We recently published the last in a series of five articles on mid-century ammonia (NH3) and methanol (MeOH) production costs from four primary energy inputs: solid fuels, natural gas, renewables, and nuclear. Consistent economic benchmarking, including uncertainty quantification, is done for Europe as a typical energy importer and selected exporting regions with access to cheap primary energy.

The main findings were as follows (https://lnkd.in/dTMz7C3M):

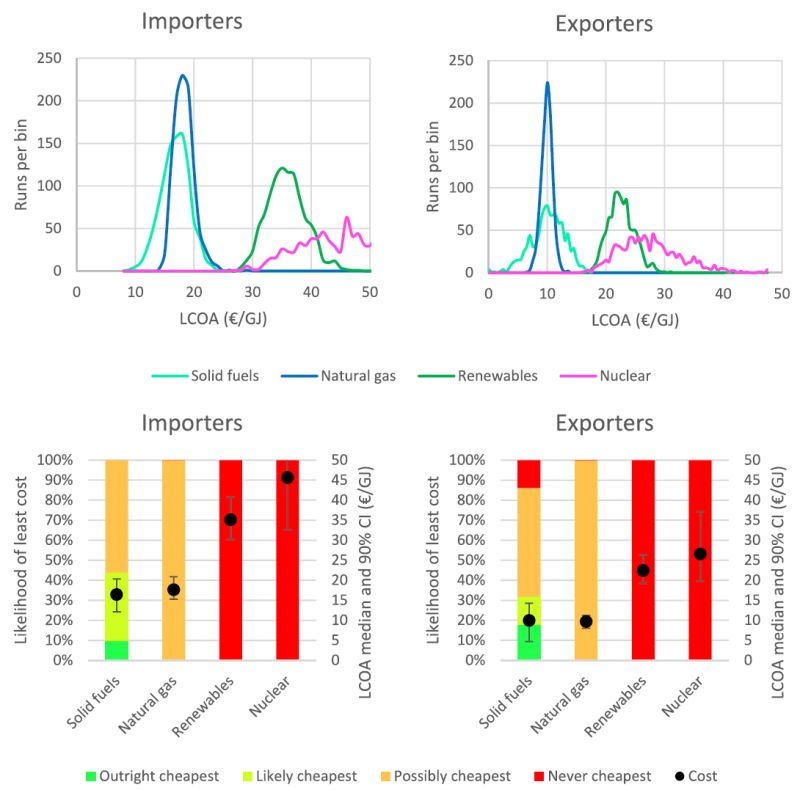

🔹 There were virtually no scenarios where electrolytic fuels (renewables or nuclear) could compete with hydrocarbon-derived fuels with CCS. Median costs for hydrocarbon-derived NH3 and MeOH are about half that of electrolytic alternatives.

🔹 Among hydrocarbon feedstocks, solid fuels (coal/biomass blends) may lead to lower NH3 and MeOH costs than natural gas if biogenic CO2 storage is rewarded with a CO2 credit. If not, natural gas is more likely to be the least-cost feedstock.

🔹 NH3 from natural gas is a promising carbon-free alternative to LNG exports, especially if the captured CO2 can be productively used for enhanced oil/gas recovery from local wells.

🔹 NH3 and MeOH are much cheaper in exporting regions than in Europe. However, some local production can still be recommended for enhanced energy security.

🔹 End-use emissions make MeOH more expensive than NH3 at relatively mild CO2 prices, but MeOH will likely retain a significant role due to its liquid state at ambient conditions.

🔹 Hybrid solid-fuel-electrolytic MeOH production presents an interesting solution for energy-importing regions with high-quality wind/solar resources and no CO2 storage potential.

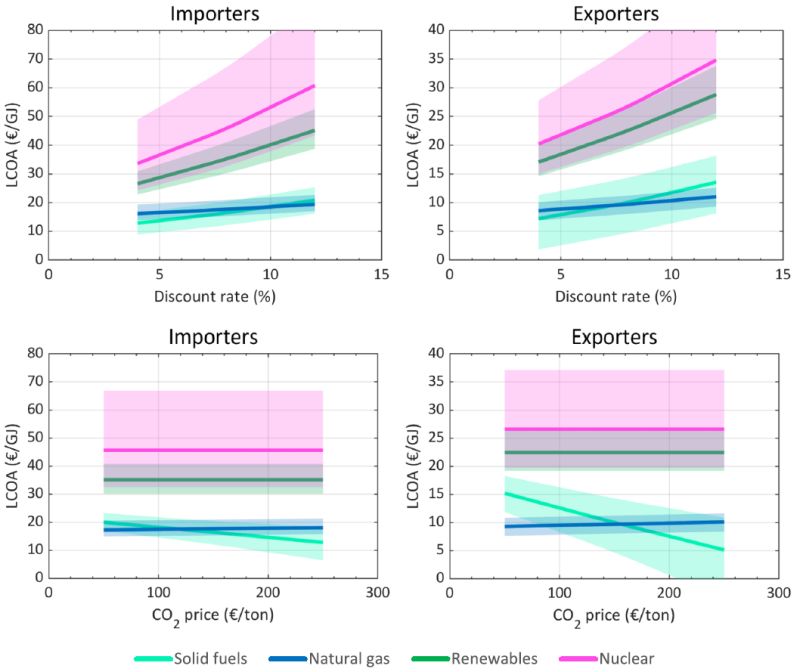

The first figure below illustrates the uncertainty distribution of the levelized cost of ammonia in importing (Europe) and exporting regions. That figure excludes uncertainties related to the discount rate and CO2 price, which are shown in the second figure (the bands are 90% confidence bounds).