U.S. energy prices have rallied since summer, with oil futures soaring about 30% in the past three months, contributing to a pick up in headline inflation and posing a challenge for the Federal Reserve as its battles to control consumer price pressures.

The climb in oil prices, if sustained, could slow consumption and economic growth, but it will be a “manageable headwind” for the U.S. economy, according to strategists at Goldman Sachs.

“While we forecast consumption growth to slow during the fall and winter, we think higher oil prices are unlikely to cause consumer spending and GDP to decline,” said a team of Goldman’s strategists led by Jan Hatzius, chief economist and head of global investment research, in a Sunday note.

See: Oil could hit $150, sending ‘shock through system,’ says top shale CEO

Here are three key reasons why the Goldman team isn’t concerned about the surge in oil prices.

The magnitude of the oil-price increase is small

“Oil prices have risen by $20 per barrel — compared to +$40 in the first half of 2008 and +$45 in the first half of 2022 — and our forecast of retail gasoline prices using futures and wholesale markets indicates that most of the rebound has already occurred,” the strategists said.

Oil futures soared from around $70 per barrel for both the West Texas Intermediate crude

CL00,

-0.17%

CL.1,

-0.17%

and Brent crude

BRN00,

+0.11%

in late June to right below the $90-a-barrel threshold for both benchmarks in late September.

Saudi Arabia, the world’s second-largest oil supplier, has slashed production by 1 million barrels a day since July and decided this month to extend the cut through the end of the year. Russia had also moved to extend a curb on crude exports through the end of 2023.

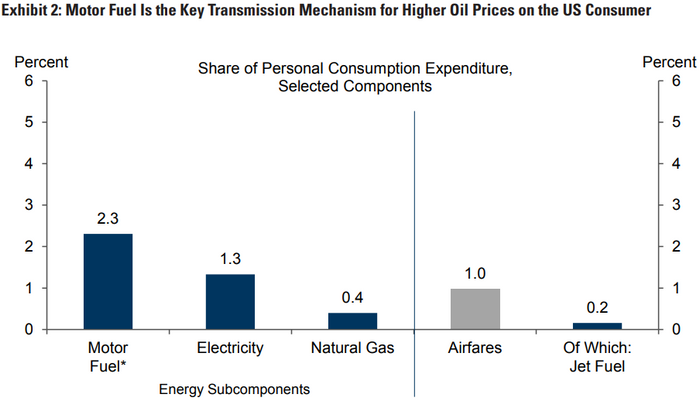

However, energy only accounted for just 4% of personal consumption expenditure in July, of which 2.3% is the cost of motor fuel (see chart below). That compares with 3.9% share for motor fuel in 2008 and 4.0-5.5% during the 1970s, said Hatzius and his team.

Moreover, while airfares represent 1% of the consumption basket of PCE, only one fifth of the cost of air travel represents crude oil, which implies a fairly marginal impact on overall consumption from higher prices in that subindustry, said strategists.

SOURCE: GOLDMAN SACHS GLOBAL INVESTMENT RESEARCH, BUREAU OF ECONOMIC ANALYSIS, DEPARTMENT OF LABOR

Higher oil prices should be partially offset by higher energy-sector CapEx, lower electricity prices

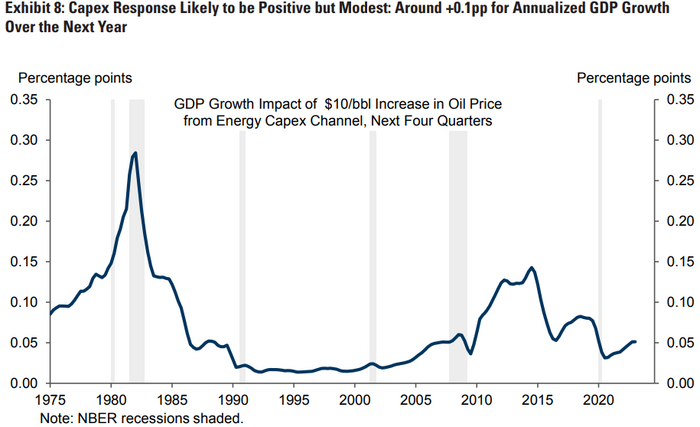

The second reason to expect the U.S. economy to continue to expand despite rising oil prices is the “offsetting positive effect” of higher energy-sector capital expenditure (CapEx) and lower electricity prices.

Higher oil prices are likely to boost corporates’ capital spending in the energy sector. Strategists at Goldman forecast a GDP growth boost from the CapEx channel of 0.1% annualized over the next four quarters (see chart below).

SOURCE: GOLDMAN SACHS GLOBAL INVESTMENT RESEARCH, BUREAU OF ECONOMIC ANALYSIS

Moreover, the year-to-date pullback in coal and natural-gas prices, as well as the end of the summer heat waves will bring electricity prices lower during the fall.

Hatzius and his team forecast a 1% pullback in consumer electricity prices between August and November, which would also boost consumer incomes and likely consumption by 0.1-0.2% in 2024, offsetting roughly one quarter of the gasoline headwind.

The Fed is unlikely to tighten monetary policy in response to higher oil prices

The Fed is another factor by which higher energy prices could weigh on the economic growth, specifically if policy makers raise interest rates to contain the inflation effects of rising oil prices, the strategists wrote on Sunday.

However, Goldman does not expect the Fed to adjust policy in response to oil prices as long as the price moves tend to be short-lived.

“The Fed should worry about the implications for price stability only if higher oil prices contribute to a de-anchoring of inflation expectations,” Hatzius and his team said. “We are relatively unconcerned about this risk and we do not expect the recent oil move to meaningfully boost consumer inflation expectations.”

See: Stock investors face a wall of worry into year’s end, creating the need for protection

Fed Chair Jerome Powell said last Wednesday that policy makers tend to look through short-term volatility and focus on how long higher oil prices are sustained.

On Monday, the West Texas Intermediate crude for November delivery

CLX23,

-0.17%

lost 35 cents, or 0.4% to settle at $89.68 per barrel on the New York Mercantile Exchange, while the November Brent crude

BRNX23,

+0.08%,

the global benchmark, gained 2 cents to end at $93.29 a barrel on ICE Futures Europe, according to Dow Jones Market Data.