Spiking oil prices can stir investor unease, but global financial markets have largely brushed off war worries, despite the tragic and growing toll of the Israel-Hamas war on human lives.

For that matter, the move in crude oil itself has been relatively muted despite day-to-day volatility, analysts said. Oil futures spiked Wednesday, rising more than 3% at their session peak to trade at their highest since the Oct. 7 Hamas attack on southern Israel. But both Brent crude

BRN00,

+2.01%,

the global benchmark, and West Texas Intermediate crude

CL00,

+2.45%

CL.1,

+2.27%

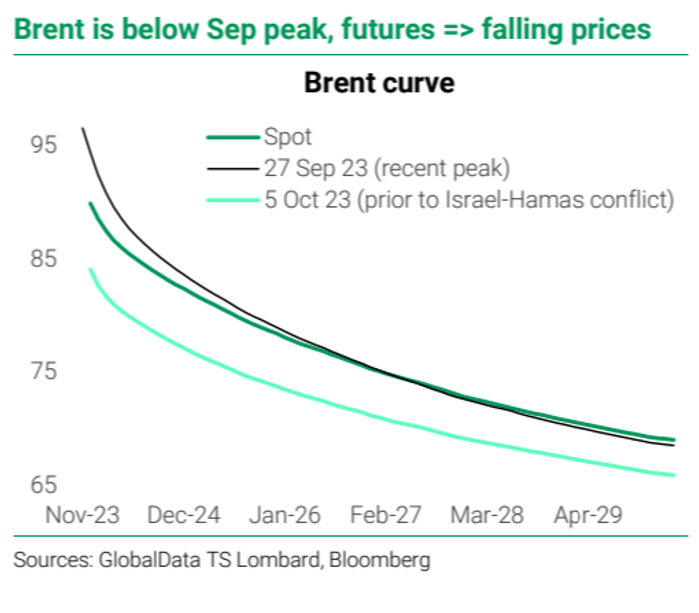

remain under their 2023 closing highs, set in late September.

And below the surface, both grades remain in what’s known as “backwardation,” meaning prices for later-dated contracts trade lower than nearer futures, indicating that traders expect prices to decline in coming months, Skylar Montgomery Koning and Andrea Ciccone of TS Lombard wrote in a Wednesday note (see chart below).

TS Lombard

While a widening conflict that involves Iran undoubtedly has the potential to push crude prices toward $100 a barrel and beyond, several factors have served to temper the rise so far.

Commodities Corner: Here’s what might lift oil prices to $95, $100 and $115 a barrel

The Organization of the Petroleum Exporting Countries, or OPEC, is estimated by the International Energy Agency to have around 4.9 million barrels a day, or mbd, of spare capacity, providing a cushion, the strategists noted. Saudi Arabia alone could, in theory, make up for any shortfall from Iran, they added.

Iranian production has crept back above 3 mbd, according to estimates, with exports recently pegged above 2 mbd.

Oil’s late September pullback came after reports Saudi Arabia and Israel were near an agreement to normalize relations, alongside a defense pact between Riyadh and Washington that would see the Saudis relax oil-production cuts. That all moved to the back burner after the Hamas attack. Indeed, a desire to derail an Israel-Saudi agreement was cited by many analysts as one potential motivation for the attack.

Regardless, Saudi Arabia knows that a surge in oil prices can be self-defeating, with elevated prices feeding into demand destruction, Koning and Ciccone noted.

That said, downside for oil is limited — and the Mideast tensions serve only to strengthen the floor beneath prices, the analysts said, supported by low reserves, an improving demand outlook and managed supply.

Beyond the oil market, the conflict underscores TS Lombard’s expectation that geopolitical “disruption” is feeding increasingly into market and economic volatility, the analysts wrote, while deglobalization, climate change, decarbonomics, strategic industrial interventions and activist fiscal policy are all also pushing in that same direction. They see early signs the market is accepting this picture, with long-term inflation expectations ticking up alongside the “term premia” — the extra yield, beyond expectations for official interest rates, that investors demand to hold debt over its maturity.

And then there are the fiscal implications of the conflict itself.

The conflict is another funding need, adding to a defense bill already enlarged by the Russia-Ukraine war, they wrote, highlighting that “once again that there is very little appetite for fiscal restraint in the U.S., meaning continued higher levels of issuance and upward pressure on yield.”