installed under the net-billing tariff are more likely to include batteries, fewer systems are being installed overall — and that means there are fewer batteries that could help serve grid needs.

CALSSA’s Del Chiaro calls this out as a troubling trend. The industry installed 22 megawatts of storage in January 2023, compared to 23 megawatts alongside a much larger amount of solar in January 2022, she told Canary Media earlier this year.

Meanwhile, the net-billing tariff alone may not provide enough incentive for owners of solar-and-battery systems to use them to help shore up the grid during times of need — or, as Barbose put it, “optimize operation of behind-the-meter storage from a grid-operational perspective.” That’s because the tariff, combined with time-of-use rates that charge more for power consumed during late afternoon and early evening periods, primarily encourages customers to store as much of their solar power as possible for their own use, not to send it back to the grid.

To get customers to start sending solar power stored in their batteries back to the grid when the grid needs it most will require “virtual power plant” structures that adequately compensate customers for that service, he said.

A few such VPP programs currently exist in California and elsewhere in the U.S., but they’re far from the norm — and unless they become more common and predictable sources of revenue, it will be hard for households and solar installers to factor their value into calculations about whether solar and batteries are a worthwhile investment.

Meanwhile, stifling a rooftop solar market that’s delivered nearly half of the state’s total solar generation capacity to date may well undermine the state’s progress on its climate goals. California’s scoping plan, the state’s official blueprint for hitting its carbon-reduction mandates, calls for 29 gigawatts of small-scale solar capacity by 2045 — nearly double the current level of about 16.6 gigawatts.

It may be unwise to rely too heavily on current market trends to predict whether California’s rooftop solar policies are positioning it to hit that target — but a growing number of energy experts worry that those policies are setting the state on the wrong course.