It looks like being another positive start for stocks Thursday, after the Federal Reserve’s policy decision and accompanying comments gave investors little to be worried about, and Meta Platforms

META,

+1.39%

managed to beat earnings expectations.

Hopes that the Fed’s campaign of rate hikes has helped cool inflation without cracking the economy, and thus battering company profits, sees the S&P 500

SPX,

-0.02%

in line for a fresh 15-month high.

And there’s more. The Dow Jones Industrial Average has just recorded its longest winning streak since 1987. Meanwhile, investors are so sanguine that the S&P 500 has now gone 44 days without a closing decline of 1% or more, its best such run since January 2020, according to Jonathan Krinsky, technical strategist at BTIG. Little wonder the CBOE VIX index

VIX,

-1.52%,

a gauge of expected stock market volatility, sits at just 13 or so, way off its long-run average around 20.

But, such a period of studied relaxation is exactly the time when traders should force themselves to look out for things that could damage a benign scenario.

Resurgent inflationary pressures should do it. And higher oil prices may be the catalyst.

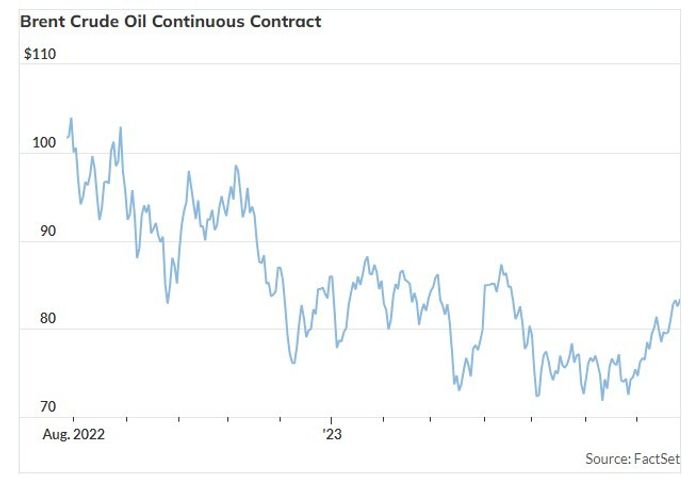

The cost of Brent crude

BRN00,

+0.59%

has climbed to a three-month high above $83 a barrel, and looks set to rally to the top of its range, says the global commodity research team at Bank of America, led by Francisco Blanch.

Brent has been stuck in a rough trading band between $70 to $90 all of the year. Factors suppressing the price are well known. Rising interest rates globally have crimped aggregate demand and curbed oil consumption, says Blanch. The narrative has encouraged speculators to maintain either neutral or short positions on oil.

In addition, China’s emergence from COVID lockdown has been weaker than hoped, while Russia has added more oil to the market than expected this year.

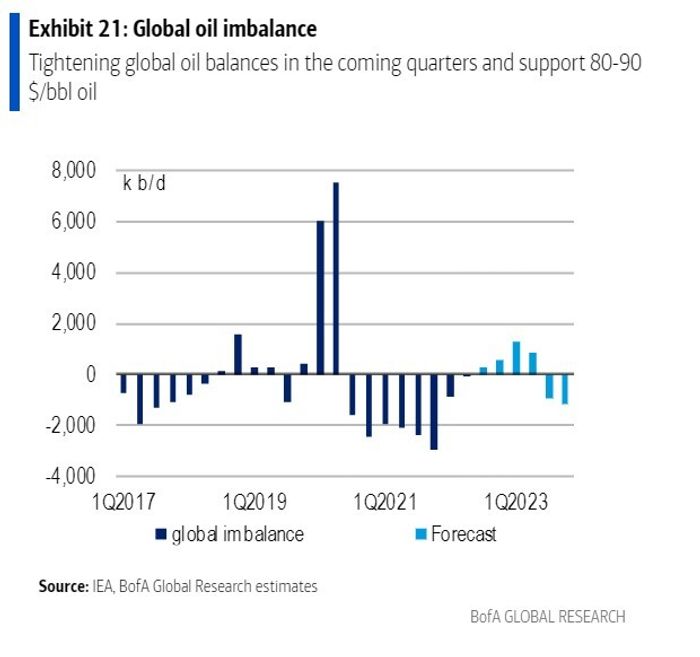

But Blanch is reiterating his $90 a barrel Brent price target by early 2024. “The stars are finally aligning for a run in crude oil prices over the coming quarters. From a fundamental perspective, our supply and demand balance projections continue to suggest that oil markets will tighten very substantially over the coming 18 months, so we expect global oil stocks to decline substantially over this period as a result,” he says.

Source: Bank of America

Driving the imbalance will be further output curbs by Opec, and lower exports by Russia as Moscow balks at the oil price cap imposed by the west. “Russia is now getting serious about reducing exports to the oil market to rein in Brent-Urals differentials,” says Blanch.

Then there’s the U.S. where the release of barrels from the strategic petroleum reserve will need to be reversed. “With U.S. oil production becoming less elastic, America has flexed its government muscle to cap global energy prices. Yet the SPR is now below 350 million barrels and needs to be refilled by to 500 or 600 million barrels.”

The fall of commodity costs in recent month has been a drag on year-on-year headline inflation measures, Blanch notes. “Yet a resurgence in energy and food prices in the months ahead, triggered by OPEC’s and Russia’s actions, could murk the macro outlook and lead to further unexpected rate hikes.”

Markets are pricing in a two-thirds possibility that interest rates will stay this year at the 5.25% to 5.5% range the Fed brought them to on Wednesday, according to data from the CME.

Markets

U.S. stock-index futures

ES00,

+0.54%

NQ00,

+1.19%

are higher as benchmark Treasury yields inch up. The dollar

DXY,

-0.23%

is lower, while oil prices rose and gold is rising.

For more market updates plus actionable trade ideas for stocks, options and crypto, subscribe to MarketDiem by Investor’s Business Daily.

The buzz

Economic data on Thursday include the weekly initial jobless claims, durable goods orders for June, and the advanced report on second quarter GDP, all due at 8:30 a.m. Eastern. Pending home sales for June will be published at 10 a.m.

The European Central Bank will deliver its monetary policy decision at 2:15 p.m. Central European Time (8:15 a.m. U.S. Eastern) with a press conference half an hour later. The ECB is expected to raise rates by 25 basis points, the ninth rise in a row, as inflation remains above 5%.

Shares in Meta Platforms

META,

+1.39%

are jumping 9% after the Facebook owner presented strong revenue growth and said its investments in AI were already reaping reward.

Going in the other direction are shares of Chipotle Mexican Grill Inc.

CMG,

-0.21%,

headed 9% lower after the fast-casual restaurant chain said inflation hit some of its most popular menu items.

Thursday’s company results include McDonald’s

MCD,

-0.21%,

Mastercard

MA,

+0.28%

and Honeywell

HON,

-0.68%

before the market opens, followed by Ford

F,

+0.66%,

Intel

INTC,

+0.76%

and Roku

ROKU,

+1.52%

after the closing bell.

Best of the web

Solar panels are three times more carbon-intensive than IPCC claims.

Stop phubbing! The 10 rules of smartphone etiquette – from the bathroom to your bed.

Netflix criticized for posting AI jobs paying up to $900,000 while writers and actors are on strike.

The chart

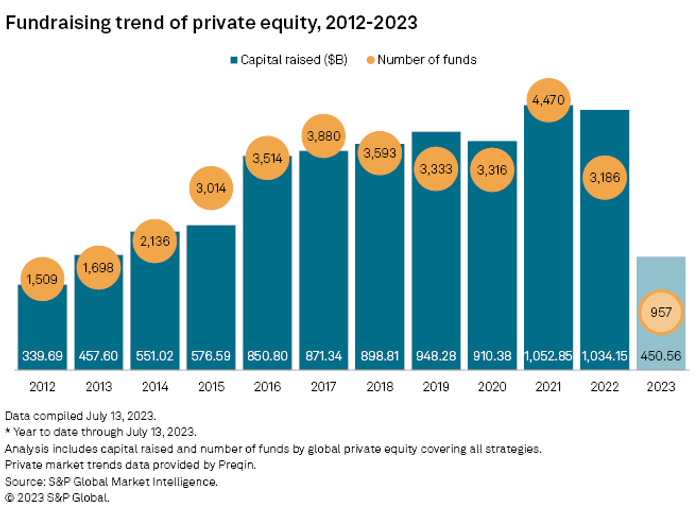

Acquisitive private equity groups can provide an underpinning to markets. So investors should note the chart below from S&P Global Market Intelligence.

“Private equity fundraising appears set to take a big step back in 2023, with both investor commitments and the number of funds in market pacing for full-year totals not seen since the middle of the last decade. Globally, private equity funds raised $444.65 billion in the first half, down 20.5% year over year from $559.02 billion in the first half of 2022,” said the S&P report.

Source: S&P Global.

Top tickers

Here were the most active stock-market tickers on MarketWatch as of 6 a.m. Eastern.

| Ticker | Security name |

|

TSLA, -0.35% |

Tesla |

|

META, +1.39% |

Meta Platforms |

|

NIO, +10.58% |

NIO |

|

AMC, -0.98% |

AMC Entertainment |

|

NVDA, -0.50% |

Nvidia |

|

GME, -0.66% |

GameStop |

|

MSFT, -3.76% |

Microsoft |

|

AAPL, +0.45% |

Apple |

|

AMZN, -0.76% |

Amazon.com |

|

MULN, +0.69% |

Mullen Automotive |

Random reads

Need to Know starts early and is updated until the opening bell, but sign up here to get it delivered once to your email box. The emailed version will be sent out at about 7:30 a.m. Eastern.

Listen to the Best New Ideas in Money podcast with MarketWatch financial columnist James Rogers and economist Stephanie Kelton