August was a hot month and it wasn’t just about the weather. Financial markets are now bracing for what’s likely to be a rebound in headline U.S. inflation next week, fueled by higher energy prices.

Barclays

BARC,

+0.18%

and BofA Securities

BAC,

+0.50%

expect August’s consumer price index to reflect a 0.6% monthly rise, up from the 0.2% monthly readings seen in July and in June. In addition, they put annual CPI inflation rate at 3.6% or 3.7% for last month, which compares with the 3.2% and 3% figures reported respectively for the prior two months.

While Federal Reserve policy makers and analysts are loath to read too much into one report, August’s CPI has the potential to disrupt expectations that getting back to the central bank’s 2% target will be easy. Inflation has instead been nudging back up since June, with the likely rebound in August being regarded as primarily driven by the energy sector. What now remains to be seen is how much longer energy prices will remain elevated and whether they’ll begin to feed into narrower measures of inflation that matter most to the Fed.

Read: Stock-market investors just got reminded that the inflation fight isn’t over

“We’re going to see a spike in gas prices and other commodity prices driven by supply cuts, which means headline CPI goes back up,” said Alex Pelle, a U.S. economist for Mizuho Securities in New York.

Via phone on Friday, Pelle said that prospects for a hotter August CPI report have already been factored in by financial markets, with all three major U.S. stock indexes heading for weekly losses.

How investors react to next Wednesday’s data will likely come down to whether the rebound in headline figures is seen as “a one-off” or something that gets repeated, and “what that means for the bottoming off of inflation,” Pelle said. “The equity market is going to have some trouble in the fourth quarter after a pretty impressive first half. Earnings expectations are still pretty high, but the macro-driven backdrop is challenging.”

Rising energy prices in August have already spilled into the month of September, with gasoline reaching the highest seasonal level in more than a decade this week. Voluntary production cuts by Saudi Arabia and Russia are a major contributing factor curtailing the supply of crude oil into year-end, and Goldman Sachs has warned that oil could climb above $100 a barrel.

In financial markets, there’s one group of traders which are telegraphing that the final mile of the road toward 2% inflation won’t be smooth.

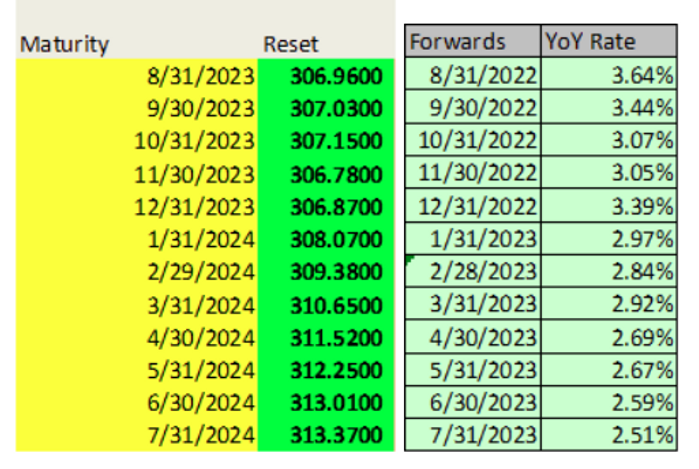

Traders of derivatives-like instruments known as fixings anticipate that the next five CPI reports, including August’s, will produce annual headline inflation rates above 3%. Though policy makers care more about core readings that strip out volatile food and energy prices, they’re aware of how much headline figures can impact the public’s expectations.

Source: Bloomberg. The maturity column reflects the month and year of upcoming CPI reports. The forwards column reflects the year-ago period from which the year-over-year rate is based.

At BofA Securities, U.S. economist Stephen Juneau said August’s CPI won’t necessarily change his firm’s view that inflation is likely to move lower next year and fall back to the Fed’s target without the need for a recession. BofA Securities expects just one more Fed rate hike in November and will maintain that view if August’s CPI report comes in as he expects, Juneau said via phone.

After stripping out volatile food and energy items, BofA Securities, along with Barclays, expects August’s core CPI readings to come in at 0.2% month-over-month — matching June and July’s levels — and to fall to 4.3% on an annual basis.

Based on core measures, August’s report wouldn’t “change the narrative all that much: Everything points to a moderation in price growth,” Pelle said. “There’s a reason why food and energy are typically excluded,” and “we don’t want to put too much stock into one month.”

As of Friday afternoon, all three major U.S. stock indexes were headed higher, with the S&P 500 attempting to snap a three-day losing streak. Dow industrials

DJIA,

the S&P 500

SPX

and Nasdaq Composite

COMP

were respectively on track for weekly losses of 0.7%, 1.2%, and 1.7%. They’re still up for the year by more than 4%, 16% and 31%.

Meanwhile, Treasury yields turned mixed on Friday as fed funds futures traders priced in a 93% chance of no action by the Fed at its next policy meeting in less than two weeks, and a more-than-50% likelihood of the same for November and December — which would leave the Fed’s main policy rate target between 5.25%-5.5%.

“There is a risk that investors are too complacent about the inflation report,” said Brian Jacobsen, chief economist at Annex Wealth Management in Elm Grove, Wis. “We might not get to 2% inflation as quickly as many hope.”