RiverNorthPhotography

I specialize in deep value stocks especially turnarounds. Most of my articles in Seeking Alpha are stocks that qualify as deep value. These can be quite lucrative. tipranks.com shows an over 40% average one year return on the 88 articles about stocks I have written in Seeking Alpha. They can also be falling knives, so you really need depth in your analysis and many still don’t work. Deep value stocks by nature are stocks that have fallen hard and have a big upside if they can turn it around. I believe Advance Auto Parts, Inc. (NYSE:AAP) is one such stock. The turnaround itself has not started, but a big first step (replacing the CEO) has.

Background

Advance Auto Parts is a retailer and wholesaler of auto parts. It does almost exactly the same thing and is of similar size as peers O’Reilly (ORLY) and AutoZone (AZO). For years it badly trailed both in profitability. Value investors bought heavily in the belief it was a simple management problem. Since they are similar businesses, there is no way Auto Zone and O’Reilly should have a profit margin of 13-16% while AAP usually gets 5-7% and only got only 1% last quarter.

The similarities between the three are striking. They are in the same industry. All get most of their sales from bricks and mortar and have a limited online presence. They have a similar number of stores, most of which are in the U.S. The store sizes are also relatively similar.

This article looks deeper into what actually is deficient about Advance and can it be fixed. We’ll start with a financial comparison.

Financial Results

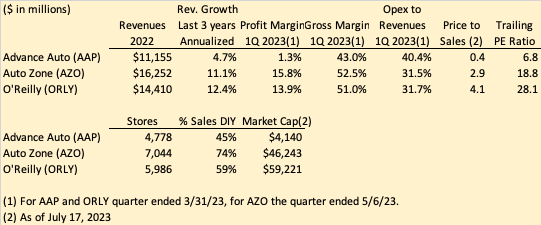

A closer comparison of Advance to its peers is shown below

Value Line, SEC Filings, Yahoo Finance

Usually, the company that grows faster than peers does so by better products or services, underpricing or heavier marketing. AutoZone and O’Reilly both grew much faster than Advance the past 3 years and have much better margins across the board. That is despite selling the same products and not underpricing or doing much more marketing. If they are getting way more growth and profits selling the same stuff at a similar price, there must be something else going on with Advance.

The first quarter of 2023 for Advance was particularly weak. Their profit margins have been running 5-7% in recent years. That is still well below Auto Zone and O’Reilly which have been running 13-16%.

The biggest difference between the three is Advance has the lowest percentage of Do-it-Yourself (DIY) sales while Auto Zone is the highest. Advance gets 55% from the Do-it-for-me (DIFM) market, which is primarily repair shops. Advance management has partially blamed recent underperformance on this mix. They are having a harder time passing on price increases to the repair shops than to consumers. Wholesale margins usually are thinner than retail, so I would expect Advance to normally have a slightly lower profit margin than the other two. However, the difference in mix is not enough to explain Advance’s underperformance. There is another difference and that is that AutoZone and O’Reilly are exceptional. Their profit margins are at the top end for all retailers anywhere.

What really sticks out is the difference in price to sales and market caps between Advance and its two peers. It has about 1/10 th the market cap of its peers despite being similar in revenues and store count. I keep looking at this and saying, this is unsustainable, something has to give.

Last Quarter

Advance reported its first quarter earnings on May 31, 2023, which was late. They had a huge earnings miss and guidance drop. Earnings were $0.72 versus the $2.57 analyst consensus. The analysts, based on company guidance, then slashed 2023 estimates from $10.54 to $5.91. Company revenue guidance was reduced much less from $11.4-$11.6 billion to $11.2-$11.3 billion. This indicates the problems are mostly in the margins, not revenues. In fact, revenues are still expected to grow 1% this year. As a result of the big miss, the dividend was drastically reduced from $1.50 per quarter to $0.25.

On the conference call, management blamed the recent problems on the following:

– a challenging pricing environment in the DIFM (repair shops) segment

– lower tax refunds

– higher labor costs

– a milder winter

– a $17 million accounting adjustment

Of the reasons above, they made clear a pricing war in the DIFM segment has the biggest impact and one they expect to continue the rest of the year. Of the others, all but higher labor costs are one time issues.

But O’Reilly and AutoZone had improved earnings in the first quarter, so something doesn’t make sense. Both should have been impacted by the first 4 reasons listed above. Management stated the DIFM industry is about $100 billion in size and highly fragmented. Advance has about 6% of that. They were asked in the conference call where the pricing pressure is coming from and they claimed it was an industrywide thing, not just from one large competitor. Too add to the confusion, an analyst on the conference call stated he was not seeing others in this space complaining about pricing pressure.

Management did mention supply issues improved during the quarter.

CEO Greco also stated the following:

In some cases, we plan to sell through owned inventory at discounted rates to transition to new higher-margin alternatives.”

I take that to mean more margin pressure this year. Another large issue is what management calls “share of wallet”. They are not losing customers, they are losing share of their customers business. That indicates to me there is a customer service problem, since they claim to be meeting competitor’s prices.

In addition to the big earnings miss and much lower forward guidance, the Board cut the quarterly dividend from $1.50 to $0.25. As a result of the miss, and guidance and dividend reduction, the stock was cut in half. CEO Tom Greco also announced he was retiring at the end of the year.

Balance Sheet

I would rate Advance’s balance sheet as adequate. There is plenty of time to turn this vehicle around. Interest bearing debt was $1.9 billion on March 31, 2023 and tangible net worth was $1.0 billion. Cash totaled $226 million and working capital was $1.2 billion. Incidentally, both AutoZone and O’Reilly have a negative net worth which they can easily handle with all the cash flow they generate. Advance’s long term debt all matures after 2025. They also have $1.1 billion available on a line of credit which matures in 2026.

Why Is Advance Lagging Its Peers?

While things got much worse last quarter, Advance has been way behind its peers for over a decade. AutoZone and O’Reilly are clearly not having the problems Advance is. As previously mentioned, all three are very similar in size, business type, location and store size. Management on the last conference call mentioned the biggest difference between them and their peers is “sales productivity”. I take that to mean less efficient warehouses and logistics. Less efficient warehouses are not only more expensive, they can hurt customer service. That may explain the lower share of the customer wallet they mentioned.

That alone is not enough to explain it. That leaves management problems and to a lesser degree customer mix (DIY versus DIFM). Advance’s underperformance goes back before the current CEO Tom Greco, who was hired in 2016 and came from Pepsi. He did not have a background in auto parts or retail which may explain the management problems, especially in warehousing.

Catalysts

So why am I a buyer? Well, there are a number of catalysts that could significantly help AAP stock. These are summarized below.

1. New CEO – Current CEO Tom Greco has announced his retirement at year end and the recruitment process has started. Internal and external candidates are being considered. Advance is a profitable large company with lots of upside potential. It should attract a strong candidate. A new CEO with a strong track record alone could pop the stock. I’m not sure why they are even allowing the current CEO to stick around until year end.

2. Sale of the company – Advance has significantly underperformed its peers for over a decade and things are getting worse. If things don’t improve soon, it would be in shareholders’ best interest to sell the company. Due to current leadership at the FTC, O’Reilly and AutoZone would not be potential buyers. But there are many others such as Canadian Tire, Walmart, Amazon, Target, AutoNation, Carmax, Penske, and private equity.

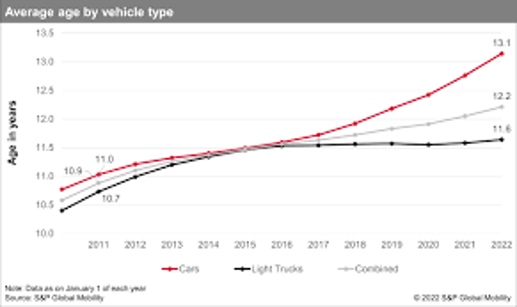

3. Aging of auto fleet – New auto sales dropped significantly during the pandemic due to supply chain shortages. Dealers were charging over list price for the first time I can remember. That means more older cars which need more repairs. This is currently helping the whole auto parts aftermarket industry.

S&P Global

4. Catch up on pricing to repair shops– Advance management claims inability to increase pricing as fast as costs rose in the DIFM segment was the biggest culprit in the big 1Q 2023 earnings miss. If that is so, there is a good chance they will catch up.

5. Get pricing right– Management also claims they are spending a lot of time trying to get their pricing right. Better pricing could benefit earnings.

6. More efficient warehouses – Management indicated that their warehouses are less efficient than their large competitors. I believe this may be one of the biggest issues they have, more so than pricing. This is a long term issue where pricing is short term. They indicated they are investing to improve efficiency.

7. Dividend increase – If earnings start to bounce back as management and the analysts expect, the dividend could be partially or fully restored. That should bring back the dividend investors. The stock was cut in half when they cut the dividend 83%, though part of that was due to the much lower earnings and guidance. However, keep in mind the current $0.25 quarterly dividend is actually well above the $0.06 dividend paid from 2007-2019.

8. More online sales – Advance currently only gets about 3% of its revenues online. However, this is up considerably in recent years and they mentioned on the last conference call they are pushing hard for more growth.

9. Supply chain improvement – Management on the conference call stated they have not had sufficient inventory to meet customer needs but the supply chain is improving. This should help revenues.

Risks

The company faces a number of risks, some of which are detailed below.

1. Recession – Most companies are impacted by a recession which many economists believe is likely within the next year. I expect it this year as I have written in several recent articles. This industry however, is less susceptible to a recession than most, and has held up well in the past. This is actually a reason to own it now.

2. EVs – EVs use much less parts than other cars and at some point will likely have a major impact on the car aftermarket parts industry. However, EVs are still only about 1% of the cars on the road in the U.S. They are also the newer ones, so a significant impact is a few years off.

3. More investment – Management talked about needing more investment in DIFM and warehouses. That will reduce free cash flow.

4. Competition– Auto Zone and O’Reilly are currently eating Advance’s lunch and its only getting worse. If this continues Advance may become too weak to fight back. This is still a ways off with the balance sheet they have.

Takeaway

Something has to give when two very similar competitors are much more profitable and the gap is widening. Advance has time to fix the problems, it’s still profitable and has an adequate balance sheet.

I believe Advance’s problems are primarily threefold; management, higher DIFM sales than peers and inefficient warehouses. New management can fix the first and third and maybe nudge the second. Some may say they have underperformed for over a decade and new management didn’t help last time. My counter is they brought in a CEO with no industry experience and stuck with him too long. He was clearly not the answer. The process to find a new CEO is underway.

An operating improvement is going to take a while. When you slash the dividend and ease out the CEO that means it’s unlikely to be a quick fix. In fact, based on management’s comments on the conference call, I expect them to miss the earnings estimate of $1.63 for the second quarter just ended. However, the first quarter of 2023 should be a bottom as it was impacted by some one-time items.

I believe the stock can return to the $150 it was trading at when the year started. At that level it is still trading at 20-25% of its peers based on price to sales. What I’m saying is it just needs to go from mediocre to average get a double. My price target is $150 in 18 months. That would be a 117% return from the $69 current price.

{kind=link}