In November 2022, the refined fuels industry reclassified ozone nonattainment as severe citing the U.S. Environmental Protection Agency Clean Air Act section 211(k)(10)(D), noting, “the sale of conventional gasoline [is] prohibited in any ozone nonattainment area that is reclassified as Severe beginning one year after the effective date of the reclassification.”

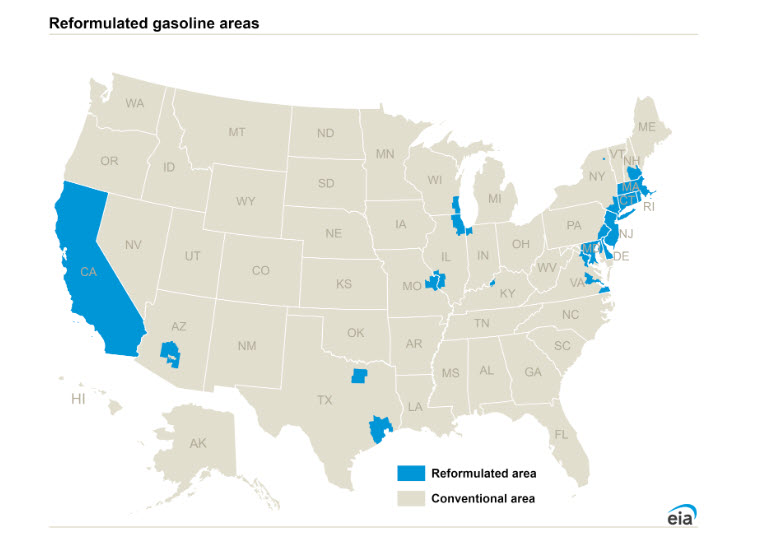

A year later, most parts of the United States have transitioned to their highest winter grade Reid vapor pressure ratings, and the remaining regions will complete the transition by December 1. Schedulers ensure they are routing gasoline with the appropriate fuel specifications on pipelines, while traders’ bid/ask price spreads adjust for the difference in fuel quality. During this season’s winter transition, the Denver area along with six additional counties around Dallas are required to sell reformulated gasoline for the first time.

“RFG is already required in four counties in the Dallas area because EPA approved a request from Texas to opt those counties into the RFG program,” said the agency, with the RFG zone now expanded to all 10 counties in the Dallas-Fort Worth area. In Colorado, Denver, Boulder, Greeley, Fort Collins, and Loveland were reclassified as severe nonattainment under the Clean Air Act. Beginning May 1, 2024, summer gasoline in these cities in Colorado will need to adhere to an RVP standard of 7.4psi at the wholesale level, and at the consumer level on June 1, 2024.

Refiners will produce the appropriate gasoline blendstock for these regions, but multiple gasoline grades despite being streamlined nationally on January 1, 2021, create different economics. RFG is used in 16 states and the District of Columbia, and roughly 25% of the gasoline sold in the United States is reformulated.

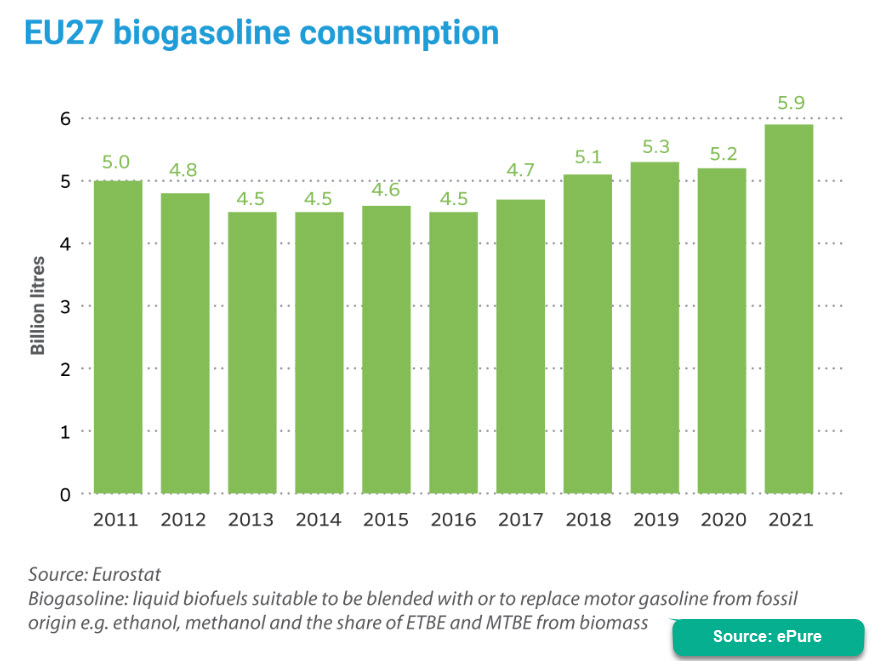

In the 27-member European Union, the number of countries adopting an E10 petrol standard has grown to 13, according to ePure, a trade organization for the European renewable ethanol industry. E10 accounts for all the gasoline supply in Bulgaria and Romania, and more than 90% in the Netherlands and Denmark. Countries with 70% or greater E10 supply include Slovakia, 87%, Belgium, 83%, Hungary, 77%, Finland 77%, and Luxembourg, 70%. Four additional countries, Lithuania, France, Estonia, and Germany, round out the count. The trade group expects the number of countries using the E10 standard will continue to grow in the EU, as they struggle to meet stiff environmental regulations such as the Renewable Energy Directive and the Fuel Quality Directive.

“The convergence between the European and U.S. gasoline markets should help to simplify trading and risk management between both markets,” said Wightman and Hui.

The increasing use of ethanol in gasoline in the EU at a 10% concentration, up from 5%, has an impact on the U.S. gasoline market in a few ways. EU gasoline specifications are increasingly aligned with the U.S. standard, with Europe’s Eurobob equivalent to RBOB. The fungibility improves the use of New York Mercantile Exchange RBOB futures and options as hedging tools for refiners and trading companies to manage risk. Thus, the RBOB contract, which can be physically delivered against authorized storage terminals in the New York Harbor, has taken on an increasing international role as a pricing benchmark.

CME Group’s Paul Wightman, senior director of Research and Product Development, and Elizabeth Hui, director of Energy Research, in June highlighted the growing use of RBOB futures by European refiners and trading houses in their paper, “RBOB Gasoline to Expand Reach from EU Green Policy Changes in Gasoline.” They found 16% of the trading volume in NYMEX RBOB futures and options during the 12-month period ending in May occurred during European hours, which is 24,800 contracts per day.

“The convergence between the European and U.S. gasoline markets should help to simplify trading and risk management between both markets,” said Wightman and Hui.

They found a strong correlation between European Eurobob non-oxy gasoline and RBOB in the United States from January 2020 to May that they indicate was about 99%.

Europe is an important supplier of gasoline along the U.S. East Coast, with total East Coast gasoline imports during the first nine months of 2023 averaging roughly 625,000 bpd, 83% of total U.S. gasoline imports, according to Energy Information Administration data. About one-third of the gasoline consumed by states along the Eastern Seaboard is produced within the region, with another third shipped by pipeline from the Gulf Coast, and increasingly, from the Midwest. Imports fill the gap.

The United States was a net exporter of gasoline during the first three quarters of 2023, with a negative 134,750 bpd net import rate, although the rate does fluctuate. U.S. gasoline exports are short haul deliveries, with more than half of the exports shipped to Mexico.

Despite the better operating efficiencies of refineries concentrated in Texas and Louisiana compared with those in the EU, such as cheaper natural gas, European refiners will continue to find favorable arbitrage opportunities in shipping gasoline to the East Coast. Gulf Coast refiners face constraints in shipping greater product volume to the East Coast, with pipeline capacity oversubscribed on the Colonial Pipeline and Products (SE) Pipe Line, commonly referred to as the Plantation Pipe Line. Waterborne transport is limited by Section 27 of the Merchant Marine Act of 1920, to tankers that are compliant with the Jones Act, pushing transportation costs higher. The Jones Act requires goods shipped between U.S. ports to be transported on ships built, owned, and operated by U.S. citizens.

In July, EU members exported 8.157 million bbl of finished gasoline and gasoline blendstock to the United States, with 78% of the exports being blendstock. The United Kingdom, which exited the EU in January 2020, exported 1.667 million bbl of blendstock and 9,000 bbl of finished gasoline in July.

Refiners produce gasoline blendstock, and the expanding use of E10 in the EU means the blendstock shipped to the U.S. market is aligned with U.S. blendstock that is more easily blended with ethanol at the terminal level. Ethanol’s increasing concentration in the EU’s gasoline pool should free up more refiner-produced gasoline that could be exported.

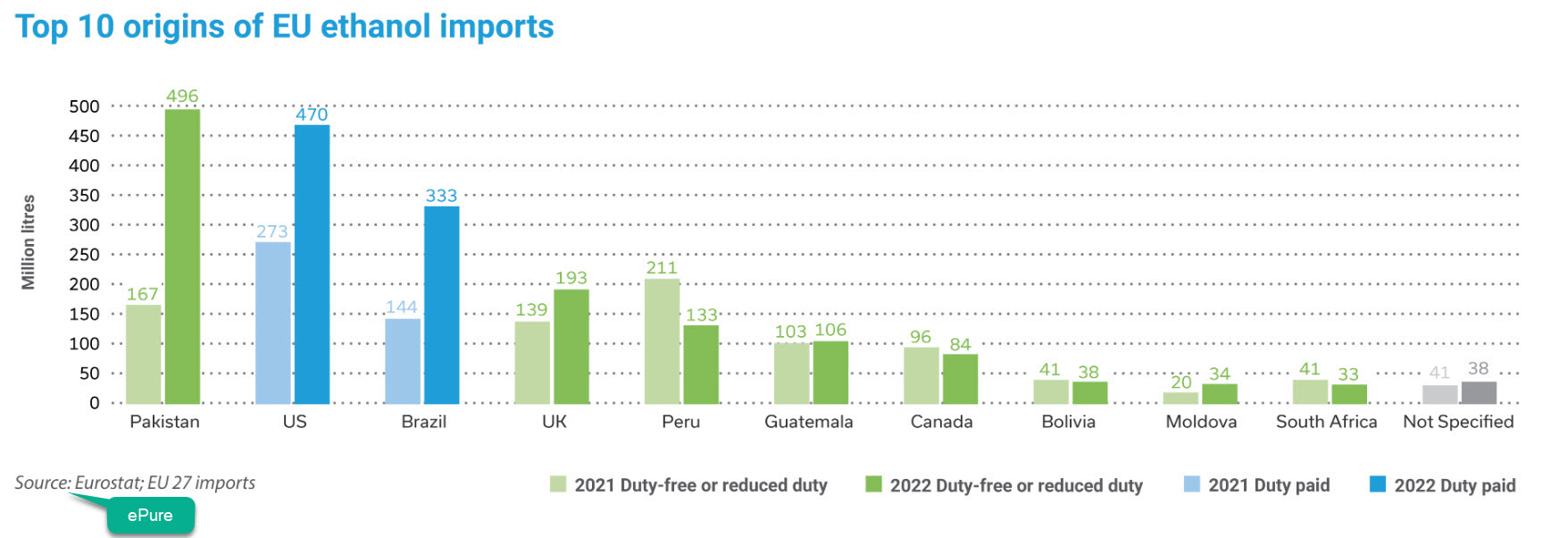

In the drive to E10, the expanded use of ethanol in the EU has drawn a bevy of ethanol imports to the continent, with the import flow overtaking some domestic producers that were forced to close operations. In response, the European Commission on Sept. 14 announced “retroactive surveillance measures” on imports of ethanol after losing market share following an 80% spike in ethanol imports between 2021 and 2022, according to ePURE.

The commission said from the fourth quarter 2021 to the third quarter 2022, the industry lost 10% of production with capacity utilization down 9%. Ethanol inventories increased by 15%, while investment is down 44% and profitability fell 15%.

“The most important exporting countries in terms of volumes in 2022 were Brazil, the United States, the United Kingdom and Peru,” said the commission. “Pakistan is the fourth most important country in terms of quantities imported, showing the highest increase of imports at 179% between 2021 and 2022. For the same period, imports from the United States increased by 96%, and from Brazil by 37%,” said the commission, adding imports from Peru fell 13%.

The commission noted the United States and Brazil produce more ethanol than consumed in their domestic markets, leaving supply for exports.

“The EU consumption is around 4.6 million tonnes and US and Brazilian producers have a combined excess capacity of 5.5 million tonnes available for export,” said the commission, adding ethanol import prices from both countries are 15% below prices in the EU, creating an attractive arbitrage incentive.

(Converting ethanol tonnes to U.S. gallons, whereas one U.S. gallon is equivalent to 0.00296 tonnes of ethanol, EU ethanol consumption in 2022 was 1.554 billion gallons, and combined excess ethanol production in the United States and Brazil equates to 1.858 billion gallons.)

The September decision by the commission “allows a close three-year monitoring of the volume of fuel ethanol imports into the Union, which will facilitate a prompt and effective reaction in case the threat related to increased imports materializes,” said ePURE.

Read more from our industry analysts.

About the author

Brian L. Milne is a 27-year veteran of the energy industry, serving in multiple roles at DTN including Editor and Analyst. Milne has delivered dozens of presentations on a wide range of topics discussing energy markets, and has been quoted widely in the media, including the Wall Street Journal, Barron’s, USA Today, Newsweek, CNN, National Public Radio, and major regional news outlets. He has authored numerous articles for international magazines, exploring market dynamics and providing forward-thinking commentary and analysis. Milne graduated Monmouth University in New Jersey with a B.A. in History and an Interdisciplinary in Political Science (Magna Cum Laude).

{kind=link}