bjdlzx

Baytex Energy Corp. (NYSE:BTE) recently purchased Ranger Oil (ROCC). But management is still going for more benefits now that the acquisition was completed. Management recently announced a normal course issuer bid that will result in stock purchased at a lower price (so far) than when the acquisition was announced. Repurchasing stock at a cheaper price in effect lowers the cost of the acquisition. Every share repurchased also enhances the effect of the acquisition exposure.

But there are still more benefits to come. The acquisition improved finances to the point that management felt comfortable initiating an C$.09 per share initial annual dividend (paid in quarterly amounts).

Debt

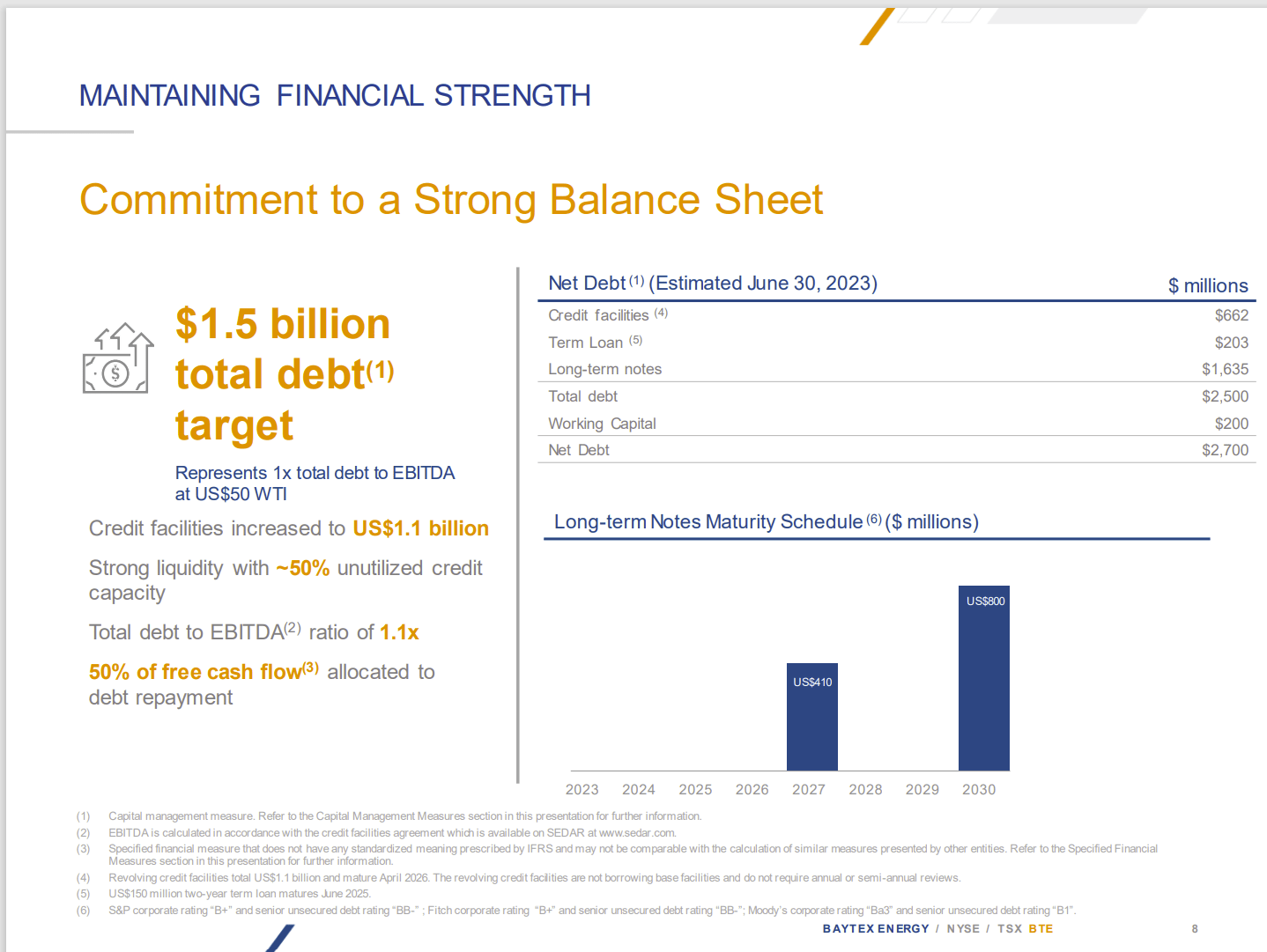

Management has issued the following debt guidance:

(Canadian Dollars Unless Otherwise Stated.)

Baytex Energy Revised Debt Guidance (Baytex Energy July 2023, Corporate Presentation)

Management now has a new debt guidance based upon materially higher production levels. Since there is now a material amount of production coming from the Eagle Ford in the United States, that debt shown above in United States dollars can likely be serviced with the money earned in United States dollars from the Eagle Ford operations. Therefore, in practice there could be no gain or loss despite the accounting reporting each month. Instead, there would be just a net translation on the cash remaining that Baytex collects after debt servicing.

Production Growth

Production per share will grow as a result of the acquisition. Now the accretion due to the acquisition that management showed as an acquisition benefit will increase with the share repurchase program that was previously stated.

But management is also likely to grow production as the assimilation and optimization process gets underway. Technology keeps moving forward with the result that many companies are reporting stronger than expected well results. This company is likely to report similar results.

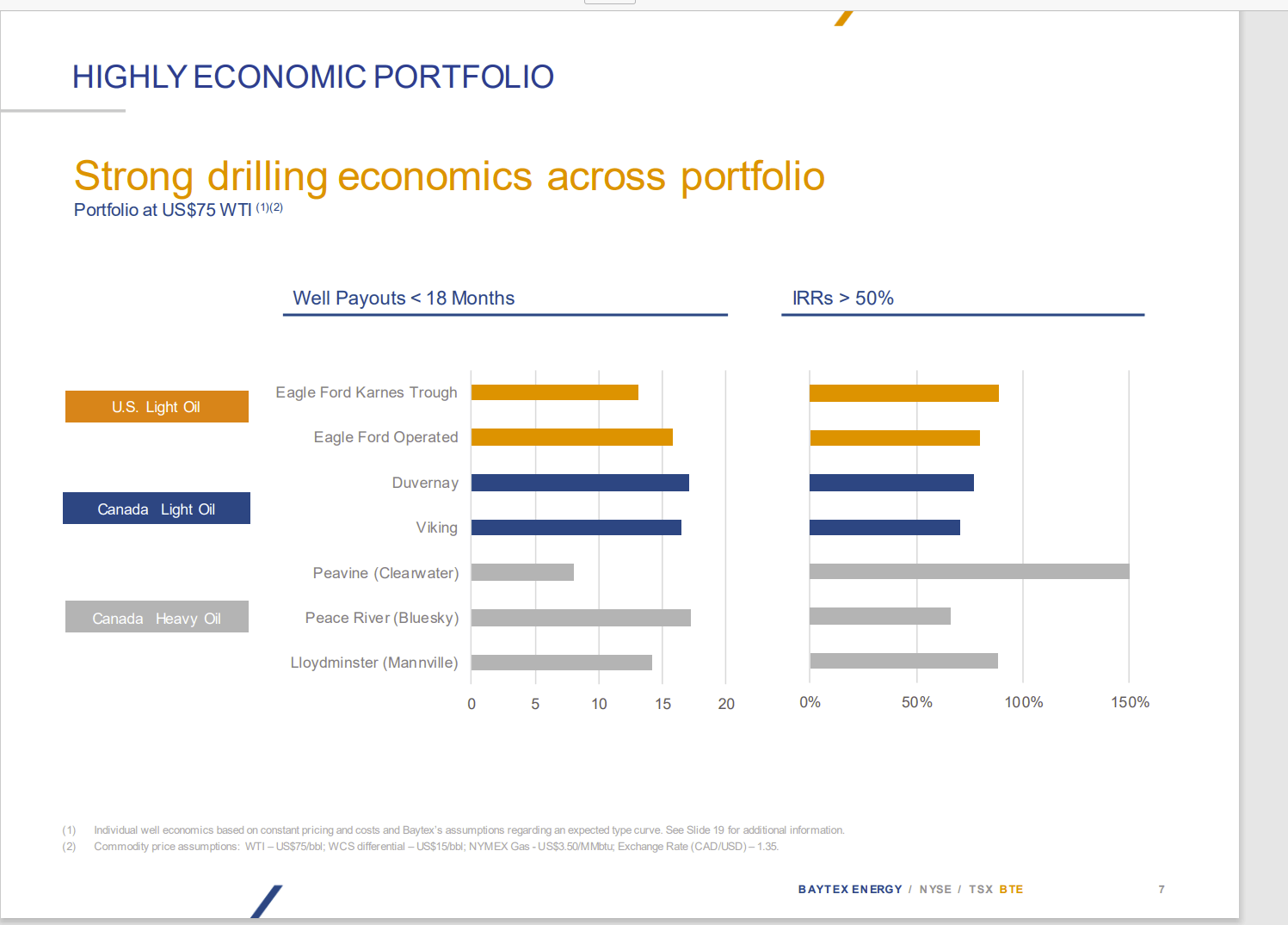

Baytex Energy Portfolio Payback Periods And Rates Of Return By Lease Area (Baytex Energy July 2023, Corporate Presentation)

The Eagle Ford non-operated acreage is operated by Marathon Oil Corporation (MRO). This is an outstanding partner with one of the better operating records in the industry. So it is no surprise that the Marathon operated acreage has slightly better Eagle Ford returns than the newly acquired acreage.

Investors should expect that Baytex will likely used knowledge from the Marathon Partnership to improve returns on the newly acquired acreage.

But the other consideration is that the heavy oil earnings are extremely volatile because heavy oil is sold at a discount to WTI. That discount tends to expand during industry downturns to the point that heavy oil operations may get shut-in to reduce negative cash flow. Therefore, the light oil must carry the company through an industry downturn.

This means that the debt ratios need to be satisfactory with the possible shut-in considerations in mind. Hence, management’s goal of a lower debt level than is the case currently.

Generally, the Clearwater play has by far the lowest costs. It may well cash flow even with a widening discount during a downturn. But that has yet to be demonstrated. Therefore, management is unlikely to count on that cash flow until it can be demonstrated with actual history.

The increased light oil production as a result of the acquisition will likely allow for the company to expand Clearwater heavy oil production. The costs of Clearwater production are so much lower than the other heavy oil production that management will likely only maintain production elsewhere for heavy oil.

It probably is not a good idea to sell the relatively high-cost heavy oil production because technology is moving so fast, that those basins could become competitive or even favored in the future. The most desirable basin has been switching for some time as unconventional technology moves forward (and gets adopted elsewhere). So, it would not be unreasonable to assume such a possibility in the future.

Overall, once the assimilation process is complete, the company will likely (finally) grow production in the future while paying down debt. The years of a straightjacket amount of debt appear to be over with (finally).

Superior Investment Strategy To Pantheon Resources (and Why)

Pantheon Resources Plc (OTCQX:PTHRF) is a British company. As such, the company reports every six months rather than the usual quarterly reports most are used to. The stock is listed on several markets. But investors need to remember that this is essentially a development stage company with little to no source of income. It is therefore very dependent upon periodic capital raises. The chief risk would therefore be so much dilution that the eventual change to an operating company would leave the investor little to no hope of recovering the investment (let alone making a profit).

As I noted in a previous article that I wrote, a lot of leaseholders had no problems handing over the leases for little to no cost for the company. Therefore, investors are forewarned as to what industry insiders believe the value of these leases to be. Only investors willing to risk the entire loss or principal should even consider an investment like this. Disciplined traders may be able to take advantage of price swings. But the discipline to walk away with a profit is something that eludes a lot of investors in this situation.

Therefore, for most investors, it is far better to consider investments with a company that has a source of income. In this case, I will repeat the comparison to Baytex Energy Corp. ((BTE)) to see how both have progressed since that last article.

The Alaska Project

Pantheon has made some progress with well flow rates.

Pantheon Resources Well Development Cost Progress (Pantheon Resources Corporate Presentation)

Clearly, well development costs have gone from “out of sight expensive” to merely “darn expensive.” Even though flow rates are now in the 500 BPD (at the 30-day measurement) range and the wells in this area tend to be long-lived, it would take a very long time to return the costs of developing a project like this.

The North slope has a lot of extra costs like roads and transportation of the production to a place where it can get to market. Then there is the cost of doing business in an extreme weather environment.

Management does have hope that they now know how to drill and complete wells for better results. But then again, the company does not really have the money to undertake the development of a project of this size.

Given the fact that wells will vary on the matter of success levels even in the same basin, this project has a high degree of risk for any partner that decides to join the company in this venture.

The Penny Stock Allure

Many investors believe that it is easier for a stock price to move from five cents to ten cents than it is for a stock price to move from one hundred dollars to two hundred dollars. Nothing could be further from the truth. Many things determine stock price movement.

But a small company with a few shares outstanding at one hundred dollars each will change value about the same as a comparable small company with a lot more shares outstanding at five cents each. The reason is that earnings prospects largely determine valuation.

Sometimes a small company like Pantheon captures the fancy of the market for a period of time because investors see a lot of reserves and think that this company will generate a lot of cash. But those reserves only mean something if they can be produced profitably. Here, industry insiders, through the transfer of leases to this company clearly indicated there was a lot of work ahead at the time of the transfer. Now at a few years later, it still looks like there is considerable work ahead before there will be any (let alone sufficient) cash flow.

Baytex Energy Achievement Comparison

Back in fiscal year 2020, I compared Baytex Energy to this company to try to demonstrate that a company with earnings that is established and is now listed on the NYSE would probably be a superior choice.

Baytex Energy Recommended Price And Stock Price Progress Since The Last Article (Seeking Alpha Website July 10, 2023)

Since I made the recommendation, the considerably larger company, Baytex Energy Stock Price, has appreciated more than 1,000% in the roughly three-year period. Not only that, but the company has sustained those gains and management is going for still more gains.

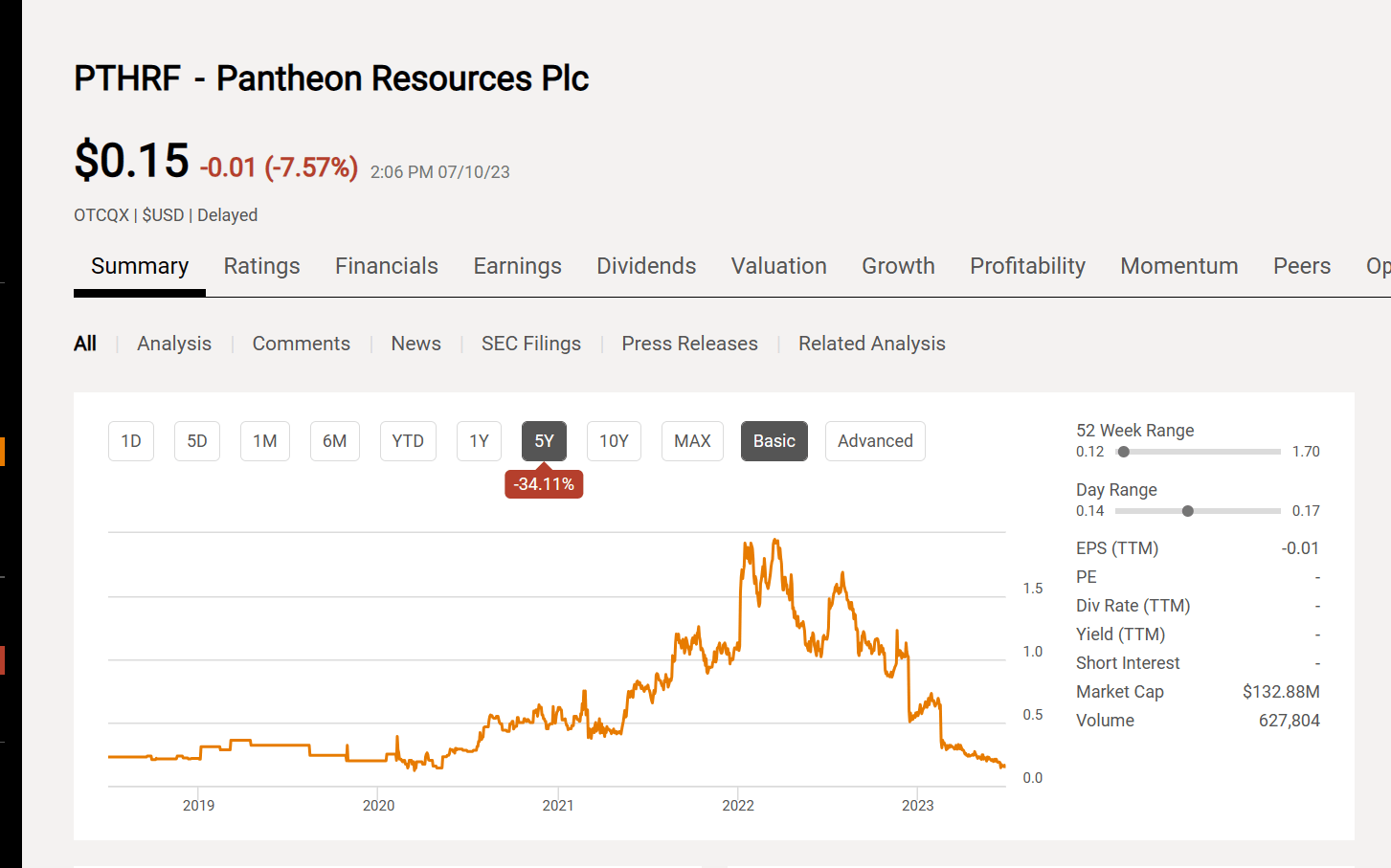

Pantheon Resources Stock Price History And Key Valuation Metrics (Seeking Alpha Website July 10, 2023)

Pantheon Resources, on the other hand, had a speculative price runup as shown above, that likewise would have potentially provided shareholders with a great return. However, an investor would have needed to sell and then walk away. The stock is nothing close to safe enough for a buy and hold strategy. Now if the shareholder did that, then a decent return was obtained. But if the shareholder hung on to the present time, then all the gains were in effect lost.

Since there is no continuing revenue at the time, a shareholder is basically stuck with hoping for another price runup as occurred before to get out. But lightening rarely strikes twice. Therefore, the time to make money may be gone for some time to come.

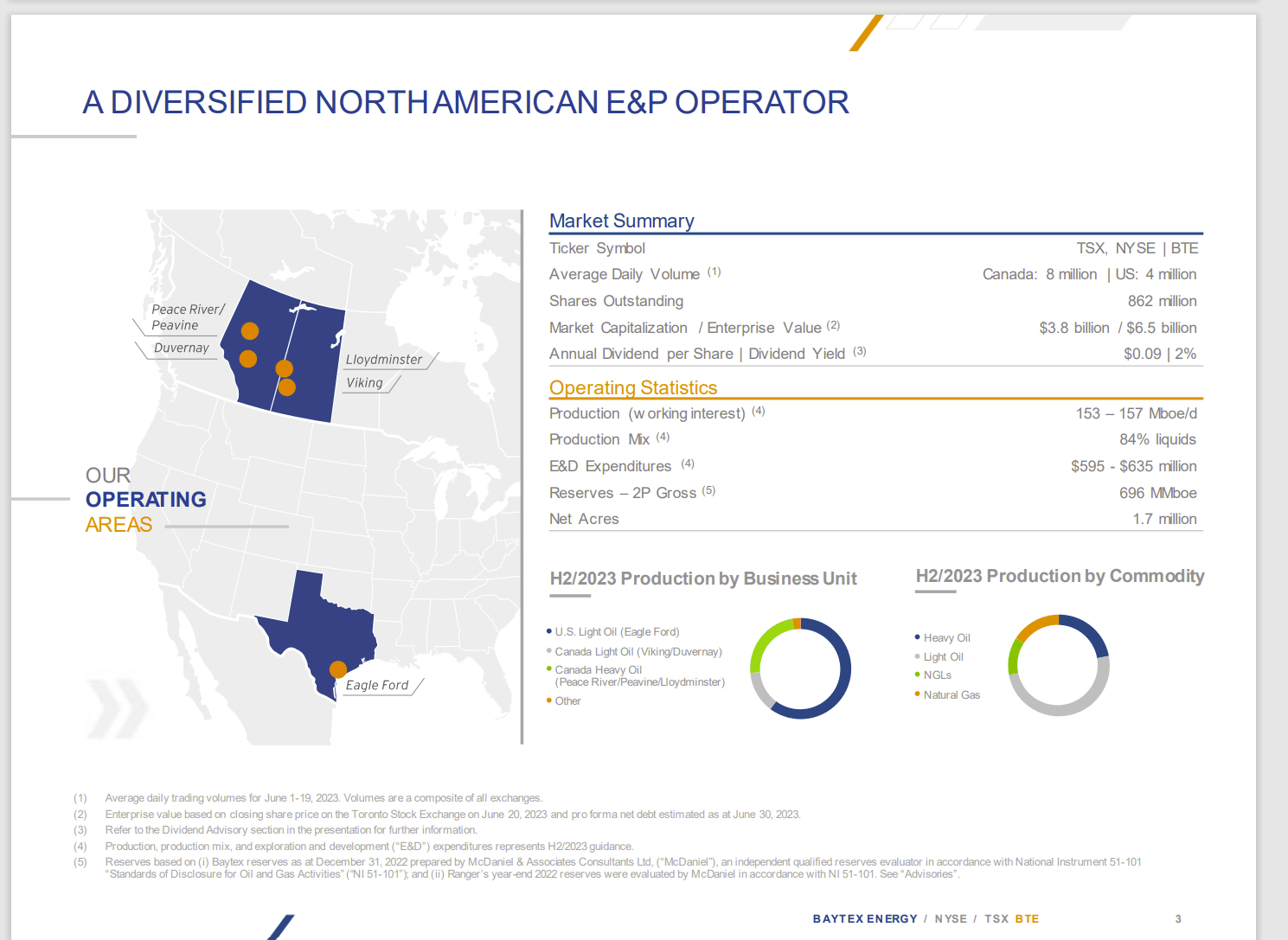

Baytex Energy Company Overview Of Operations (Baytex Energy July 2023, Corporate Presentation)

Baytex Energy recently completed its acquisition of Ranger Oil to add considerable light oil production from the Eagle Ford. The company is still trying to make the Duvernay discovery commercial (similar to the situation Pantheon is facing). But the company has bright prospects outside of that discovery to power considerable growth well into the future.

Management announced a Clearwater discovery of a new low-cost heavy oil prospect that is likely to power earnings forward for years to come. Unlike the Duvernay, no work was needed to make this one commercial. The Clearwater discovery is, therefore, being developed as we speak.

The earnings and the likelihood of low-cost development possibilities at Clearwater and the Eagle Ford point towards a future of production growth. Baytex Energy Corp. can continue its work on the Duvernay while providing shareholders with stock price appreciation and a newly established dividend.

Conclusion

Any development stage company is likely to be a trading proposal for disciplined traders who know when to walk away with a profit. That is generally a very specialized situation for those who know how to handle the risk.

In contrast, an investment in Baytex Energy not only had a similar stock price appreciation, but the stock price sustained that price appreciation. So, the average investor who gets caught up in work and family issues does not need to worry about profits vanishing into losses.

Any investment needs monitoring. But some need less attention than others. Clearly, the Baytex investment idea needs less attention than does Pantheon Resources. Therefore, for investors, Baytex Energy Corp. remains a strong buy consideration (despite the price runup) as the company exploits the Clearwater discovery and assimilates the recent acquisition of Ranger Oil.

Pantheon Resources, on the other hand, is really not a consideration for most investors. It is simply too hard for most investors to make money on a stock like that.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

{kind=link}