dan_prat

Back in May, I wrote an article on Gear Energy (TSX:GXE:CA) (OTCQX:GENGF), warning that its 12% dividend at the time may not be sustainable. In short, the calculations that I presented in the article indicated that in order to sustain paying CAD$0.01/month in the oil price environment at that time, management had to resort to debt. With the release of the Q2’23 results, it was announced that the August dividend will be indeed cut to CAD$0.005. However, the market environment has changed for the better during the last month as oil prices rose. The WCS spread also narrowed, although some temporary reductions in the US refining capacity may widen it again for a short period of time. Overall, Gear reported a decent quarter and the conservative stance of management, regarding the dividend, is rather a positive as it put the long-term sustainability of the business at the forefront.

Operational overview

Q1’23 key numbers (Gear Energy)

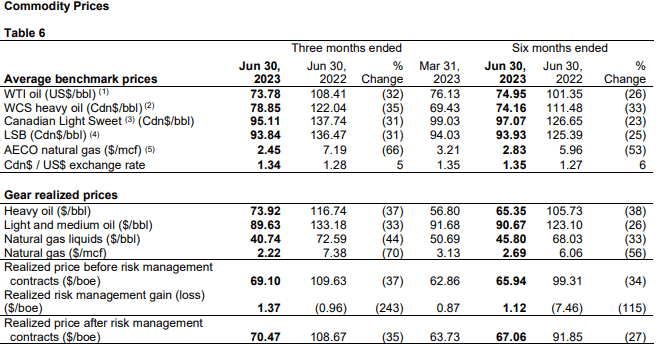

The operational environment in Q2’23 remained challenging as international oil prices continued to drop. The average price of the WTI benchmark for the quarter was US$73.78/barrel, down 3.1% QoQ and 31.9%, compared to the record Q2’22. However, this negative development was somewhat offset by shrinking of the Western Canada Select (WCS) price differential to WTI. As such, the spread fell to US$15.06/barrel in Q2’23, which is a considerable improvement, compared to US$24.76/barrel in Q1’23.

Reference and realized oil prices (Gear Energy)

As a result, the actual realized price of Gear’s production mix was CAD$69.1/boe (+9.9% QoQ; -37.0% YoY). Consequently, this was enough to compensate the QoQ drop in production (5,742/boe day; -3.5% QoQ) and Q2’23 sales amounted to CAD$36.1M (+7.2% QoQ; -37.4% YoY). Gear realized CAD$714k of gain on hedging, compared to a loss of CAD$506k a year ago.

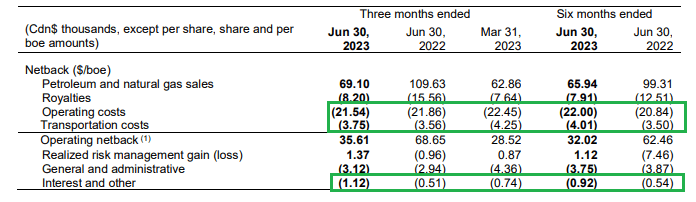

Costs (Gear Energy)

In terms of costs, despite lower production, Gear was able to achieve OPEX (Operating and transportation costs) of CAD$25.29 or 5.3% improvement on a quarterly basis. However, as expected, interest burden continued to rise. The company reported interest expense of CAD$484k (+62.4% QoQ; +130.5% YoY). The increase is due to both an increase to the level of debt (CAD21.5M as of 30 June 2023) and the interest rate. Using the Q1’23 debt level as foundation indicates that Gear is paying an annualized interest rate of approximately 9.3% on its liabilities. The bottom line for the quarter was CAD$5.6M, which equals EPS of CAD$0.02.

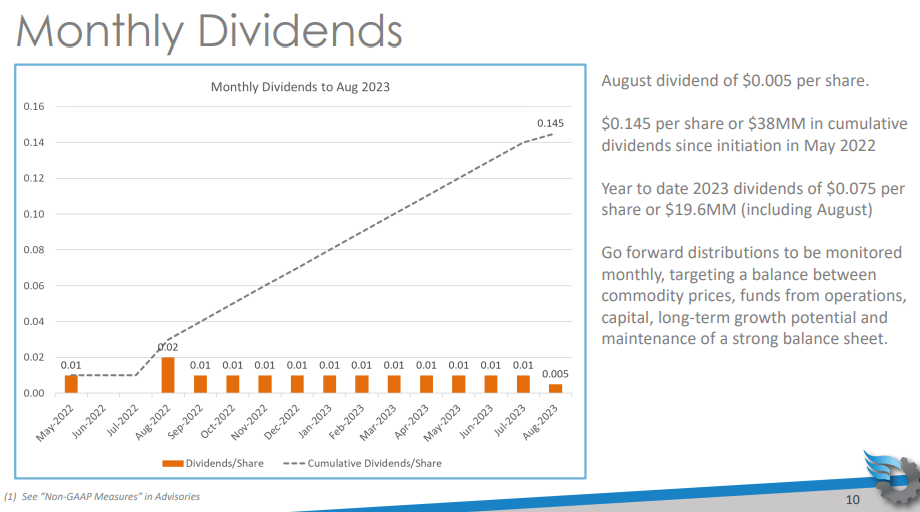

Updated guidance and dividend cut

Dividend payments (Gear Energy)

Looking at the evolution of Gear’s net debt, it increased from CAD$2.2M from 2022 year-end to CAD$14.3M as of the end of Q2’23. And this happened despite Gear spending CAD$26.7M on CAPEX, whereas the initial guidance was for CAD$58M for the full year, which would mean roughly CAD$29M for H1’23 if linear spending is assumed. Clearly, maintaining the monthly dividend of CAD$0.01/share was not sustainable, so management decided to cut it by half to CAD$0.005/share. On an annualized basis, this dividend results in roughly 6.7% yield.

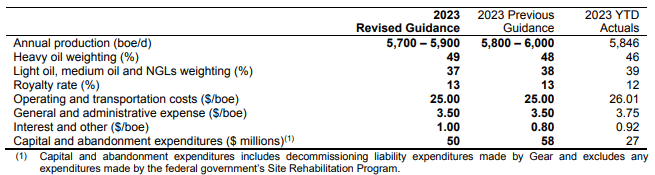

Updated guidance (Gear Energy)

Management also provided updated guidance, reflecting slightly lower production expectations and a bit higher interest expenses, but reaffirmed OPEX guidance. It’s important to note the reduction of the CAPEX budget to CAD$50M. This will allow the company to retain CAD$8M of potential cash outflow, but may have some minor effects on future production. It appears that management is trying to find the balance between capital returns, balance sheet strength and CAPEX. In light of the rising borrowing costs, I find the focus on balance sheet improvement to be prudent.

Improved outlook

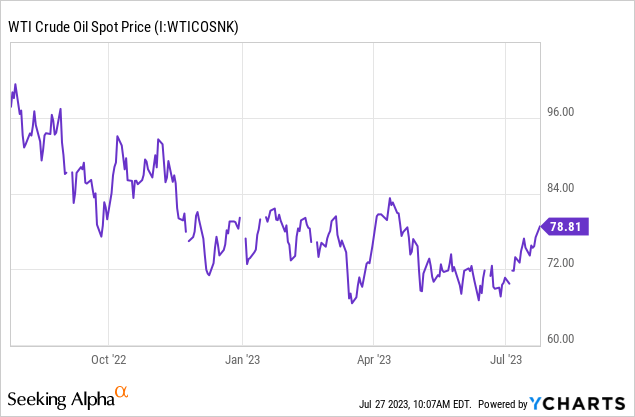

On the bright side, WTI prices have risen substantially in July so far, approaching the US$80/barrel level. This would be a big positive for Gear, especially if the WCS spread continues to narrow. Regarding the latter, the recent unexpected temporary reduction is US refining capacity may be a headwind as demand for WCS oil may fall. In light of the changed environment and the new guidance, I updated my projections for the next quarter.

| unit | ||

| production | boe | 5800 |

| WTI price | US$ | 79 |

| WCS-WTI spread | US$ | 15 |

| realized price/boe | CAD$ | 80.3 |

| Revenue | CAD$M | 42.4 |

| royalties | CAD$M | 5.5 |

| opex | CAD$M | 13.2 |

| G&A | CAD$M | 1.8 |

| interest | CAD$M | 0.4 |

| Depletion | CAD$M | 11 |

| net income | CAD$M | 10.9 |

| FCF | CAD$M | 21.4 |

| CAPEX | CAD$M | 11.7 |

| dividend | CAD$M | 3.9 |

| surplus/shortfall | CAD$M | 5.8 |

* Author’s own assumptions and calculations

Note, that the calculations assume the monthly dividend to be maintained at CAD$0.005/share, which would require approximately CAD$3.9M for the quarter. In the end, the model indicates that under the particular scenario, Gear should be able to improve its net debt situation by CAD$5.8M. Of course, if the favourable environment persists, management may decide to boost the dividend yet again. I think in a scenario where WTI is north of US$80/barrel and the WCS spread stays below US$15/barrel, a dividend increase is to be expected.

Valuation discussion

Market reaction (Seeking Alpha)

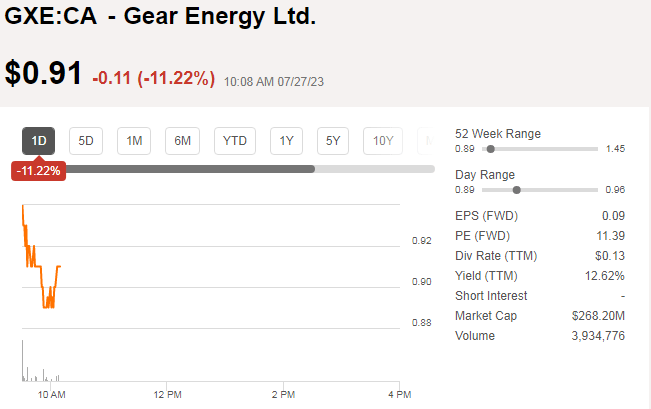

The market reaction to the Q2’23 release, including the dividend cut announcement, was not greeted warmly as shares fell double digits shortly after the market opened. This is understandable, as many income oriented investors were probably disappointed by the substantial dividend cut. My simulation of the quarterly results in the current price environment indicate that Gear should be able to generate about CAD$86M of cash on an annual basis. However, this figure doesn’t take into account any CAPEX. Using the 2023 guidance of CAD$50M as reference would leave CAD$36M as FCF, resulting in FC yield of 15%, which is quite decent. For that reason and my general bullish views on oil, I think that the current negative reaction of the market may provide an opportunity. A potential increase of the dividend could be an upside trigger.

Conclusion

Gear Energy was affected by the negative market environment in H1’23 and management decided to be conservative and cut the dividend. However, there were some positive developments in Q2’23 – the WCS spread began to narrow substantially, offsetting the lower WTI prices. However, oil has been on the up move in July, with WTI approaching US$80/barrel. My calculations indicate that such an environment would allow Gear to eventually hike its dividend. In that scenario, the share price should react favourably and erase today’s negative reaction.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

{kind=link}