arsenisspyros

As I have mentioned in numerous previous articles and blog posts, one of the biggest problems facing the average American today is the incredibly high rate of inflation that has been dominating the economy over the past two years or so. In fact, earlier today, I pointed out that consumers appear to be getting increasingly stressed and are nearly at their breaking points. We can see the root cause of this problem by looking at the core consumer price index, which measures the cost of a basket of goods that is regularly purchased by the average person. As we can see, this index has increased by far more than the 2% annual rate that is considered healthy during each of the past twelve months:

Trading Economics

The above figures differ somewhat from the officially-reported figures because they specifically exclude food and energy from the calculations. Most of the “progress” against inflation that politicians are taking credit for is simply due to the fact that energy prices are much lower now than they were at this time last year. This is something that could very easily reverse itself, and indeed there are reasons to believe that crude oil could be at $100 per barrel by the end of the year. Due to this volatility, it is best to leave energy prices out of the equation when determining the actual impact of rising prices that consumers are seeing. Wages have generally not kept with the pace at which prices are rising, so most people have been getting progressively poorer in terms of what they can actually purchase over the past two years. This means that they are having more and more difficulty maintaining the standard of living to which they are accustomed.

As investors, we are certainly not immune to this. After all, we need to purchase things just like everyone else. Fortunately, we do not need to resort to some of the extremes that some people have started engaging in recently. This is because we have the ability to put our money to work for us earning an income. One of the best ways to do this is to purchase shares of a closed-end fund aka CEF that specializes in providing its investors with a high level of income. These funds are unfortunately not particularly well-covered in the financial media and many investment advisors are unfamiliar with them, which makes it difficult to obtain the information that we would like to have to make an informed investment decision. This is a shame because these funds offer a number of advantages over familiar open-ended and exchange-traded funds. In particular, a closed-end fund has the ability to employ a variety of strategies that boost its yield beyond that of any of the underlying assets or indeed just about anything else in the market.

In this article, we will discuss the AllianceBernstein Global High Income Fund (NYSE:AWF), which is one fund that investors can use to earn a very high level of income. This is evidenced by the fund’s impressive 7.94% current yield, which makes this one of the few assets available today that beats the yield of an ordinary money market fund. I have discussed this fund in the past, but several months have passed since that time so a great many things have changed. This article will focus specifically on those changes as well as provide an updated analysis of the fund’s finances. Let us investigate and see if this fund could be a good addition to your portfolio today.

About The Fund

According to the fund’s webpage, the AllianceBernstein Global High Income Fund has the objective of providing its investors with a high level of current income. This is not an especially surprising objective, considering that this is a fixed-income fund. The fund’s webpage describes its strategy thusly,

A globally diversified portfolio that takes full advantage of our best research ideas by pursuing high-income opportunities across all fixed-income sectors.

[The fund] invests primarily (and without limit) in corporate debt securities from US and non-US issuers, as well as government bonds from both developing and developed countries, including the US.

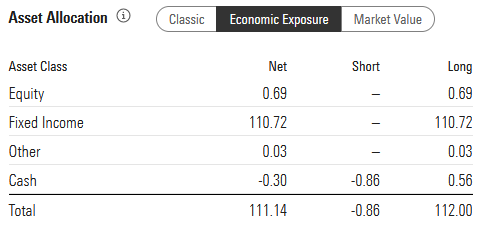

The fund is as good as its word here, as its portfolio is almost entirely invested in fixed-income securities:

Morningstar

We do see a small allocation to common equities and other things, but it is such a small allocation that it can be safely ignored. This is, for all intents and purposes, a fixed-income fund. This is why the fund’s objective of generating a high level of current income makes sense. A bond investor purchases a bond at its face value when it is issued, receives a stream of coupon payments from the bond issuers, and then receives the face value back when it is returned. Thus, the only investment return that the bond delivers over its lifetime is the coupon payment that serves as income for the bondholder. A bond has no net capital gains over its lifetime because it has no inherent link to the growth and prosperity of the issuing entity. Due to this simple fact, pretty much any fixed-income fund will have the generation of current income as its primary investment goal.

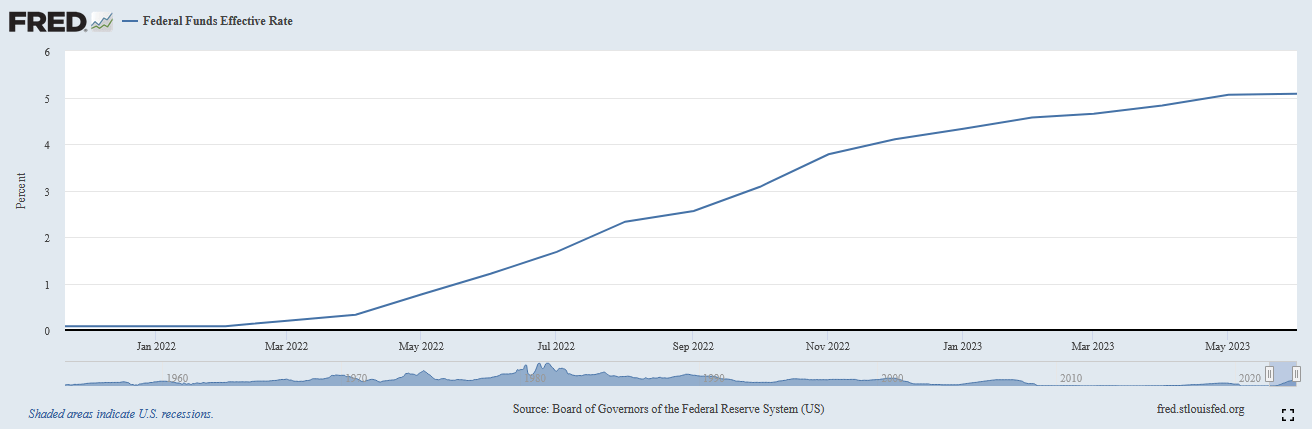

Although bonds have no net capital gains over their lifetime, it is possible for a fund to obtain capital gains by trading bonds prior to maturity. This comes from the fact that bond prices vary with interest rates. It is an inverse relationship, so when interest rates go up, bond prices go down. The reverse is also true. This is driven by the fact that a newly-issued bond will carry a coupon interest rate that corresponds to the interest rate in the market. Thus, during a period of rising rates, a newly-issued bond will almost certainly have a higher coupon rate than an existing bond. In such a situation, nobody will buy the existing bond so its price has to decline to the point that it delivers a similar yield-to-maturity as a brand-new bond with identical characteristics. As everyone reading this is no doubt well aware, the Federal Reserve has been very aggressive about raising interest rates in the United States as part of its efforts to combat inflation. In February 2022, the effective federal funds rate was 0.08% but today it is 5.08%:

Federal Reserve Bank of St. Louis

This has had a devastating effect on the prices of American bond issues. In 2022, the Bloomberg U.S. Aggregate Bond Index (AGG) delivered a -13.01% total return and a -0.94% total return over the past twelve months.

While this bond price decline would have an effect on the AllianceBernstein Global High Income Fund, it is important to keep in mind that it is not invested exclusively in American bonds. In fact, only 71.72% of the fund’s assets are invested in bonds issued by American entities:

AllianceBernstein

As such, the interest rate policies of other nations would impact this fund. This is important because the Federal Reserve has been somewhat more aggressive about raising its benchmark interest rate than the central banks of most other developed nations. However, as of right now, the only two countries in the Group of 20 that have not raised their benchmark interest rate over the past year are Japan and China. Japan is widely expected to raise its rate in the near future, however. This is because the high inflation problem is not limited to the United States, but has been a global phenomenon. As such, bonds issued by entities in just about every major country will suffer adverse interest rate effects right now. The fact that this fund can move its holdings from country to country provides it with some advantages over American-only funds though since some bonds will perform better than others at certain times. The fund also is not required to hedge its currency exposure, so it can take advantage of the fact that most major currencies have been appreciating against the U.S. dollar so far this year.

This ability to diversify globally and take advantage of fluctuations in bond prices has allowed the AllianceBernstein Global High Income Fund to deliver fairly strong performance for a bond fund. In fact, the fund delivered a 10.67% total return during the twelve-month period that ended on June 30:

AllianceBernstein

The 5.77% total return year-to-date is also reasonably impressive. In both cases, it beat the Bloomberg U.S. Aggregate Bond Index by quite a lot as that index returned 2.09% year-to-date and -0.94% over the twelve-month period that ended on the same date. This shows the skill of the fund’s management team and the advantages of being able to invest in non-US bonds. With that said, it is important to remember that past performance is no guarantee of future results but it still provides reasons to be confident in the fund’s management.

In previous articles on closed-end bond funds, I have noted that many of these funds invest in speculative-grade bonds. These are what are colloquially known as “junk bonds,” and this fund is no exception to this. We can see this by looking at the credit ratings that have been assigned to the bonds in the fund’s portfolio:

AllianceBernstein

An investment-grade bond is anything rated BBB or higher. As we can see, that is only 23.83% of the fund. With the exception of the 0.80% allocation to short-term investments, the rest of the fund’s assets are invested in junk debt securities. That obviously constitutes the overwhelming majority of the fund’s holdings. This is something that may be concerning to those investors that are worried about the preservation of principal. After all, we have all heard about the high default risk carried by junk debt securities. However, one thing that we see here is that 64.39% of the bonds in the fund are rated either BB or B. These are the two highest-possible ratings of junk bonds. According to the official bond rating scale, securities with these ratings are issued by companies that have sufficient financial strength to meet their current obligations even in the event of a short-term economic shock. Thus, these securities should have a very low risk of loss due to default.

When we consider that there are 1,393 bonds in the fund’s portfolio as of the time of writing, we can see that the actual risk of default-related losses that an investor is exposed to should be quite minimal. Overall, the biggest risk here is interest-rate risk and even that is partially hedged due to the fund’s ability to invest in foreign securities.

Leverage

In the introduction to this article, I stated that closed-end funds such as the AllianceBernstein Global High Income Fund have the ability to employ certain strategies that allow them to boost their effective yields beyond that of any of the underlying assets. One of these strategies is the use of leverage. In short, the fund borrows money and uses that borrowed money to purchase bonds and other fixed-income assets. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case. With that said the benefits of leverage today are much less than they were a year ago due to the fact that borrowing rates are much higher.

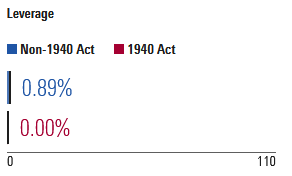

However, the use of debt in this fashion is a double-edged sword because leverage boosts both gains and losses. As such, we want to ensure that a fund is not using too much leverage because that would expose us to too much risk. I do not like to see a fund’s leverage exceed a third as a percentage of its assets for this reason. Fortunately, the AllianceBernstein Global High Income Fund easily satisfies this requirement. As of the time of writing, the fund’s levered assets comprise 0.89% of its assets:

Morningstar

This is a remarkably low level of leverage, especially compared to the 30%+ that is used by most other closed-end funds. We can therefore conclude that we should not have to worry much about this fund’s use of leverage. Indeed, it could probably take on more and still be striking a reasonable balance between risk and reward.

Distribution Analysis

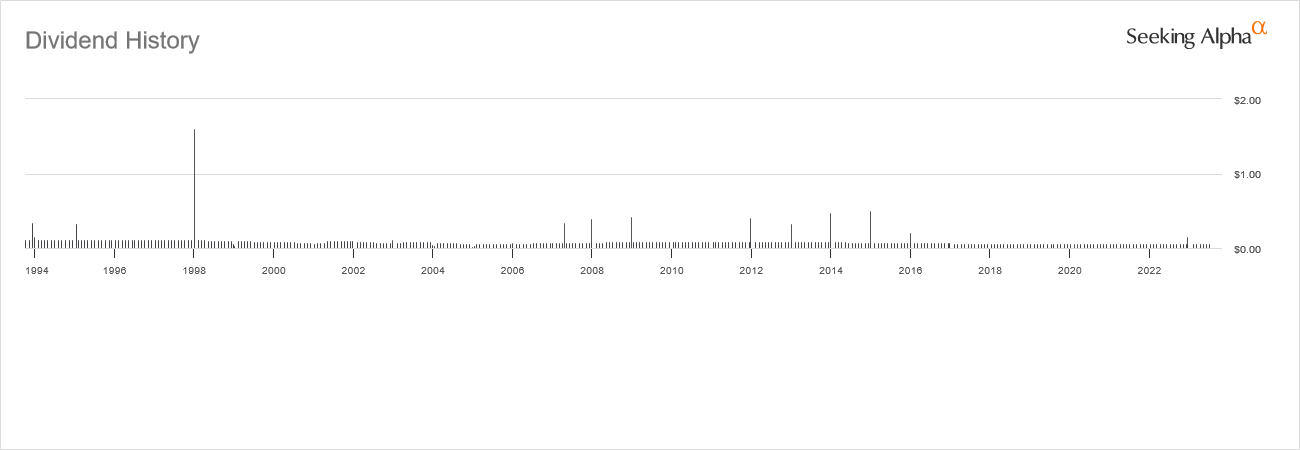

As mentioned earlier in this article, the primary objective of the AllianceBernstein Global High Income Fund is to provide its investors with a high level of current income. In order to accomplish this goal, the fund primarily invests in high-yield bonds issued by companies all around the world. In some cases, these bonds will boast much higher yields than bonds issued by American companies. This is particularly true if the issuing entity is located in an emerging market. The fund also engages in bond trading to take advantage of changes in bond prices and generate some capital gains. It then pays all of its investment profits out to the shareholders as distributions. As such, we might assume that the fund will have a very high yield itself. This is certainly the case as this fund pays a monthly distribution of $0.0655 per share ($0.786 per share annually), which gives the fund a 7.94% yield at the current price. The fund has varied its distribution somewhat over the years, although it has been stable since April 2019.

Seeking Alpha

The fact that the fund’s distribution has varied somewhat over the years may be a bit off-putting to some investors, particularly those that are seeking a stable and secure source of income to use to pay their bills or otherwise finance their lifestyles. However, it is the case that nearly every fixed-income closed-end fund varies its distribution somewhat over time. This is largely due to the fact that changes in interest rates greatly affect bond performance and they do not have any net capital gains over their lifetimes. The fact that this fund has been able to maintain a stable distribution since 2019 speaks well to it though, as very few fixed-income funds have been able to accomplish that task. It also means that we should investigate further to determine whether or not the fund may be at risk of having to cut soon, as most of its peers have done.

Fortunately, we have a very recent document that we can consult for this purpose. As of the time of writing, the fund’s most recent financial report corresponds to the full-year period that ended on March 31, 2023. This is a much newer report than we had available the last time that we discussed this fund, which is quite nice. The American bond market rebounded sharply this year from its disappointing performance in 2022 and that gave the fund an opportunity to recover some of the losses that it suffered last year. We want to see if it managed to accomplish this task.

During the full-year period, the AllianceBernstein Global High Income Fund received $67,880,521 in interest along with $1,271,615 in dividends from the assets in its portfolio. This gives the fund a total investment income of $69,152,136 during the period. It paid its expenses out of this amount, which left it with $59,434,784 available for shareholders. This was, unfortunately, not enough to cover the $76,201,166 that the fund actually distributed to its shareholders during the period. At first glance, this is certain to be concerning as we normally like a fixed-income fund to cover its distributions solely with net investment income. This one obviously failed in that task.

With that said, the fund does have the ability to obtain money through other means that could be used to cover its distributions. For example, it can trade bonds in an attempt to realize a profit from price changes. Unfortunately, this fund failed in that task during the period. It reported net realized losses of $59,646,186 and had another $49,324,368 net unrealized losses.

Overall, the fund’s assets declined by $125,736,936 during the full-year period. This comes on top of the $65,586,789 asset decline during the prior-year period. It thus does appear that this fund is overdistributing and will almost certainly have to cut at some point to avoid depleting its asset base.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the AllianceBernstein Global High Income Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund’s assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of July 19, 2023 (the most recent date for which data is currently available), the fund had a net asset value of $10.71 per share but the shares only trade for $9.85 each. This works out to an 8.03% discount on the net asset value. That is quite a bit better than the 6.13% discount that the shares have had on average over the past month. Thus, the current price looks quite reasonable.

Conclusion

In conclusion, investors are just as desperate for income as everyone else in today’s highly inflationary environment. The AllianceBernstein Global High Income Fund offers a solution to that as it invests in a portfolio of bonds from issuers all around the world in an attempt to provide its shareholders with a high level of income. It has had some success at this, as the fund does have a remarkably high yield today. Unfortunately, it has seen two years of net asset declines now and there are a lot of reasons to doubt that the distribution is sustainable going forward. The fund does trade at a discount though, so the possibility of a distribution cut is priced in somewhat. It may be best to wait for a cut though, since the fund’s share price will almost certainly decline when that happens.

{kind=link}