Saudi Arabia and its OPEC+ allies continue to throttle crude output in an effort to support oil prices, but the U.S. — with its record-high production and growing exports — is making that task particularly difficult.

In other words, the global battle for market share is heating up again.

OPEC+ members on Nov. 30 agreed to voluntarily cut production by another 2.2 million barrels per day, or bpd, through the first quarter of 2024, a figure that included the rollover of a production cut of 1 million bpd first implemented by Saudi Arabia in July.

“As Saudi Arabia has undertaken significant production cuts in the last year, this has been reflected through in considerably lower crude exports,” Matt Smith, lead analyst, Americas, at Kpler told MarketWatch.

“On the flip side, as U.S. oil production hits a record, U.S. crude exports continue to gradually rise,” he said. “Hence, exports from the two have been converging, particularly in the last six months.”

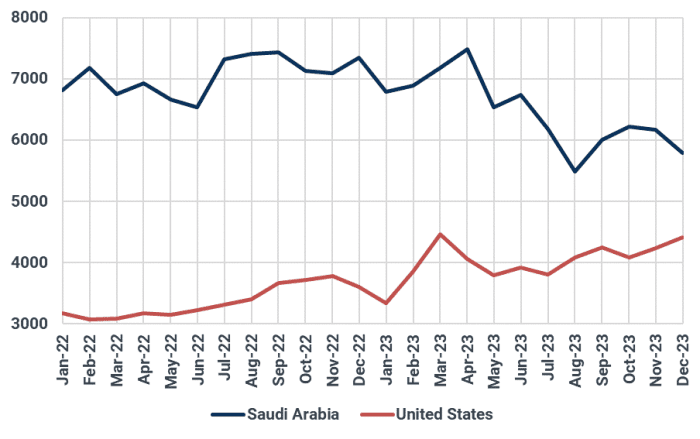

U.S. crude exports climbed to 4.5 million barrels per day in December, while Saudi Arabia’s crude exports have declined to less than 6 million bpd, according to data from Kpler.

Kpler

Back at the start of 2022, Saudi Arabia was exporting nearly 7 million bpd, which was over 3.5 million bpd more than the U.S., said Smith.

Last month, however, the gap narrowed to just 1.5 million bpd as Saudi crude exports fell below 6 million bpd and U.S. crude exports stood close to 4.5 million bpd, he said.

That comes against a backdrop of rising tensions in the Middle East that have contributed to disruptions to shipments of oil and other goods through the Red Sea. Iran-backed Houthi rebels have attacked on vessels in the waterway, leading companies to halt shipments and reroute cargo.

Read: Here’s what’s been keeping a lid on oil prices despite risks of a wider war in the Middle East

Some analysts said that the shipping disruptions in the Red Sea may have contributed to a rise in U.S. petroleum exports, as buyers look to procure cheaper oil supply from the U.S., with U.S. benchmark crude prices trading at a discount to global benchmark Brent crude.

Read: Why Red Sea chaos is driving oil buyers ‘into the arms of U.S. shale producers’

Market share may be of particular concern for Saudi Arabia and other members of OPEC+ as weekly U.S. oil exports inch closer to a record.

U.S. oil exports rose by 1.377 million bpd to 5.292 million bpd for the week ended Dec. 29, according to the Energy Information Administration.

That’s not too far from a record. Weekly U.S. crude-oil exports reached an all-time high of 5.629 million bpd in the week ended Feb. 24, 2023, based on EIA data going back to February 1991.

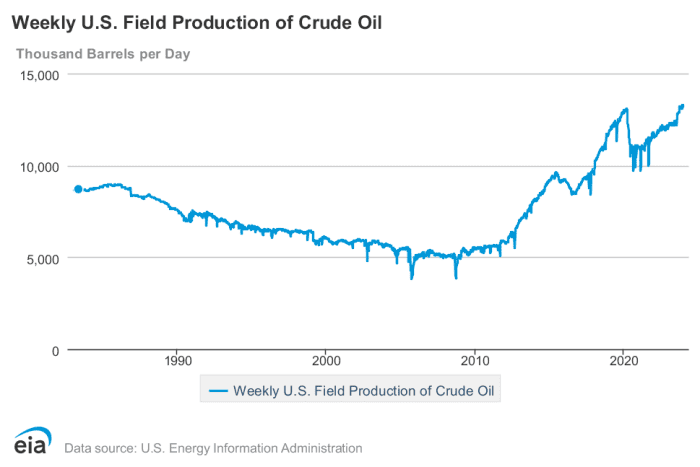

Weekly U.S. oil production, meanwhile, climbed to a fresh record of 13.3 million bpd in mid- to late-December, though it’s edged back to 13.2 million bpd as of the week ended Dec. 29.

U.S. crude-oil production marked a record high at 13.3 million barrels per day for the week ended Dec. 22, according to the EIA.

U.S. Energy Information Administration

U.S. oil production exceeded expectations in 2023 as efficiency and productivity gains surprised the market and offset some of the OPEC+ output cuts, said Rebecca Babin, senior energy trader at CIBC Private Wealth U.S. At its meeting in November, OPEC+ announced additional voluntary cuts totaling 2.2 million barrels a day to the end of March 2024.

U.S. output, however, was not the only surprise story of 2023, said Babin.

Iran, which is an OPEC member but not subject to production quotas, also materially increased output, she said. Iranian Oil Minister Javad Owji said in November that Iran’s oil production had climbed to 3.3 million bpd, up 50% since August 2021, according to SHANA, the Iranian oil ministry’s news agency.

Meanwhile, Saudi Arabia may have more than one reason behind its decision to lower prices for buyers of its oil — and one of them may be to regain some of the market share it’s lost to rivals.

On Sunday, oil giant Saudi Aramco said it would reduce the official selling price, or OSP, for its crude in February to all regions, including Asia, by as much as $2 a barrel.

The price cuts reflect softer demand in Asia, Babin said, adding that some data suggest China’s oil demand growth has been “moderating.”

These price adjustments bring Saudi prices in line with demand, she said, but they also indicate that the Saudis are “shifting policy from price stability to market share.”

OPEC+, as a group, has made other moves to strengthen its influence in the oil market. As of January, Brazil is its newest member.

Brazil’s will contribute to OPEC+’s supply growth over the next several years, Babin said — just not soon.

Brazil is not subject to quotas at this time so the near-term impact of their membership is “limited as it won’t impact production,” she said. This could be the first step in OPEC trying to get them to participate in group quotas, but “this will take a long time to develop” and likely require some infrastructure-related investments” by the Saudis in Brazil.

For now, Babin believes that oil prices in the $70 to $75 a barrel range is “comfortable for producers,” but not a range in which they will adjust investment or capital expenditure plans.

On Monday, West Texas Intermediate crude for February delivery

CLG24,

+2.49%

CL.1,

+2.49%

settled at $70.77 a barrel on the New York Mercantile Exchange, while March Brent crude

BRNH24,

+2.36%

BRN00,

+2.36%

settled at $76.12 on ICE Futures Europe.

Oil priced at $70 reflects a market that is balanced in 2024, but there are concerns that there will be modest oversupply in the first quarter of this year if OPEC members do not comply with voluntary production cuts, said Babin.