I’m going to cut to the chase here. Devon Energy (NYSE: DVN) is a buy, provided you share management’s view on its capital allocation policy. That’s the key to the investment decision here, so here’s an outline of everything you need to know before buying the stock.

Devon Energy’s capital allocation policy

The company’s policy is to return 70% of its free cash flow (FCF) to investors, with the remaining 30% used to reduce debt and build its cash balance. The company’s adjusted FCF in the first quarter was $623 million.

You can think of the 70%, or $436 million, in the first quarter in terms of three buckets:

-

The fixed dividend of $0.22 per share accounted for $143 million in the first quarter.

-

The variable dividend, which was only $0.13 per share in the first quarter, accounted for $82 million.

-

An ongoing share buyback program accounted for $205 million in the first quarter.

Given that the last two are discretionary, it’s clear that management is prioritizing share buybacks over the variable dividend right now. Indeed, CEO Rick Muncrief believes that the market is making that decision easy for him. According to Muncrief on the recent earnings call, “Given that the equity market is still heavily discounting valuation to the energy sector, we plan to continue to prioritize share buybacks over the variable dividend to capture the incredible value that Devon offers at these historically low valuations.”

What you have to believe to agree with this strategy

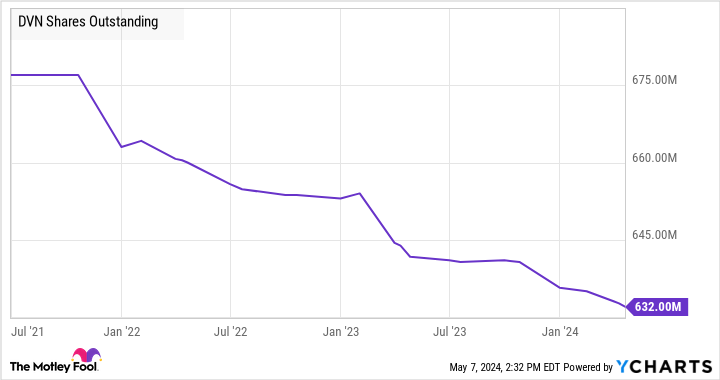

In other words, management believes the best use of shareholders’ cash is to buy back stock, increasing the share of the claim on future cash flows for existing shareholders. As the chart below shows, management has steadily reduced the outstanding shares in issue by following a share buyback program. Since the $3 billion buyback program was initiated in 2021, Devon has repurchased $2.5 billion in stock.

It’s a worthy strategy, but you should also believe a few things to support it.

First, you have to believe that the current price of oil is sustainable. If it isn’t, and the price of oil drops to around $33 a barrel as it was in 2016, buying back stock using cash flow generated at the current price of oil to increase a claim on oil only valued at $33 a barrel doesn’t make sense.

Second, you have to believe that Devon Energy will be able to increase reserves and production in the future. By using cash to make buybacks, you’re still investing in the belief that the company will produce the oil and gas to benefit from increased prices.

If you aren’t comfortable with both of these beliefs, the best use of FCF generated at the current price of oil is to return it through dividends and pay down debt.

Why Devon Energy stock is a buy for energy bulls

It’s not easy to predict the future direction of the price of oil. It suffices to argue that if you aren’t comfortable with the oil price outlook, then it makes no sense to hold the stock. Some investors may well be buying Devon under the enticement of its trailing 4.8% dividend yield and potential to pay more, given its excellent FCF generation. Still, management has made it clear that it believes buybacks are the priority at the current stock price.

As for Devon’s future production growth, the company pleased investors by raising its full-year production forecast to 655,000 barrels of oil equivalent per day (MBoe/d) to 675,000 MBoe/d from a previous estimate of 650,000 MBoe/d on the back of a successful investment in improving well productivity in its core Delaware assets. Equally impressively, the production forecast increase doesn’t imply any increase in its planned capital spending budget of $3.3 billion to $3.6 billion.

Is Devon Energy stock one to buy?

At the time of the earnings report, management estimated it was on track to generate 9% of its market cap in FCF in 2024. Buying back stock on this FCF yield is a significant investment for shareholders and makes more sense than returning it through the variable dividend. After all, investors buy into stocks expecting management to generate better returns on the money than they (investors) can.

Moreover, if you are bullish on the price of oil and gas and Devon’s ability to produce it, then Devon’s assets will be worth more in the future, so it makes sense to increase your claim on them by having the company buy back stock.

Should you invest $1,000 in Devon Energy right now?

Before you buy stock in Devon Energy, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Devon Energy wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $543,758!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of May 6, 2024

Lee Samaha has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Devon Energy Stock: Buy, Sell, or Hold? was originally published by The Motley Fool