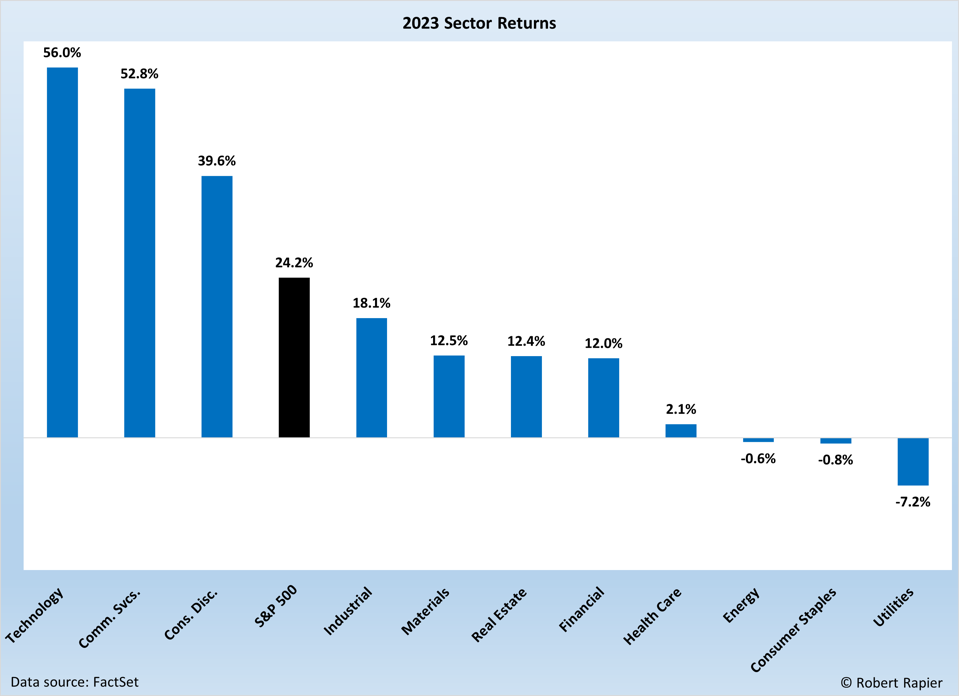

The year ended on a solid note, with most sectors notching double-digit gains in the fourth quarter. However, the energy sector, which was the top-performing sector in the third quarter, pulled back in the fourth quarter. Energy was the only negative performer in Q4, and one of only three negative performers for all of 2023.

It was a big year overall for the S&P 500, which had a total return of 24.2% in 2023. But the rally was narrow, with only three of eleven sectors beating the S&P 500. This can happen when there is a big rally in the technology sector. The S&P 500 is heavily weighted toward big technology companies. The technology sector’s 56% gain helped drive the S&P 500 performance to well above the median sector return of ~12%.

Although the energy sector was down, not all of the energy subsectors were down. According to data provider FactSet — which I use to analyze companies — the average upstream company declined 6.8% in 2023. These are the companies that produce oil and gas.

But the negative performers were primarily the smaller upstream companies. The average return of the ten largest upstream companies was +3.9%. Two Canadian companies — Canadian Natural Resources (+23.7%) and Imperial Oil (+20.6%) — each returned more than 20% for the year.

The midstream segment fared much better. Among the 43 companies that FactSet classifies as “midstream”, the average return was 31.7%. The midstream segment was led by an extraordinary 360% return by NGL Energy Partners.

The integrated supermajors were mostly higher, gaining 3.9%. Among this group, the best performer for the year was Shell with a return of 20.2%. But after huge gains in 2022, Chevron (-13.6%) and ExxonMobil (-6.3%) were both down.

The Big Three refiners — Marathon Petroleum, Valero, and Phillips 66 — also significantly outperformed the broader energy sector, gaining an average of 23.1%. Phillips 66 (+33.1%) and Marathon (+30.5%) both returned more than 30% for the year.

The energy sector performance in 2024 is going to be all about oil prices. OPEC+ supply reductions will be a driver in the oil markets this year but offsetting that is record U.S. oil production. The Biden Administration is also making purchases to replace some of the depleted reserves from the Strategic Petroleum Reserve (SPR), and that will also have a bullish impact on oil prices. But high oil prices are a prescription for losing an election, so that’s also why I think the SPR purchases this year will be limited.

Follow Robert Rapier on Twitter, LinkedIn, or Facebook

{kind=link}