Decarbonisation of the oil and gas sector seems something of a tautology. That the spiritual home of carbon should itself be looking to decarbonize, but this is, in fact, the case and there’s some very good reasons for it. At least on the operations and maintenance side and in the short run.

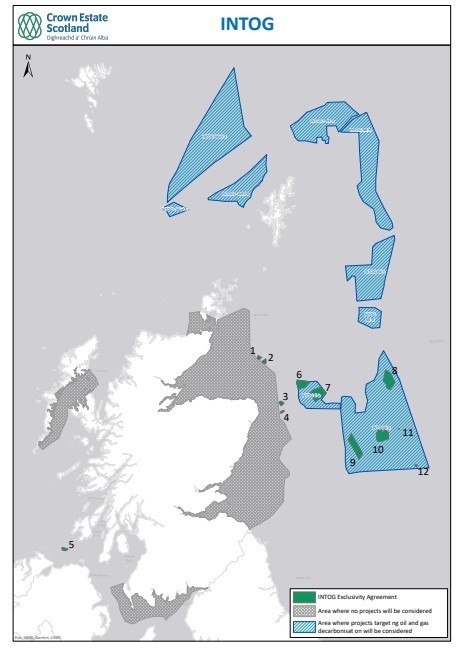

With Crown Estate Scotland updates appearing in March, the sibling Project Acorn once again in motion and leases being signed there is activity for the INTOG programme – one which have been sharing with you the community over several years.

With Crown Estate Scotland updates, the sibling Project Acorn once again in motion and leases being signed there are signs of activity on the INTOG programme which have been sharing with you the community over a number of years.

The leasing round raised £261,780,521 in Option Fees with BP, TotalEnergies and Harbour Energy being listed among the successful projects.

Proposals are split into two categories, innovation and targeted oil and gas (TOG), applicants had to meet certain criteria when applying for either of the leasing round options. The fees are literally a drop in the ocean as to what can now follow as a supply chain is fashioned from a mix of incumbents and newcomers.

There are good reasons why this is a good fit between the incumbents the oil and gas sector and perhaps the future of the energy sector in places ranging from the North Sea to the Gulf of Mexico and elsewhere.

Oil and gas majors have been making strategic acquisitions in the last decade and linking up with such outfits as floating power plant and others.

It is part of a longer-term process with oil and gas companies such as Statoil becoming Equinor, whilst Danish oil and gas or Dong now the world’s most sustainable company as Orsted.

It’s not always been a smooth ride, but in the background, of course is especially in Europe is the idea that oil and gas is not infinite as are renewables and a sector formed in the UK in 1960s and 70s must face the eye-popping costs of decommissioning which was pushed to the backburner back then.

As we’re now seeing in the Irish Sea, where methane is running out, those decommissioning factors must be faced, far better for an oil and gas company.

To turn a potential liability into an asset, especially if that can be eased, with some state funding to encourage the transition.

INTOG will ensure that at least the operations and maintenance side be decarbonized as they use diesel to power the platforms and to produce electricity for site operations. Decommissioning or re-purposing may this time mean a second life as a hydrogen generator or offshore wind base once the reservoir is expended.

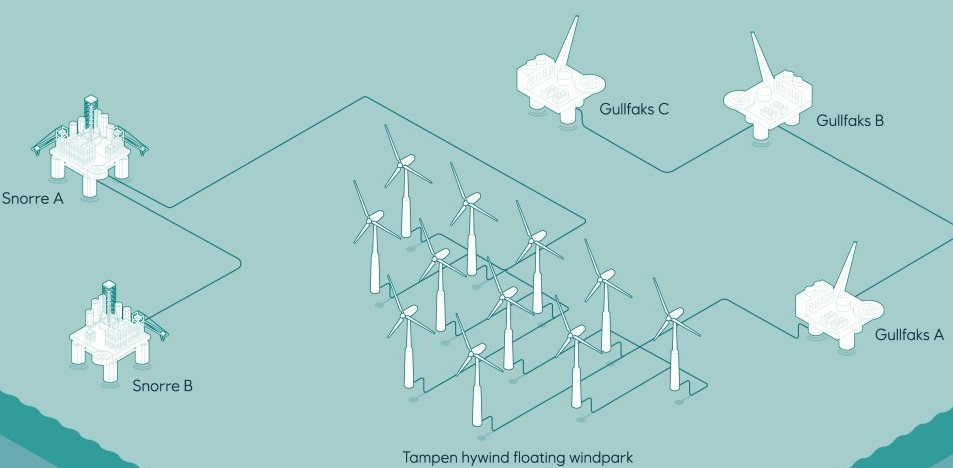

It’s already happening with Hywind and follow on oil and gas focussed Tampen cluster in the North Sea being developed by Norwegian Equinor,

The activity will encourage the floating wind sector where over a hundred models are now available but perhaps seeking a perhaps a simple Model T turbine. Wind arrays are moving into might be in deeper waters and likely 100 miles or more so from the beach.

The political backdrop has shifted and favours INTOG with energy security ramping up the agenda since Cop26 in Glasgow where opposition to the Cambo field was most evident but one of a series of oil and gas leases in similar geographical areas to Avalon and to be delivered going forwards.

If the 15 GW floating wind within the ScotWind leasing around this to be delivered, then ITOG is a necessary precursor with the merchant offtake avoiding the need for problematic electrical transmission grid infrastructure.

We can track these projects as they move forwards. All Energy in Glasgow next month offers a timely is a useful opportunity to see the shifting tectonics of the North Sea at close quarters.

Charley Rattan Associates actively supports energy companies developing their portfolios. We offer training, advisory and facilitation services. Stay informed with the moderated focus group; https://bit.ly/3rhoSWF

INTOG | Innovation and Targeted Oil and Gas

{kind=link}