okan akdeniz/iStock via Getty Images

Introduction

When last we discussed ARC Resources Ltd. (OTCPK:AETUF), Attachie was on the drawing board, but had not been sanctioned. We have passed through that gate as of the Q1 2023 report, and now it’s time to catch up again with the company. I had commented in the last article that when gas saw $2.50, ARC might rip higher.

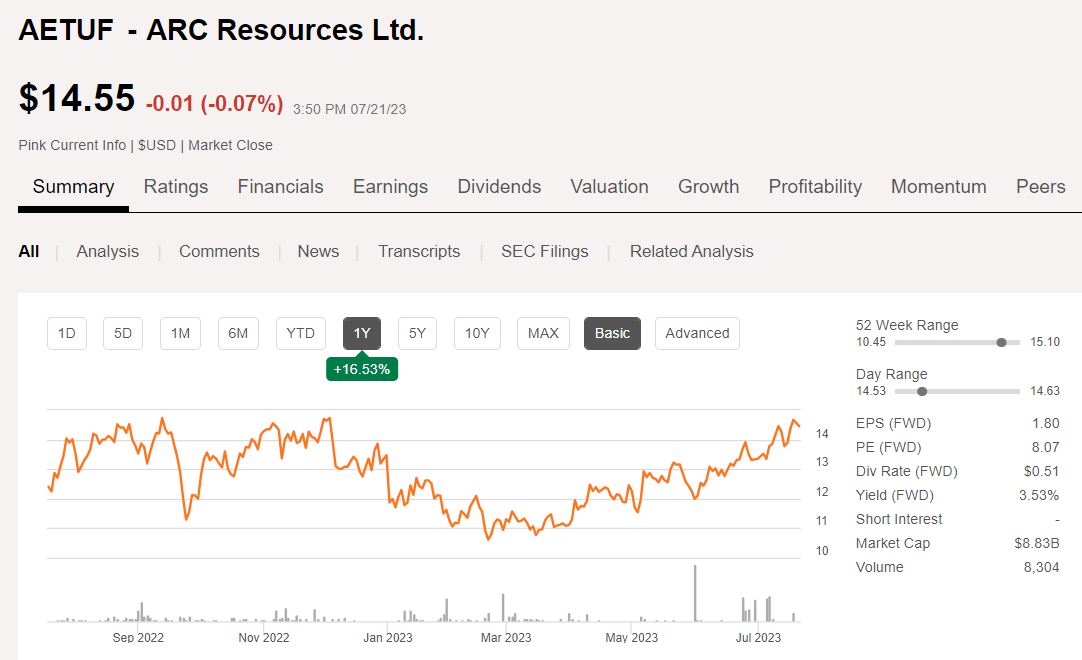

ARC Resources price chart (Seeking Alpha)

Lo and behold, I was right, as the company rocketed higher with the May rally in gas prices. Typical trading volume on ARC is about 10K shares per day. On May-31st, there was a huge capitulation of nearly 3/4 of a million shares, just as the rally began. It would be inappropriate to call this the “Smart Money,” this time around, as the stock began to immediately rally. In July, the buying activity has been fairly robust with several 300K+ share buys. Still trading in an upward channel, the stock is nearing resistance at $14.80, and if it pushes through there, could see the $18 level, set previously in June, of 2022.

In this article we will run through the Q1 2023 number and refresh our buy, sell, or hold thesis for the company. We are not going to dig too deep into the weeds here, as I’ve published on ARC several times. If you aren’t familiar with ARC, I’ve written them up several times pretty thoroughly. Please give those a read for a deeper dive than I am going to do today.

The thesis for ARC

It’s pretty simple really. As Canada’s third largest gas producer the stage is being set for export to Asia through the startup of LNG Canada, supported by the startup of the Transmountain Pipeline at the end of this year. If that isn’t enough, there are also the 42″ pipes that lead to the GoM, and the ~5.1 MPTA of liquefaction determined to keep Asia well supplied with good, clean burning North American natural gas, scheduled to come on line in 2024/5. The moon and stars are moving into a favorable alignment for ARC. And lest we forget all that wonderful ethane activity on the Texas/Louisiana Gulf Coast, it should be noted that the condensate thesis for ARC is alive and well.

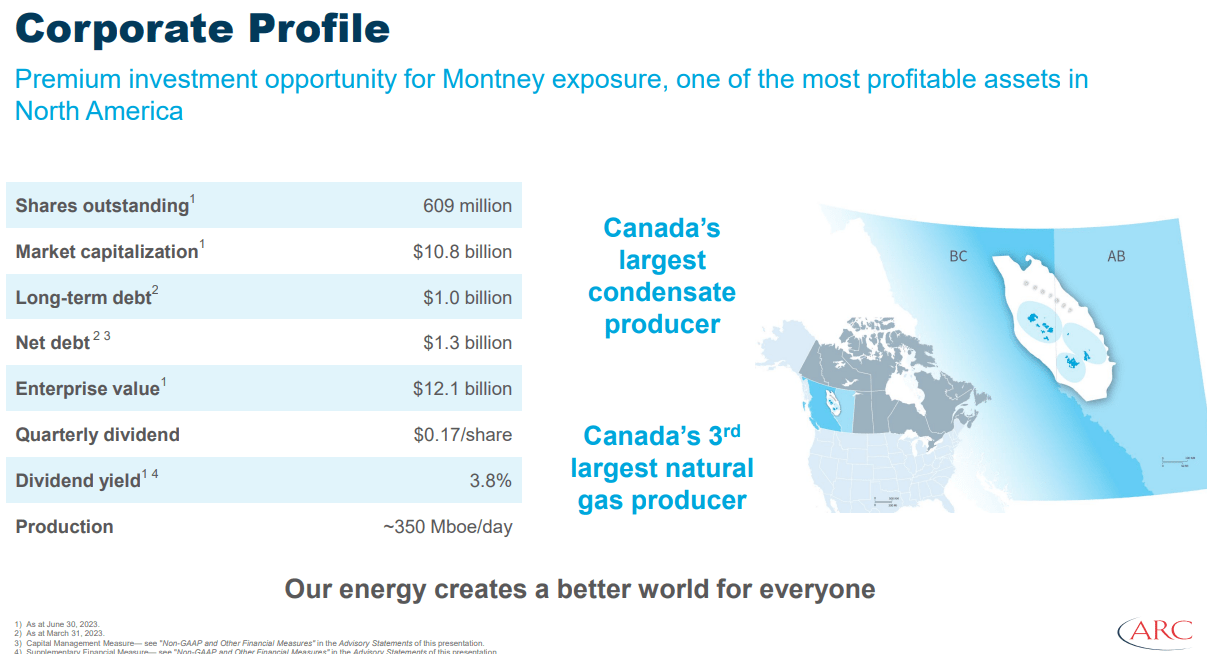

ARC Corporate Profile (ARC Resources)

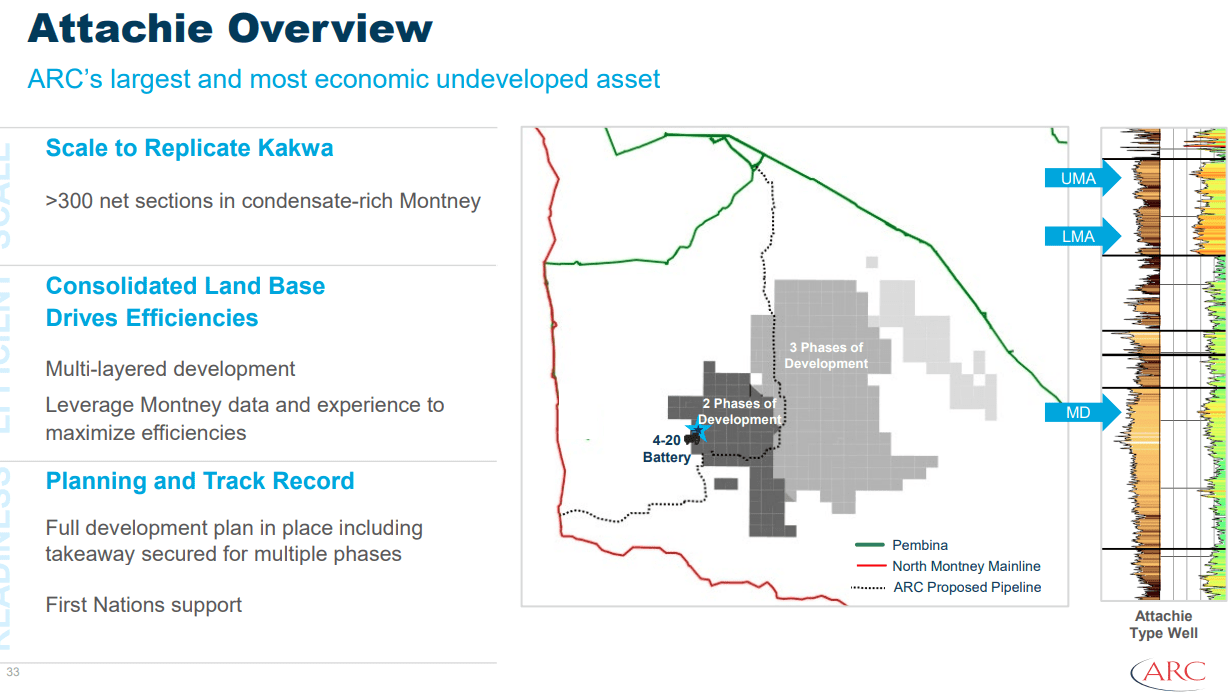

Attachie: A 2025 catalyst for shares

Attachie was always going to be sanctioned. The SP log below shows a thick column of gas-rich strata (green), and just above (as nature intends) a very contiguous column of condensate. Attachie is slated for pad-style frac development in as many as 5-separate phases, Phase-1 is set to kick off. With an estimated 5,000 drill sites across all phases, Attachie will keep ARC busy for decades.

Attachie Overview (ARC Resources)

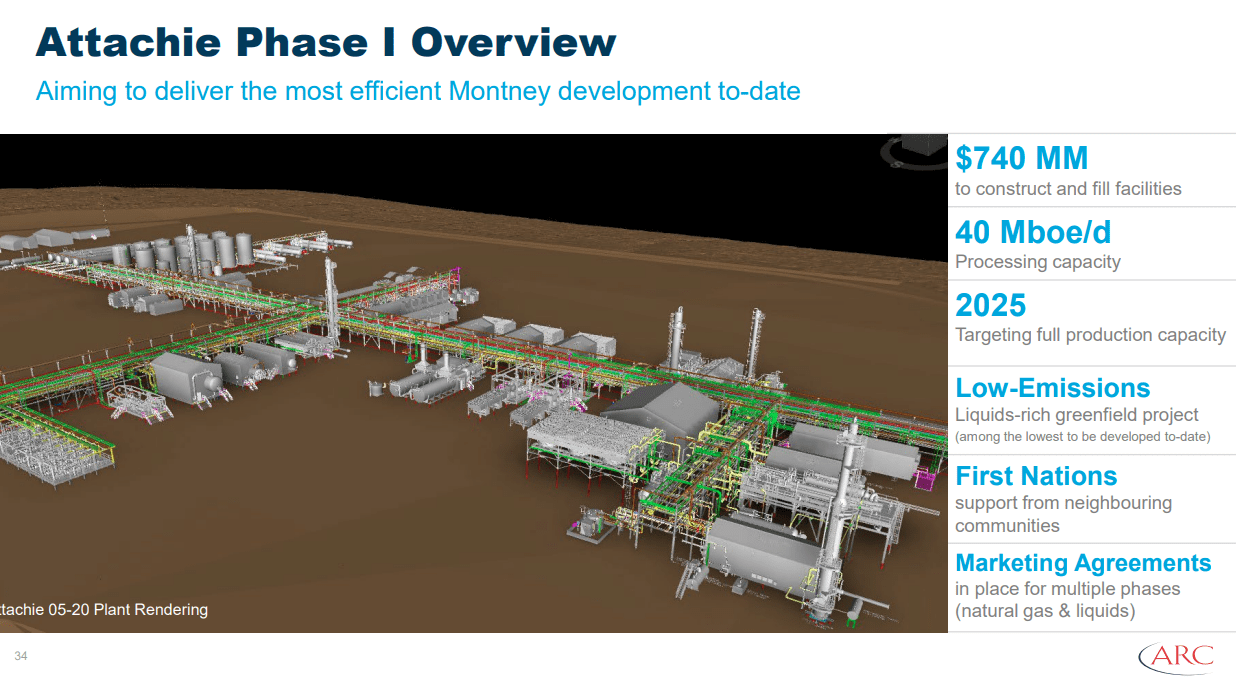

All the key elements appear to be in place for Attachie. $740 mm equates to $18K per flowing barrel equivalent, ensuring a rapid payout of capital costs. First Nations support means no court injunctions or delays constructing facilities and gathering lines, except what Ottawa may bring. Never count the government out.

Attachie Phase I overview (ARC Resources)

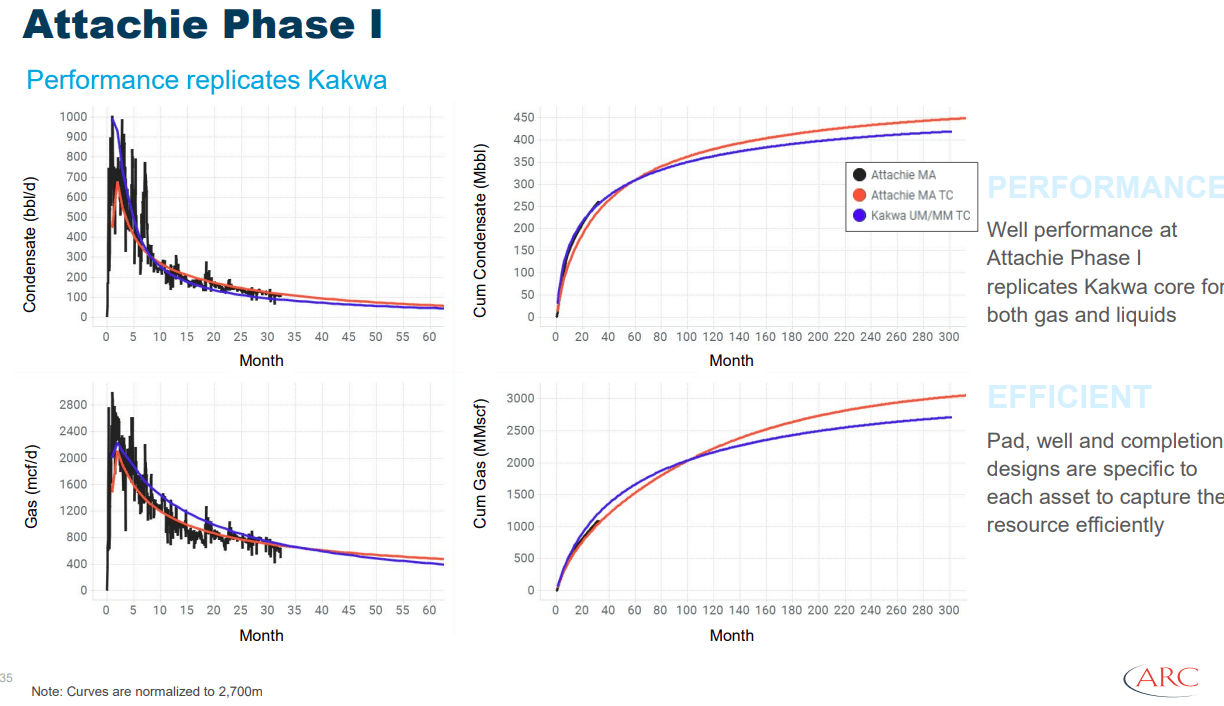

Prior to Attachie, Kakwa was and still is ARC’s top money maker. The connectedness of the reservoirs makes the pads efficient for multi-lateral completions that save time and money. Efficient completions mean that the company can still be drawing significant revenues at the 60 months, but perhaps soon reaching the balance point for water intrusion. 60 months is pretty good for a fracked completion, as compared to U.S. shale. At 600 BOPD average for condensate and 2-MCF/D average for the gas, these wells are paying out at the 6-month level, suggesting at least 5-6 multiples of the initial investment. Again, not too bad.

Attachie performance curves (ARC Resources)

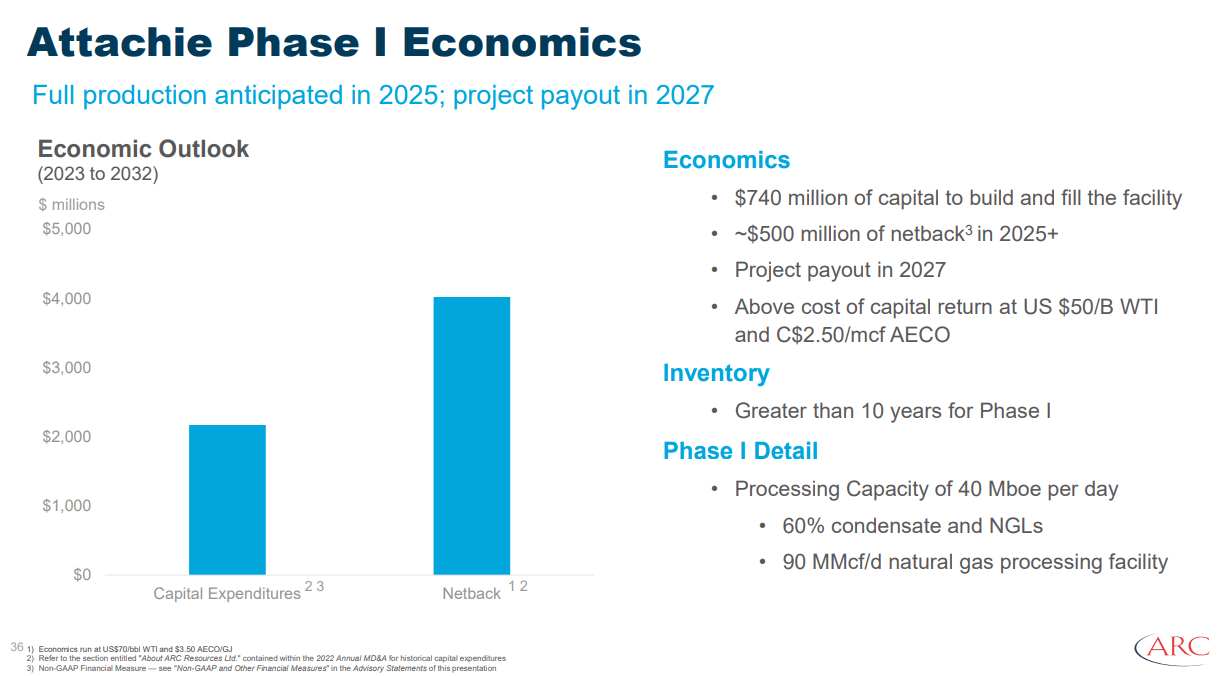

The economics that ARC projects below track pretty well with my estimates above, meaning once payout is achieved the stage is set for enhanced returns of capital. Sustaining capex is estimated at $150 mm per year for 2027 and beyond. In 2025, the company expects Attachie to contribute $450 mm AFFO, essentially doubling AFFO from the current quarter. We will keep those figures in mind for our takeaway section.

Attachie economics (ARC Resources)

Q1 2023 and full year guidance

First quarter production averaged 338,377 boe per day (62 per cent natural gas and 38 per cent crude oil and liquids). Strong base production more than offset the previously announced unplanned third-party downtime. The total impact from the unplanned third-party outages was approximately 7,000 boe per day in the quarter with production fully restored in late February. Kakwa delivered first quarter 2023 average production of 181,867 boe per day. Since acquiring the asset in 2021, Kakwa has contributed $3.7 billion to ARC’s free funds flow.

First quarter 2023 funds from operations were $717 million ($1.16 per share), representing a decrease of $269 million from the fourth quarter of 2022. This decrease was primarily driven by lower production and lower commodity prices. Partially offsetting these items were as follows:

G&A expense of $35 million ($0.06 per share) decreased by 38 per cent or $21 million from the fourth quarter of 2022 and was in-line with guidance. The decrease in G&A expense quarter over quarter primarily reflects the decrease in the fair value of share-based compensation liabilities.

Realized losses on risk management contracts of $151 million decreased $128 million from the fourth quarter of 2022. ARC has approximately 25 per cent of its natural gas hedged in 2023, primarily through collars and weighted to the summer months.

First quarter 2023 cash flow from operating activities was $540 million.

Free Funds Flow & Shareholder Returns

ARC generated free funds flow of $230 million ($0.37 per share) during the first quarter of 2023.

ARC distributed 106 per cent or $243 million ($0.39 per share) of free funds flow to shareholders through a combination of dividends and share repurchases under its NCIB.

With net debt approaching the bottom end of ARC’s debt targets, ARC intends to return essentially all free funds flow to shareholders in 2023.

Dividends

During the first quarter 2023, ARC declared dividends of $92 million ($0.15 per share). The Board approved a 13 per cent increase to the quarterly dividend, from $0.15 per share to $0.17 per share. The dividend increase is effective with the second quarter dividend payable on July 17, 2023 to shareholders of record on June 30, 2023.

Share Repurchases

During the first quarter of 2023, ARC repurchased 10 million common shares under its NCIB at a weighted average price of $15.51 per share. ARC has repurchased 44 million common shares since renewing its NCIB on September 1, 2022, representing 67 per cent of its current NCIB allotment. ARC has repurchased approximately 16 per cent of total outstanding shares, or 116 million common shares, at a weighted average price of $15.54 per share.

Full year guidance 2023

ARC intends to invest between $1.8 billion and $1.9 billion in capital expenditures (previously $1.8 billion). The company plans to invest $250 million to $300 million at Attachie Phase I in 2023. The majority of the Attachie Phase I investment in 2023 will be allocated towards long-lead items and infrastructure construction. Revised guidance includes approximately $70 million of capital inflation that has been realized year-to-date.

Offsetting the investment for Attachie Phase I is lower capital investment required to sustain base production due to stronger than forecast well performance, and the removal of approximately $120 million of capital previously allocated for water infrastructure at Kakwa. In its place, ARC has secured a long-term agreement with a third-party for water infrastructure and disposal at competitive terms. The agreement is expected to decrease associated operating costs by between $30 million and $60 million per year beginning in 2024.

Other guidance revisions include a three per cent decrease to operating costs per boe, and slight revisions to the production mix to reflect a higher natural gas weight as a result of the third-party downtime in the first quarter, and updated timing of new well pads at Kakwa. All other expenses are unchanged.

ARC’s 2023 preliminary annual guidance, 2023 revised annual production guidance, is 350-355K BOEPD, with LOE, OPEX and Transportation cost of ~$13.00/bbl.

Risks

My main concern for ARC is that its core assumptions regarding West Coast LNG sales and the Transmountain Pipeline become a reality. As long as those meet company targets, I don’t see a lot of downside risk to ARC shares.

Your takeaway

13 of 17 analysts covering the company rank it as a buy. Price targets range from about $12 USD-$18.00 USD, with a median of about $15, or where it is essentially now. In USD it is trading at 2.4X EV/EBITDA and $25K per flowing barrel using EOY estimates, so I am not sure why the analysts are so timid.

I think ARC is still in the buy zone at current levels and could rally hard if gas fundamentals improve anytime soon. I noted a while back that I think gas has bottomed for this cycle, and we should see supplies tighten in late summer.

As noted, Attachie, Phase I is near term catalyst with another $450 mm of AFFO hitting the books in 2025. That’s not that far away. If we turn that into EBITDA it’s probably another $650 mm annually, putting the total in the $4.2-4.5 bn range. To keep that multiple the same at 2.4X, the share price should go toward $20 USD, representing a 30% uplift. If gas prices improve multiple expansion could see the into the mid $20’s USD. In short, the Smart Money could be diving back into this one.

In short, I think ARC Resources Ltd. stock remains a buy for growth and increasing income from share buybacks and increasing dividend. Investors may want to monitor ARC closely for an entry point or incremental share purchase near current levels.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

{kind=link}