julie_bartoo/iStock via Getty Images

Last April, I wrote about Unit Corporation (OTCQX:UNTC) for Seeking Alpha and suggested it was an attractive investment option with limited downside. I also wrote a thread on Twitter last June, proposing that Unit represented an attractive long option relative to SandRidge Energy (NYSE:SD), given their similar positioning in Oklahoma and production profiles. Unit has outperformed and paid $12.50 in special dividends versus $2 from SandRidge, and I want to re-examine which is more attractive to own going forward.

Production Assets

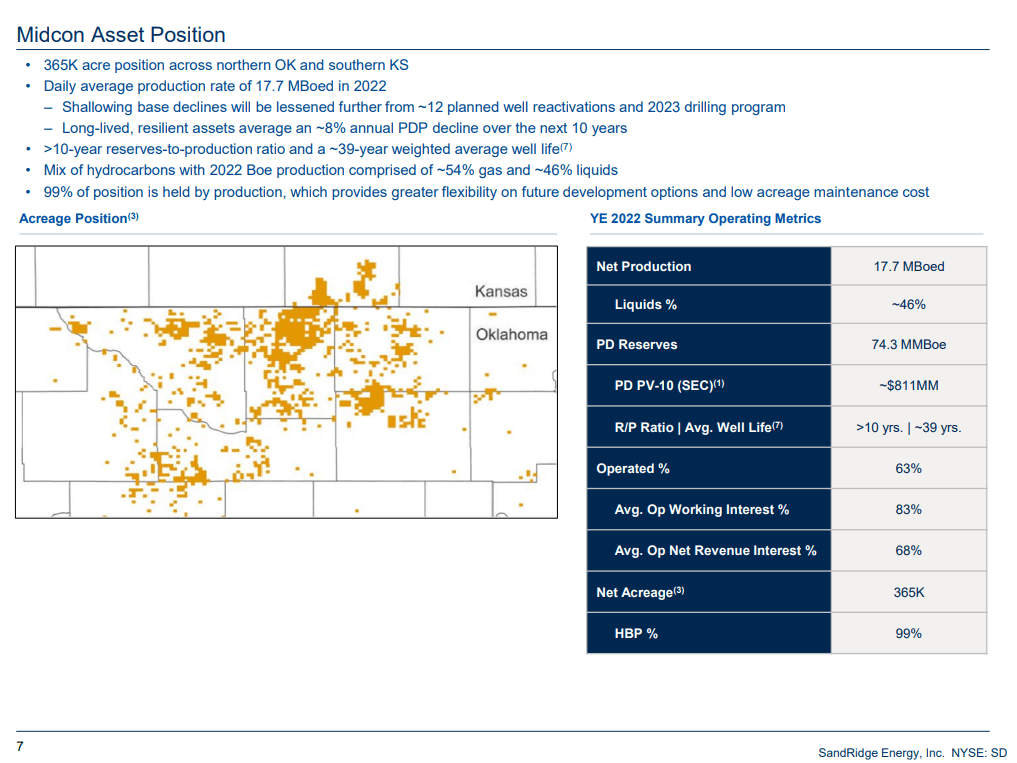

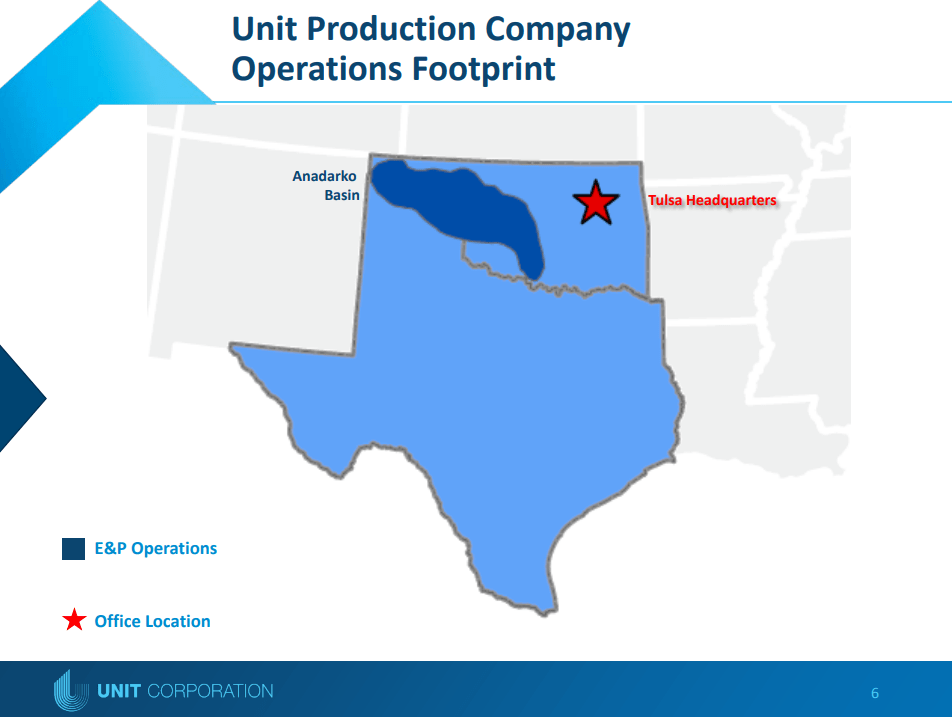

Unit and SandRidge primarily operate in Oklahoma, with SandRidge focused on the Mississippi Lime Basin and Unit operating in the Anadarko basin.

SandRidge IR

Unit IR

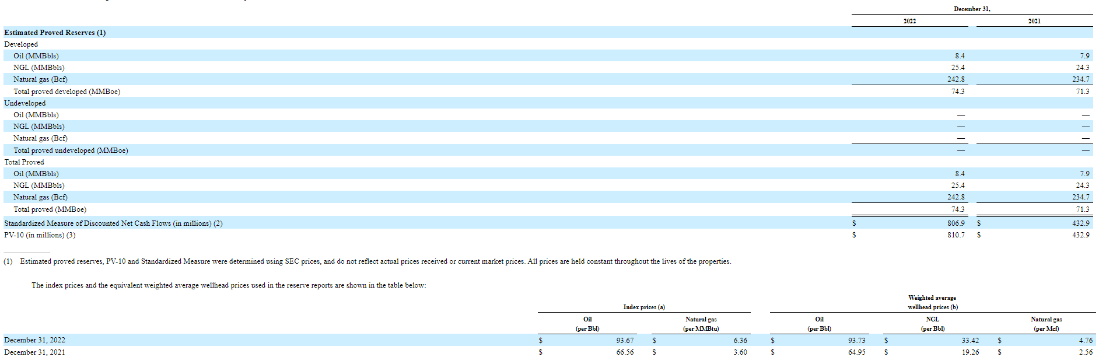

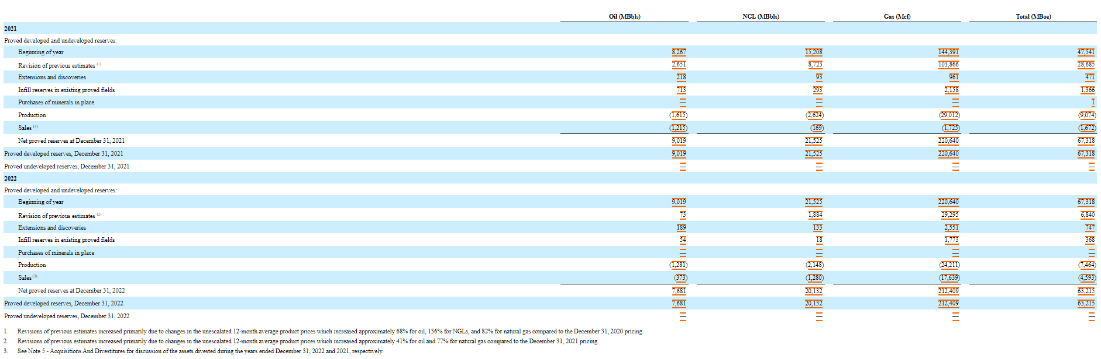

Each operator has a similar oil/gas/NGL production profile and reserve base, as you can see from their latest 10-Ks:

SandRidge 10-K

Unit:

Unit 10-K

SandRidge has a higher overall proved reserve base than Unit at YE22:

|

Reserves |

Unit |

SandRidge |

|

Oil (MMbbl) |

7.7 |

8.4 |

|

NGL (MMbbl) |

20.1 |

25.4 |

|

Gas (Mcf) |

212.4 |

242.8 |

(Source: Company filings @ 12/31/2022)

Looking at current production, their Q1-23 was as follows:

|

Q1-23 Production |

||

|

Oil (Mbbl) |

300 |

261 |

|

NGL (Mbbls) |

419 |

420 |

|

Gas (MMcf) |

5,369 |

4,912 |

|

Total (Mboe) |

1,614 |

1,500 |

(Source: Company filings)

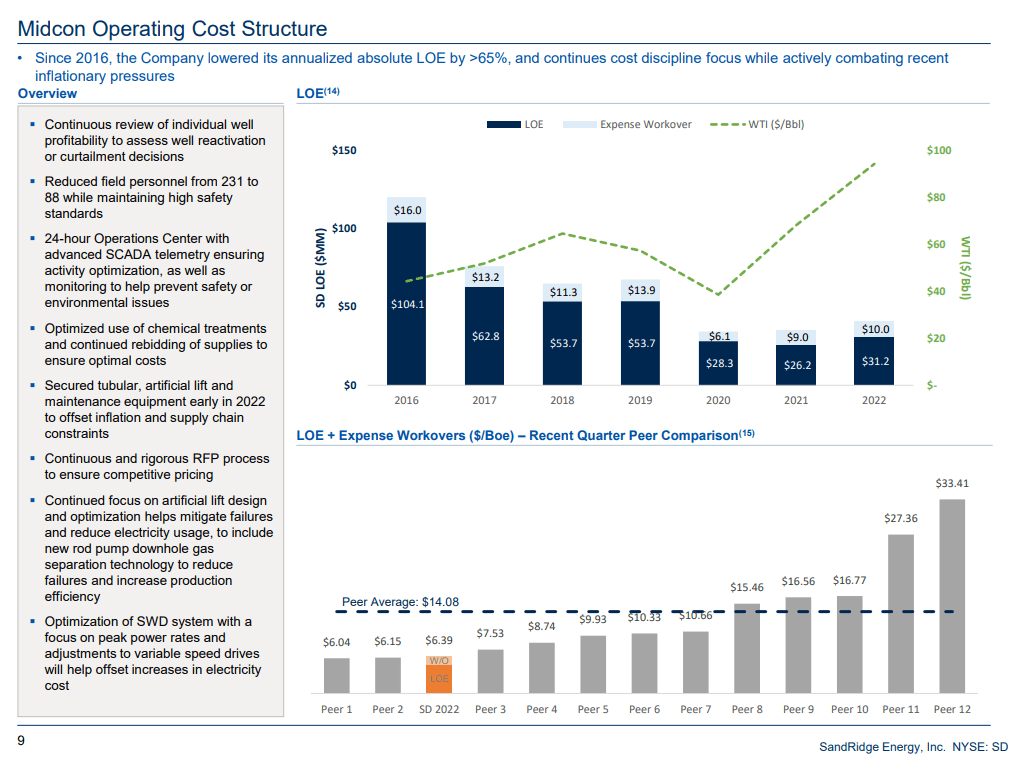

Unit’s operating expenses for production (ex-D&A) were $17.2m ($10.63/MBoe) versus $15.4m ($10.27/MBoe) for SandRidge during Q1, giving SandRidge a slight advantage on production costs. Both companies stack up well against Midcon producers, per SandRidge’s chart:

SandRidge IR

All in, Unit is earning slightly more from their production segment on a gross basis due to higher total production, offset by marginally higher production costs. Both businesses benefited from hedges in Q1, and Unit has a portion of oil and gas hedged at low prices for the remainder of 2023.

An important issue to consider is Asset Retirement Obligations (“ARO”), as Unit has about $24m in future liabilities expected from retiring their wells, but SandRidge has $65m, that significantly offsets their higher reserve value.

As a point of valuation, SandRidge just acquired minority interests in 26 wells they operate for $11.25m. These wells are ~30% oil and averaged 500 Boe/day during Q1-23 (3% production increase, $22.5k/Boe/day implied valuation). These wells appear more valuable given their oil content relative to both Unit and SandRidge’s current production, but we can assume they were bought on somewhat favorable terms given the existing minority interest. Valuing each company’s production using this transaction would generate:

-

1,614 flowing Mboe/90 *22.5k = $403.5m for Unit

-

1,500 flowing Mboe/90 *22.5k = $375m for SandRidge, plus this new $11m acquisition

I’m comfortable valuing each segment around $400m given current oil and gas curves, though these valuations will be sensitive to future movements in commodity prices.

Drilling

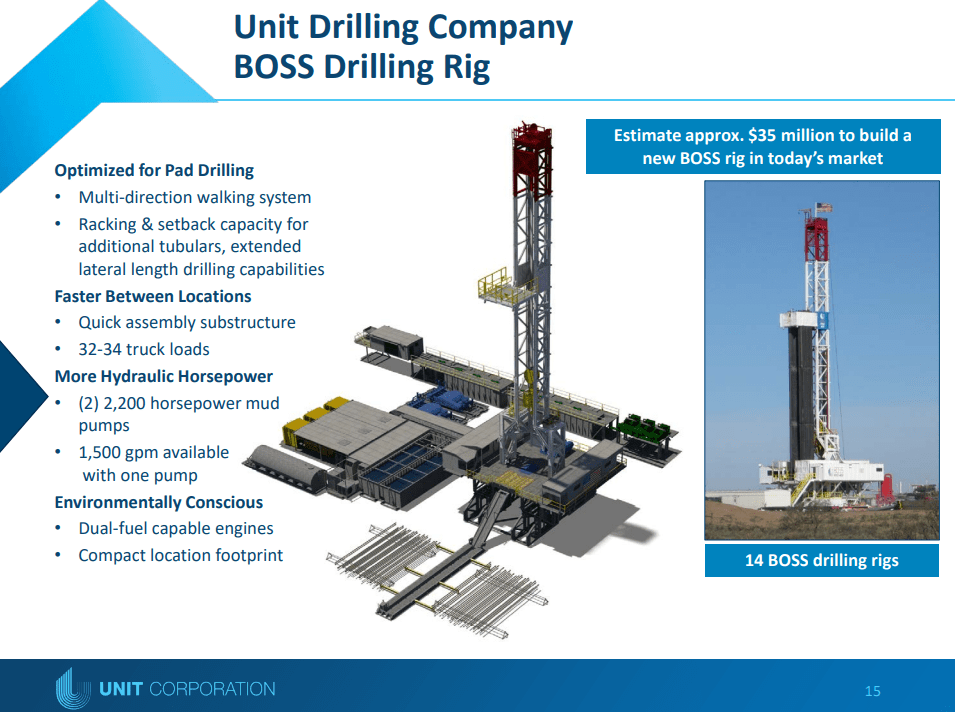

Unit IR

While SandRidge is focused on production, Unit also maintains a drilling segment with high-spec BOSS rigs. In Q1-23, these rigs generated $45.9m of revenue and about $19m of operating income. HP and ICD seem to be anchored at higher day rates (mid $30ks versus $30.8k for Unit) and I expect these rates to find decent support in this range unless resource prices decline further.

Despite its terrible capital structure with 22.5% effective convertible interest, Independence Contract Drilling (ICD) helps me comfortably value Unit’s rigs at $150-$200m. This is not an amazing earnings multiple, so if Unit sells the segment for this amount, I imagine the buyer will do very well. But now that Unit has activated all the BOSS rigs and scaled up day rates, this segment should generate significant cash in the near term.

Cash Balances

At the end of Q1-23, SandRidge was carrying $286m of cash, and Unit had $171m. The following adjustments should be made:

-

Unit’s $2.50/share dividend in Q2 (-$24.1M)

-

Unit’s $20m sale of Superior (+$20m), of which $12m was received in Q2 and $8m is deferred 12 months

-

SandRidge’s $2/share special dividend in Q2 (-$73.8m)

-

SandRidge’s $11m acquisition

-

Net adjusted $167m cash at Unit and $201m at SandRidge

Both companies have open share repurchase programs in place, which if used may reduce cash further, and both should generate meaningful cash from operations in Q2, likely more at Unit due to rigs.

Valuation

Using the above numbers, Unit has:

-

$400m production

-

$150m rigs (low end)

-

$167m adjusted cash

-

9.6m shares outstanding

-

$75/share valuation (60% upside)

SandRidge has

-

$400m production

-

$201m cash

-

36.9m shares outstanding

-

$16.29/share valuation (4% upside)

As a bonus, Unit is returning capital and selling properties, while SandRidge is actively looking for acquisitions. This may benefit SandRidge in the long run, if they can find deals on attractive terms and energy prices subsequently increase. Unit is run by a fund manager taking no salary, which also indicates they are more likely to sell the business in the near term, offering investors a catalyst for value realization.

If you want to value each company based on cash generation, the result will also be favorable for Unit given their rigs and higher current production levels (Unit did ~$49m FCF in Q1-23 versus ~$30m for SandRidge). Unit also declared a regular $2.50/share dividend in Q2 which they appear capable of maintaining at their current earnings level, generating over a 20% yield versus the $0.10 quarterly dividend at SandRidge (set to begin August 2023) yielding ~2.5%.

Other Considerations

I see few reasons compelling me to own SandRidge over Unit. As covered above, they do have a slightly larger reserve base, but I think this advantage is offset by their ARO. There are some other considerations raised in this Twitter thread that I would also evaluate before acquiring shares in SandRidge. Their recent reactivation program for wells has certainly delivered a temporary boost but may not be as sustainable as hoped.

SandRidge IR

SandRidge does have lower G&A expenses than Unit, which presumably reflects their more streamlined operation and lack of drilling segment.

Carl Icahn owns a large chunk of SandRidge, and his recent battles with Hindenburg seem like a possible catalyst for SandRidge enhancing their capital return, mere days after they demurred.

The best argument for owning SandRidge is that they are buying while Unit is selling, and SandRidge would be better positioned for another boom in resource prices. Given their large cash position, I don’t think either of these stocks will give you the ideal torque you’d want in that scenario, but it’s the one scenario where I think SandRidge is most likely to outperform Unit. A company like W&T Offshore (WTI) would likely be more interesting in such an environment.

A final consideration is Unit trades over the counter and averages about $700k of volume per day, versus ~$9m of volume per day and an options chain for SandRidge. For a deep-pocketed investor or fund this may make a difference, but I think the valuation gap more than makes up for the liquidity overhang.

Conclusion

If you bought SandRidge during the depths of Covid (or earlier) you certainly made a fantastic return, but going forward I expect investors in Unit will outperform. Both companies’ production assets are close in value, but the extra value from Unit’s rigs puts them ahead even if illiquidity may be an issue for larger investors. If energy prices recover, investors in both companies should do well.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

{kind=link}