Speculators have been quick to chase a breakneck rally in crude futures. Now, the U.S. benchmark may be prone to a near-term pullback, warned analysts at Société Générale on Monday.

West Texas Intermediate crude

CL00,

+1.16%,

the U.S. benchmark, closed Monday at $91.48 a barrel on the New York Mercantile Exchange, a gain of 71 cents, or 0.8%, for its highest close since Nov. 7. It’s rallied more than 37% off its 2023 closing low of $66.74 set on March 17.

November Brent crude

BRN00,

+0.26%

BRNX23,

+0.26%

rose 50 cents, or 0.5%, to close at $94.43 a barrel. It’s up more than 31% from its 2023 low.

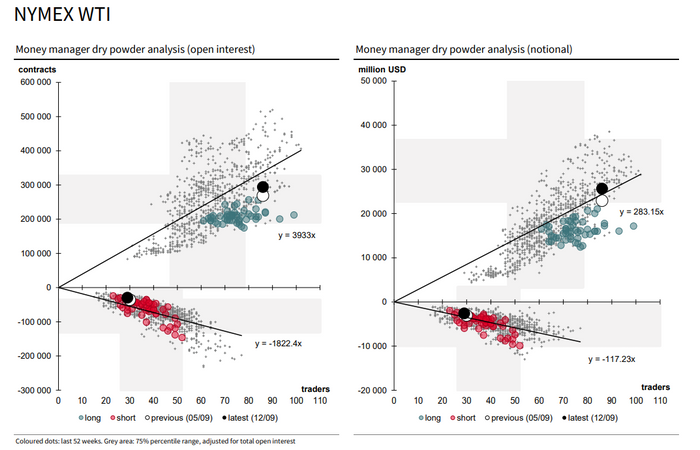

SocGen analysts, led by Benjamin Hoff, global head of commodity research, estimated that the energy complex saw a $4 billion bullish flow in the weekly period ended Sept. 12, driven by flows of $2.7 billion for WTI and $2.1 billion for Brent. Bullish flows are defined as long building plus short covering, or long building that exceeds short building, or long liquidations that’s less than short covering.

Société Générale

Money-manager long positions in WTI are now the largest since February 2022, while Brent longs are largest since this past March.

SocGen’s one-year overbought/oversold, or OBOS, model, meanwhile, remains “extremely overbought” for WTI, the analysts wrote. That means WTI futures are “extremely vulnerable” to a one-year pullback. Brent moved in the same direction, but hasn’t yet reached overbought territory due to a lack of long money-market positioning relative to total market open interest, SocGen said.

Open interest refers to the total number of open contracts.

A decision by Saudi Arabia to cut production by 1 million barrels a day beginning in July has helped boost the rally for crude, amplifying expectations for a second half supply deficit. The cut was recently extended through the end of the year, while Russia has also moved to curb supplies by 300,000 barrels a day over the same stretch.

See: Janet Yellen says she expects soaring oil prices to stabilize